TOP NEWS AFFECTING THE STOCK MARKET THIS WEEK:

-

Department of Justice V.S. Google! The Outcome...Who Won...Who Lost...and The 3 Stocks That Will Benefit! (Source)

Stocks mentioned: $GOOG, $AAPL, $META

For years, the Department of Justice (DOJ) pursued Google (GOOG) in one of the most high-profile antitrust battles of the modern era. Regulators alleged that Google abused its dominance in search and advertising by making Google Chrome the default gateway to its services and locking out rivals. The most aggressive remedy on the table was to force Google to sell off Chrome entirely, severing the pipeline between the world’s most widely used browser and the company’s $300+ billion ad empire. This week, the courts struck down that threat. The DOJ lost, and Google will keep Chrome, its most underappreciated strategic asset. This sent Google stock soaring up 10% since the decision.

One of our students in the CEO Watchlist Investment Club asked us, "Why is Google Chrome such a big trigger for you. Seems like something small for me...is it such a big thing in terms of revenue or something?" Now this was a great question because most people probably don't fully understand the implications if Google had to sell off Chrome. Google’s DOJ victory is a much bigger deal than just preserving ad revenue, it protects the engine behind its entire ecosystem. Chrome, with roughly 60–65% of search market share, doesn’t directly generate revenue but amplifies it by defaulting billions of searches to Google each day, securing traffic that feeds the company’s core ads business across Search, YouTube, and its network. More importantly, Chrome provides a critical stream of user behavior data that powers Google’s ad targeting, AI models, and overall effectiveness. It also acts as the gateway to Google’s tightly integrated ecosystem (Search, Gmail, YouTube, Android) keeping users locked in and creating a seamless experience. Without Chrome, Google would face weaker data, diminished targeting, and strategic vulnerability to rivals like Apple and Microsoft, whose browsers could shift users toward Bing or other search engines. By keeping Chrome, Google retains its strongest leverage point, ensuring its dominance in digital advertising and safeguarding its moat against competitors.

For investors, the key takeaway is that Chrome is staying with Google and that this court decision sets a massive precident to protect tech, in general, from an overreach by the DOJ. So which stocks will be direct beneficiaries of this decision, well I've listed my top 3 below for you:

-

Alphabet (GOOG): The obvious direct winner. Preserving Chrome ensures continuity in ad revenues, data collection, and user lock-in across the ecosystem.

-

Apple (AAPL): One part of the courts decision in this case was that Google can no longer have exclusive only deals with companies like Apple. This benefits Apple because they can still charge Google to have their search on Apple devices but also opens the door to even more revenue from competitors who might also want to get listed. If the court didn't rule this way, Apple could have lost a very powerful revenue stream. This is why we saw a nice pop in Apples share price after the courts decision.

-

Meta Platforms (META): Meta is a direct competitor to Google so why does a court decision that helps Google also help Meta many of our students asked? As we explained to them, since Meta and Google are in the same space (ad revenue) they both actually benefit from this decision because it means less regulation and oversight over all companies in this area. Since there is a court ruling that the DOJ overstepped trying to break Google up then that means if the DOJ ever tries to go after META, for a similiar reason, they will more than likely be shut down thanks to this specific case.

The bottom line, if Google lost, it would have been forced to cede control over the default search funnel and its richest source of behavioral data. Instead, it walks away with its ecosystem intact and a huge win. This case shields, not just Google, but all the big tech companies from DOJ overreach, which adds a positive tailwind to the sector as a whole. As for Google, we still view it as undervalued. With a market cap of $2.8 trillion and a forward P/E of 22 we believe Google has another +30% upside from here! Even when you look at analyst estimates they breakdown each of Googles individual segments as being valued at:

-

Search - $1.25 Trillion

-

Deepmind and TPU - $897 Billion

-

Google Cloud - $572 Billion

-

YouTube - $446 Billion

-

Waymo - $173 Billion

-

Network - $138 Billion

When you add up all of the above segments of Google you get a $3.47 trillion market cap. Since Google is at $2.8 trillion this tells us that based on analyst estimates Google still has another roughly 30% more to go to the upside. We personally have a price target on Google of $300/share with a "Strong Buy" rating, right in line with most of these analyst. For a complete list of ALL the stocks we currently own and are buying this week [CLICK HERE] if you're and Investment Club member and if you're NOT an Investment Club member you can sign up to get access to these and more by [CLICKING HERE] and using our [$200 OFF DISCOUNT CODE] as a thanks to anyone that is subscribed to our Newsletter.

-

-

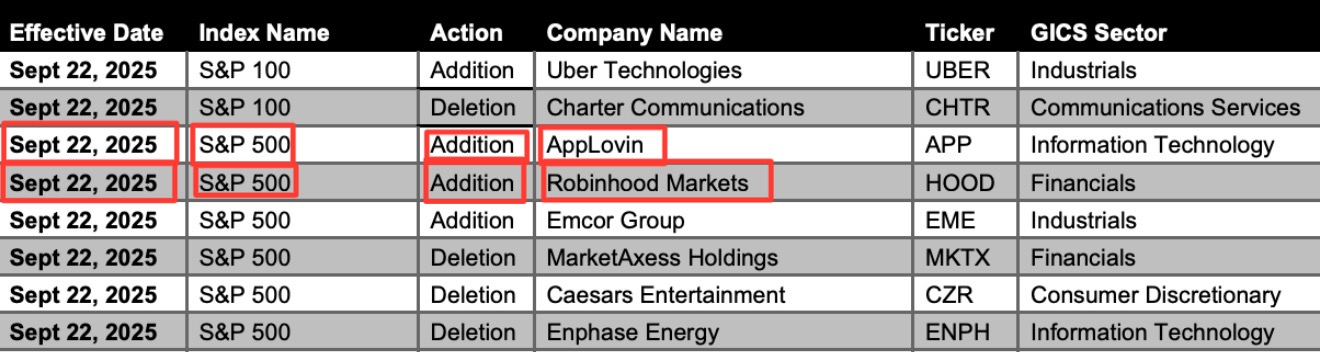

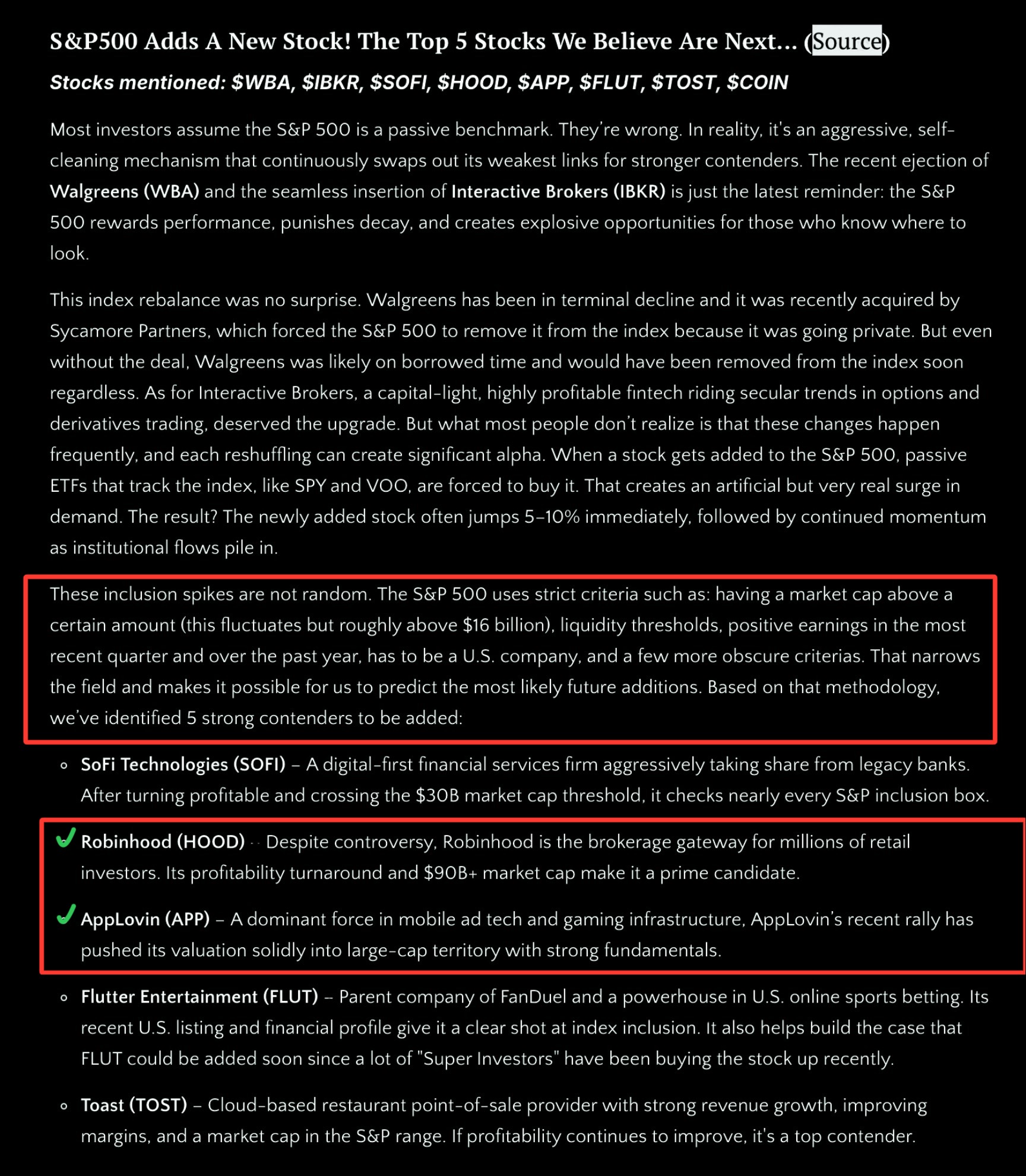

We Predicted Robinhood & AppLovin ... Here Are the Next 5 Stocks Headed for the S&P 500 (Source)

Stocks mentioned: $HOOD, $APP, $FLUT, $TOST, $VRT, $SOFI, $ARES

-

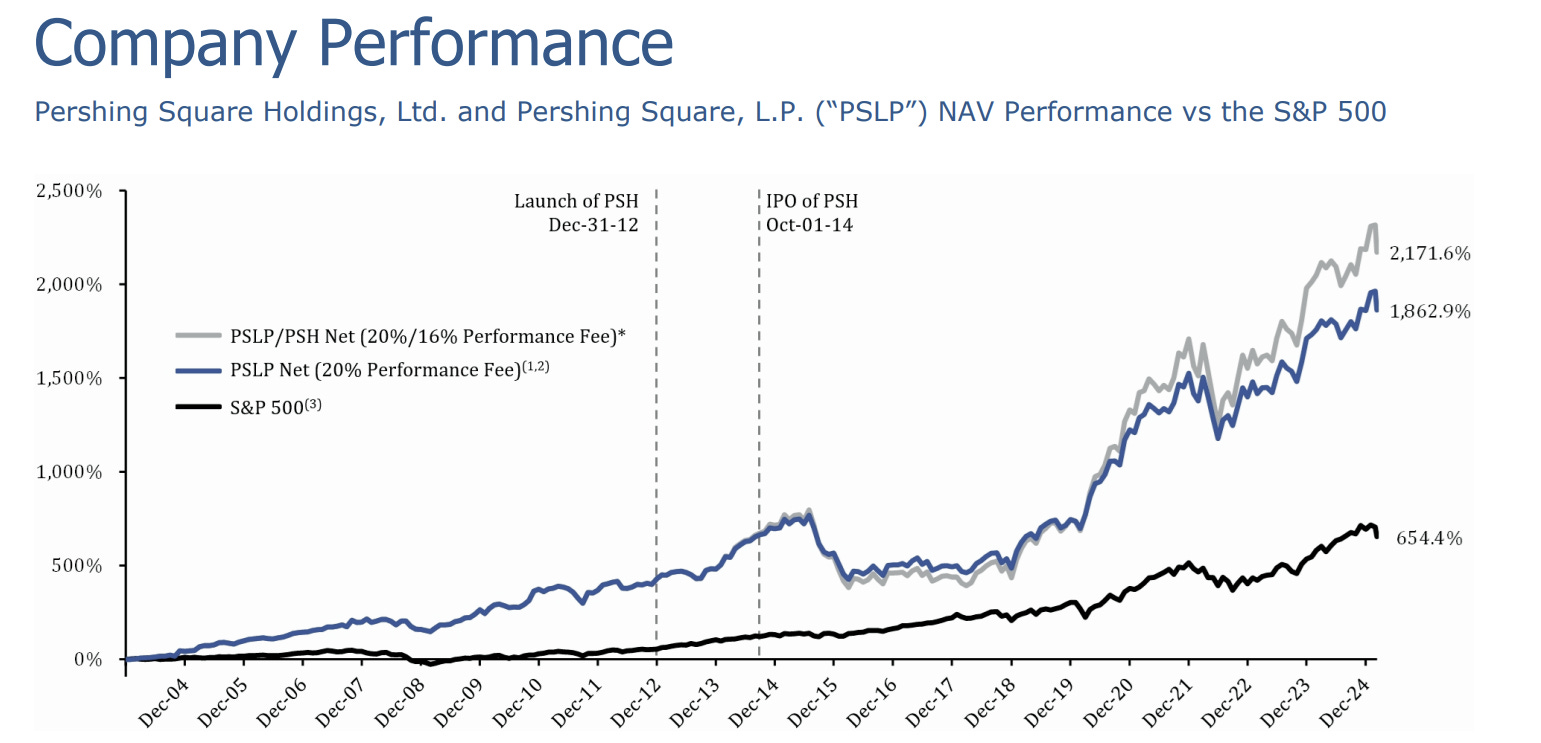

"Super Investor" Spotlight: Bill "The Concentrated Capitalist" Ackman (Source)

Stocks mentioned: $UBER, $BN, $QSR, $AMZN, $HHH, $CMG, $GOOG, $GOOGL, $HLT, $HTZ, $SEG

INSIDER TRADES FROM THE WEEK:

1. Shenandoah Telecommuications Co. (SHEN) - ECP ControlCo LLC, a Private Equity Firm, bought ~$29,000,000 of SHEN stock between May 27, 2025 - Sep 3, 2025, but it was most recently reported to the public on Sep. 4, 2025 (Source)

2. TriplePoint Venture Growth (TPVG) - James Labe, CEO, bought ~$3,100,000 of TPVG stock between Aug 20- Sep 3, 2025, but it was most recently reported to the public on Sep 4, 2025 (Source)

3. Direxion Small-Cap 3x Bear ETF (TZA) - Tim Moore, U.S. Rep. From North Carolina (R), bought between $81,000-$215,000 of TZA between August 12-27, 2025, but it was most recently reported to the public on Sep 4, 2025 (Source)

Over 2,000 people have already signed up for my FREE Masterclass video on how to unlock my exact strategies for finding winning stock/options trades! I'll share everything including how to find what Politicians and CEOs are buying. Don’t miss your chance to get in for FREE before spots fill up!

INFOGRAPHICS FOR THE WEEK:

CONTACT US: [email protected]

Responses