TOP NEWS AFFECTING THE STOCK MARKET THIS WEEK:

Apple Finally Enters The AI Race...But the Real Winner Might Be A Little Unknown Stock That Nobody Is Talking About! (Source)

Stocks mentioned: $AAPL, $MSFT, $GOOG, $AMKR

For years, the story on Apple (AAPL) was simple: brilliant at hardware, but lagging in artificial intelligence. While Microsoft (MSFT) and Google (GOOG) pushed forward with generative AI, Apple appeared strangely absent, risking its position as the most valuable company in the world. That narrative just cracked. Apple has quietly built its own ChatGPT-style system, signaling that the company is finally serious about AI. Analysts are responding in kind, this past week Evercore lifted its price target from $260 to $290, while Wedbush went even further, hiking from $270 to $310. Coupled with record-breaking demand for the iPhone 17 and the iPhone Air, Apple looks like it has found its second wind.

The bullish thesis is clear: Apple has both the hardware distribution and the cash flow to integrate AI across hundreds of millions of devices almost overnight. That scale is unmatched. The new iPhone launch reinforces the story with lines wrapped around city blocks, supply chain chatter suggesting blowout earnings, and consumer adoption that few companies can replicate. For investors, it’s easy to view Apple as a “safe AI play,” where momentum in both hardware and software converge. Yet the company’s sheer size, nearly $4 trillion in market value, creates a ceiling. Even spectacular growth in AI and iPhone sales translates into modest percentage gains. Buying Apple at these levels is more about stability than explosive gains.

That brings us to the real underappreciated opportunity: Amkor Technology (AMKR). Most of you have probably never heard of this company, but Amkor is a $7 billion semiconductor packaging and testing firm, the kind of company most investors overlook until it’s too late. Unlike chip designers such as Nvidia, Amkor sits at a critical chokepoint in the supply chain: it makes sure chips are properly packaged, tested, and ready for deployment into products like Apple’s iPhones. As Apple doubles down on both AI chips and domestic production, Amkor stands to be a direct beneficiary. Trump’s reshoring push, designed to bring advanced manufacturing back to U.S. soil, only strengthens this dynamic. Amkor is already tied into Apple’s plans, making it a vital behind-the-scenes player in America’s AI and hardware renaissance.

Skeptics might argue that Amkor, while strategically important, remains a mid-cap semiconductor services company with cyclical risk. Demand could ebb and flow with the smartphone cycle, and it doesn’t enjoy the same software-like margins that Apple or Microsoft command. But that critique misses the point. The macro shift toward domestic manufacturing is not a quarterly story, it’s a multi-decade project. As long as the U.S. prioritizes self-reliance in technology, companies like Amkor that sit at the physical bottleneck of chip production will not just survive, they will thrive. Unlike buying Apple, investors here are getting in on the ground floor of a structural trend. Even Apple's CEO, Tim Cook, praised Amkor in a recent interview on CNBC where he highlighted Amkor's importance to Apple, stating that, "Amkor will do packaging" for them.

The conclusion is sharp: Apple entering the AI race is a headline, but Amkor enabling that race is the hidden opportunity. Before now, Apple was able to rely on more labor overseas, but now that they are bringing manufacturing, packaging, and testing back to the states, a company like Amkor now has very strong tailwinds. In a market starved for differentiated upside, the companies positioned at supply chain chokepoints, not the trillion-dollar behemoths, offer asymmetric reward. Apple’s AI ambitions are inevitable, but the real underpriced story may be the companies making that ambition possible. For investors looking beyond the obvious, Amkor is a name that deserves urgent attention now, but Amkor isn’t the only name on our radar. Our specialty is spotting stocks with serious upside before the crowd catches on, and this past week alone we’ve flagged several that could benefit into year-end. For those in the Investment Club, make sure to [LOG IN] and check the updated stock and option portfolios. We’ve made a number of fresh buys that you’ll want to review.

Reshoring Revolution: Why Intel Could Be Tech’s Biggest Comeback Story and The 3 Other Winners And Losers...(Source)

Stocks mentioned: $ORCL, $NVDA, $TSM, $INTC

For decades, the logic of globalization was simple: build where it’s cheapest. That story is now being rewritten. The Trump administration is reportedly preparing a rule that would require every chip produced abroad to be matched by a chip produced on U.S. soil, an unprecedented 1-to-1 production ratio designed to reduce dependency on foreign supply chains. At first glance, this looks like protectionism dressed in new language. In reality, it signals something bigger: the age of reshoring technology production is no longer optional, it’s becoming the price of entry to trade in the world’s largest market.

The backdrop could not be more competitive. TikTok, under pressure, is splitting its app into a U.S. and Chinese app, with Oracle (ORCL) taking a direct stake. Nvidia (NVDA) just committed $100 billion into OpenAI to strengthen the United States' largest LLM since Open AI owns Chat GPT. Across the Pacific, China continues to ramp its own semiconductor and AI investments, determined to avoid technological dependence on the West. China announced this past week that they have developed chips that will surpass even Nvidia over the next 3 years. Put simply: the “AI war” is here, and it’s no longer about just apps or algorithms, it’s about where the core infrastructure of computing physically exists. Tariffs and mandates are just tools in a larger contest for control.

The policy constraint, the 1-to-1 production rule, reshapes corporate strategy. Every chip company selling into the U.S. now faces a binary choice: either build fabs domestically or risk 100% tariffs. For some firms, this is an existential cost. Taiwan Semiconductor (TSM), the world’s largest foundry, relies heavily on offshore manufacturing, meaning it faces enormous capital commitments to maintain access to U.S. customers. By contrast, Intel (INTC), long seen as a laggard, suddenly looks like a policy-backed champion. With fabs already on U.S. soil, a direct government stake, and now regulatory tailwinds, Intel is positioned to become the biggest beneficiary of America’s reshoring push.

For investors, the lineup of potential winners and losers is already taking shape:

- Intel (INTC): Once an underdog, Intel has become a policy favorite, with the U.S. government’s 10% stake signaling both strategic necessity and future capital flows. Just this past week, after the Nvidia deal was announced, Intel approached Apple for investments as well. It now seems that Intel is partnering not only with the government but also with major tech players. While the company is far from impressive today, if it can capture even a small percentage of TSM’s market share, Intel could realistically double from current levels.

- Taiwan Semiconductor (TSM): Still the undisputed leader in scale and expertise, but increasingly at risk of margin compression as new mandates push higher-cost U.S. production. The good news for TSM is that it is already building fabs in the U.S. However, even with those expansions, demand will continue to outpace supply, leaving room for Intel to step in. Although TSM remains the technological leader, government mandates may gradually shift the spotlight toward Intel. This is a headwind for TSM, but the company is still a phenomenal long-term investment.

- Nvidia (NVDA): A major indirect winner of reshoring, with AI chip demand so insatiable that any domestic supply expansion helps stabilize its ecosystem. With Nvidia’s recent investment in Intel, the company is not only benefiting from its own momentum but also positioning itself as a financial backer of other tech firms. This gives Nvidia strategic leverage to maintain its lead over competitors like AMD.

- Oracle (ORCL): A sleeper beneficiary, strengthening its position by securing critical infrastructure through TikTok’s U.S. spin-off while deepening ties to government-backed reshoring initiatives. The current administration has publicly stated that Oracle will be a key player in U.S. tech dominance, and historically, companies with such backing tend to perform well. Beyond government support, commitments from Meta and OpenAI further bolster Oracle’s role in this reshaping of the tech landscape.

Critics will argue that such a hardline tariff framework risks inefficiency, higher costs, slower innovation, and the very real possibility of retaliation from trading partners. That rebuttal has merit. But the counterpoint is clear: national security is not about efficiency, it’s about redundancy and control. In a world where software eats the world, chips power the software, and whoever controls chip supply chains controls the trajectory of entire economies. That is the logic driving these moves.

The bottom line: Trump’s 1-to-1 production mandate is not a temporary bargaining chip; it’s the continuation of a trend we have been signaling since the government first took a stake in Intel. This is the domino effect playing out in real time. For investors, the opportunity lies in recognizing that reshoring is no longer a political talking point, it’s an inevitable structural reset. The market is still underpricing how much these policies will reshape competitive dynamics, but the direction of travel is obvious: America wants chips made in America, and Intel is about to be written back into the story of global tech dominance.

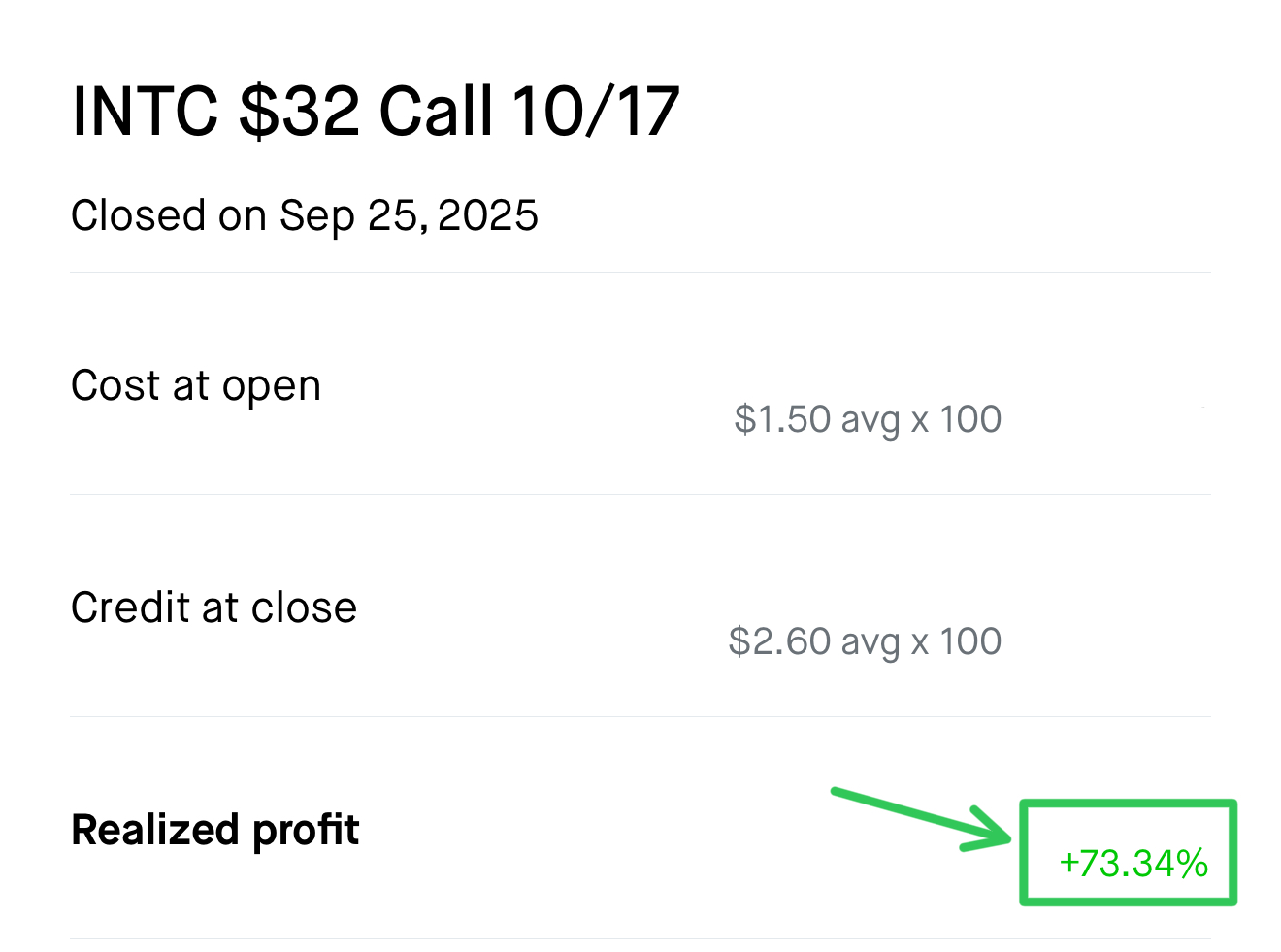

But betting on Intel should come as no surprise if you’re in our Investment Club. We’ve been pounding the table on Intel since the Trump administration took a 10% stake. Just this past week, we capitalized on the move before any of the big headlines broke, locking in trades that delivered more than 73% gains in under 24 hours:

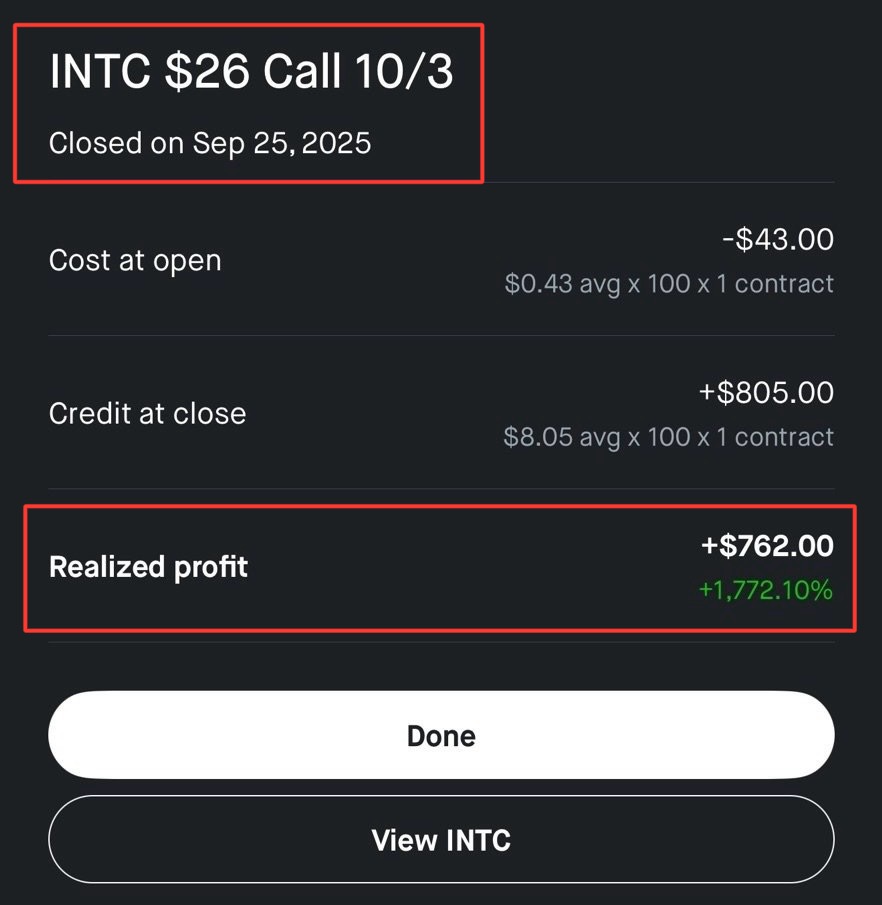

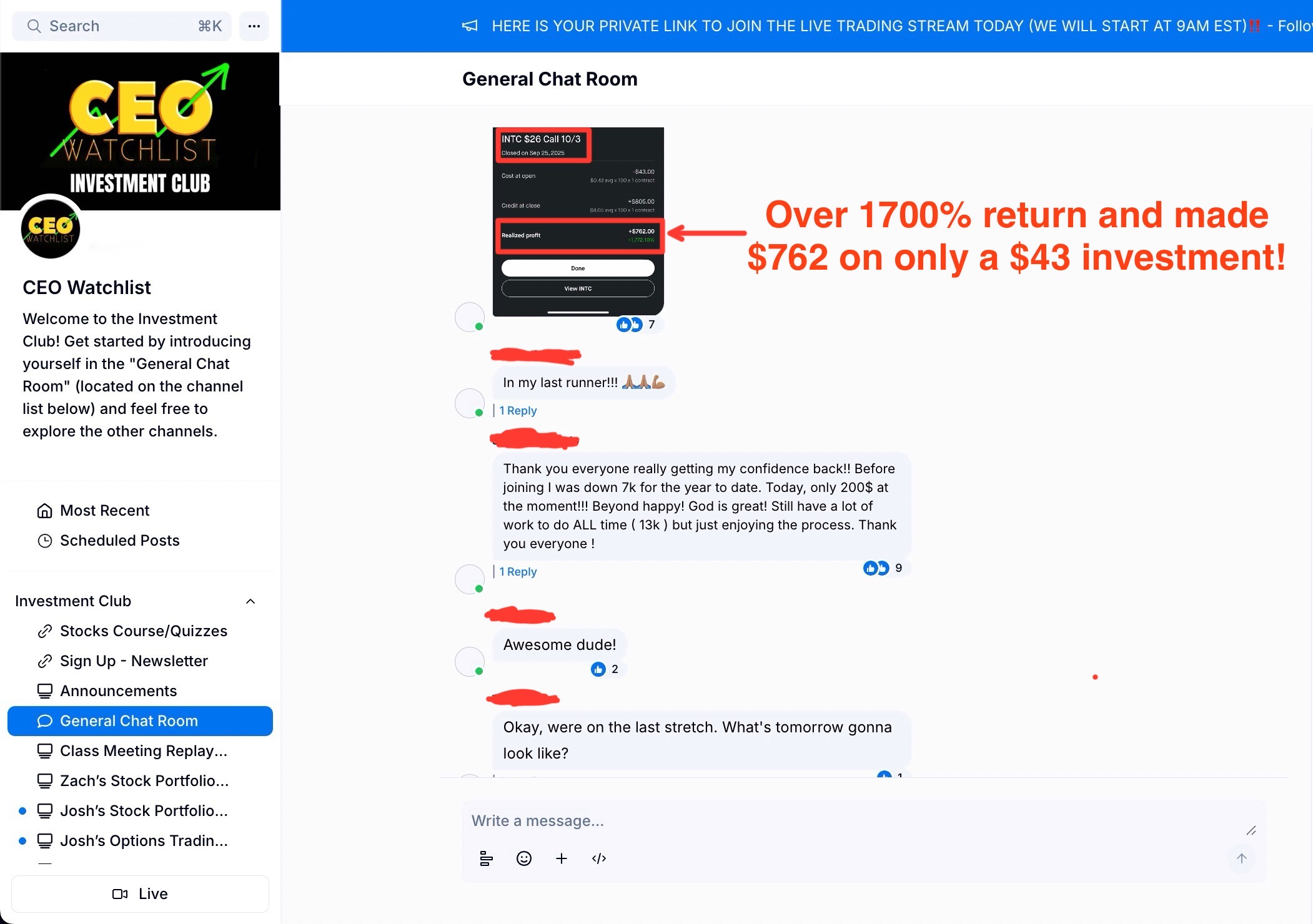

And it wasn’t just me. Our students in the Investment Club are seeing the same kind of success. As we showed in last week’s newsletter, many of them have scored returns ranging from 100% to over 5,000% on single trades. One student even turned ~$20 into roughly $1,300 in a single day. This week is no different. One of our other students put up an impressive 1,772% gain in a single trade, turning $43 into $805 ($762 of profit):

This is why it's important to learn how to invest, because once you learn how to spot the opportunities in the stock market, making the money becomes a lot easier. That's why when people ask us, "Do I need a lot of money to get started?" we always point them to our students who are able to make trades like this, which cost them less than a night out at dinner. So, if you’re tired of watching opportunities like this pass you by, now is the time to get in the game. As a thank you for being a subscriber of ours, we’re offering you [$200 OFF] when you join the Investment Club today. [CLICK HERE] to secure your spot, learn the exact strategies we use, and maybe even become the next student we feature for landing a 10X trade!

"Super Investor" Spotlight: Chris Hohn (Source)

Stocks mentioned: $GE, $MSFT, $V, $MCO, $SPGI, $CP, $GOOGL, $CNI, $FER

When we talk about “Super Investors,” we’re talking about a very rare breed: portfolio managers whose track records, discipline, and conviction separate them from the crowd. They’re not just managing millions; they’re moving billions, and their trades often provide a roadmap for where capital is flowing next. Watching their filings, especially the quarterly 13F reports that reveal their stock holdings, gives everyday investors a chance to sit in the passenger seat of some of the best financial minds of our time.

Chris Hohn is one of those minds. Founder of The Children’s Investment Fund (TCI), Hohn has built a reputation as one of Europe’s most formidable activist investors. With over $50 billion in assets under management, he’s known for taking concentrated bets and forcing change at the world’s biggest companies. His long-term track record? Outstanding. Since launching TCI in 2003, Hohn has compounded capital at double-digit rates while consistently ranking among the most influential voices in global markets.

According to his most recent 13F filing, here are the stocks he owns:

- General Electric (GE) – 24.1%: His single largest holding. The recent spinoffs in aviation, healthcare, and energy are unlocking value, and Hohn is positioning GE as a global industrial champion.

- Microsoft (MSFT) – 17.2%: A core anchor in enterprise software and cloud computing. This position reflects Hohn’s belief in the durability of Microsoft’s ecosystem and its role as one of the most powerful platforms in the digital economy.

- Visa (V) – 13.4%: The world’s largest payment network. Hohn’s bet on Visa underscores the long-term secular trend toward cashless payments and the company’s unrivaled scale.

- Moody’s (MCO) – 13.1%: A leader in credit ratings and analytics. Alongside S&P Global, this position gives Hohn exposure to a near-duopoly with recurring revenue and strong pricing power.

- S&P Global (SPGI) – 11.5%: A powerhouse in financial data, indices, and benchmarks. Together with Moody’s, it highlights Hohn’s conviction in financial infrastructure as a long-term wealth compounder.

- Canadian Pacific Kansas City (CP) – 8.3%: A dominant North American railway. This position aligns with Hohn’s strategy of owning hard-to-replicate infrastructure that moves the backbone of the economy.

- Alphabet (GOOGL) – 5.6%: Parent of Google, spanning search, ads, YouTube, and cloud services. A smaller but still meaningful position that provides exposure to global digital advertising and AI.

- Canadian National Railway (CNI) – 4.7%: Another critical North American railway. Hohn clearly views railroads as irreplaceable assets in an era of growing supply chain and logistics demand.

- Ferrovial (FER) – 2%: A Spanish multinational specializing in infrastructure and toll roads. While the smallest position in the portfolio, it reinforces Hohn’s steady bet on essential global infrastructure.

Notice the structure: Hohn doesn’t spread himself thin. Instead, he concentrates capital in a handful of global leaders across industrial infrastructure, financial services, and technology. That concentration magnifies both upside and downside, but it also reflects extreme conviction, a hallmark of true "Super Investors" like his colleagues Bill Ackman and Dev Kantesaria (who we featured in last week's newsletter).

For retail investors, the lesson is clear: Chris Hohn doesn’t chase hype cycles; he doubles down on global franchises that control choke points in the economy, whether it’s Visa in payments, Microsoft in enterprise software, or railroads like CP and CNI in transportation. His selective trimming of smaller infrastructure and financial names underscores that his focus remains on dominant, scale-driven moats rather than speculative plays. In a market where dispersion is widening, that kind of concentration in quality could be exactly what wins over the next decade.

INSIDER TRADES FROM THE WEEK:

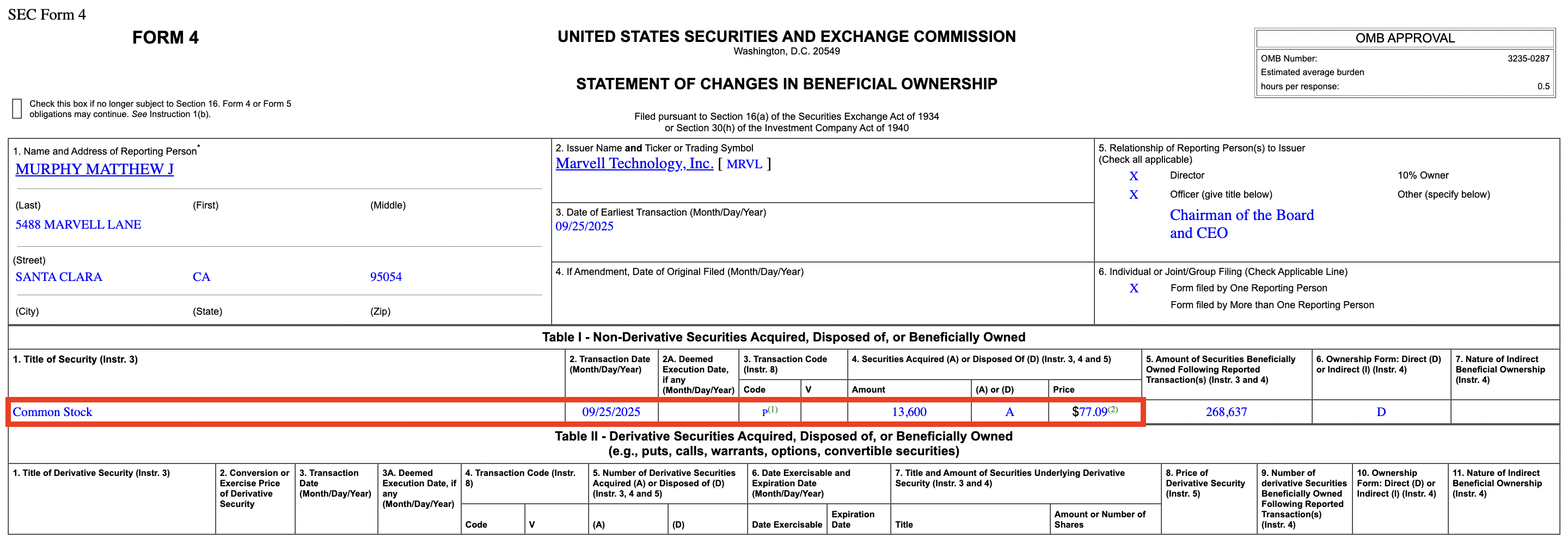

1. Marvell Technology, Inc. (MRVL) - Matthew Murphy, CEO and Chairman of the board, bought ~$1,000,000 of MRVL stock on Sep 25, 2025, and it was reported later the same day. Also note that multiple other insiders are also purchasing MRVL stock at a similar price. (Source)

2. Global Partners LP (GLP) - A General Partner bought ~$1,000,000 of GLP between Sep 23-24, 2025, but it was most recently reported to the public on Sep 25, 2025 (Source)

3. Worthington Enterprises, Inc. (WOR) - Michael Endres, Director, bought ~$529,000 of WOR stock on Sep 25, 2025, but it was most recently reported to the public on Sep 26, 2025 (Source)

Over 2,000 people have already signed up for my FREE Masterclass video on how to unlock my exact strategies for finding winning stock/options trades! I'll share everything including how to find what Politicians and CEOs are buying. Don’t miss your chance to get in for FREE before spots fill up!

INFOGRAPHICS FOR THE WEEK:

CONTACT US: [email protected]

Responses