TOP NEWS AFFECTING THE STOCK MARKET THIS WEEK:

-

Wall Street’s Make-or-Break Moment Hinges on One Stock: Nvidia! (Source)

Stocks mentioned: $NVDA, $AMZN, $MSFT, $TSLA, $PDD, $CRWD, $PANW, $SNOW

Wall Street is stressing over this Wednesday's earnings. Nvidia’s (NVDA) earnings aren’t just another quarterly update, they’re the main event, the pay-per-view showdown that could determine how the entire tech sector performs into the end of the year. With seasonality data pointing to weakness in late August and September, a strong beat-and-raise from Nvidia could flip the script entirely. But if they miss? It would ignite a broad-market selloff and shatter the recent run-up we've had in this AI-fueled rally. This isn’t just a single stock story, it’s a macro turning point.

Let’s zoom out. Last year, the tech-led rally in 2024 was built on two things: AI euphoria and earnings resilience. Nvidia has been the tip of the spear. But now, market breadth is thin, megacaps are stretched, and the bears are itching for the spotlight. The last line of defense? Nvidia. Despite that, it remains the most fundamentally sound of the AI giants. According to Fundstrat and Bloomberg, Nvidia is projected to generate more net income over the next 12 months than any company in the index, including Amazon (AMZN), Microsoft (MSFT), and Tesla (TSLA).

And yet, its forward P/E multiple, our preferred valuation metric, doesn’t even crack the top 50 most expensive stocks in the S&P 500. So, for the critics saying that Nvidia is in a bubble and this is exactly like the dot com crash, we would push against that point by saying fundamentals have never been stronger, and although valuations are elevated, they are not in bubble territory yet. Today, Nvidia trades at a forward P/E of 40. For reference, the forward P/E of the higher quality tech names during the dotcom bubble was around 60 foward P/E. That means currently, assuming all else the same, we still have a 50% upside until we get closer to those numbers.

Here’s why all this matters: Nvidia’s results will be the litmus test for whether AI spending is accelerating or plateauing. And depending on their results, it will either lead the growth and tech sector higher into the end of the year or mark this week as a potential top in the stock market. Now although Nvidia's going to be the star this week that everyone is paying attention to, we do have a few other stocks on our radar. Those stocks include:-

PinDuoDuo (PDD) – The parent company of Temu, has seen "Super Investors" actively trading its stock, signaling high conviction in its global e‑commerce growth trajectory. With its earnings being released on Monday, investors should focus on whether Temu continues to fuel international expansion and whether margins are stabilizing amid rising expenses, uncertainty around tariffs, and stiff competition. We prefer owning Amazon (AMZN) over PDD because we believe it offers a better risk-to-reward opportunity. Also, Amazon has a more diversified business model into growing sectors such as: robotics and cloud.

-

CrowdStrike (CRWD) – A cybersecurity leader expected to benefit from AI-driven threat detection. Strong annual recurring revenue (ARR) and margin expansion will suggest cloud software resilience. We believe Crowdstrike will have a great quarter as they are one of our top picks for cyber security. Based on earnings from Palo Alto Networks (PANW), who just reported a double-beat and raise on guidance, we expect similar results for Crowdstrike on Wednesday when they report. Crowdstrike is down roughly -20% from its all time high, which signals its already sold off into this earnings report. This pre-earnings sell off normally makes it easier for stocks to rally if they can report even a small beat and raise on guidance.

-

Snowflake (SNOW) – A data infrastructure player whose consumption-based model will tell us whether customers are actually putting AI tools to use. Snowflake has struggled since its initial public offering (IPO), but with its recent earning reports, it has gained some positive traction. We believe there is a high likelihood that they will have a strong quarter, but then again, because they report on Wednesday after the close, if Nvidia doesn't do well, it will take names like Snowflake down with it...whether or not Snowflake had a good or bad quarter.

Needless to say, this next week we have some very important stocks reporting earnings, but they can easily be overshadowed by the reaction from Nvidia's report. The good news is we believe Nvidia has a strong chance of beating earnings, therefore there's a low likelihood of a major negative reaction in the market. Layer in endorsements from top analysts like Dan Ives and Tom Lee, plus the fact that even politicians like Nancy Pelosi are still holding positions in Nvidia, and it becomes clear that institutional conviction is still abundant, even near all-time highs for the stock. That tells us this isn’t euphoria peaking, this is inning two of a long bull market in AI.

If Nvidia delivers, it could provide the thrust needed to push through seasonal headwinds and ignite a year-end melt-up. If they don’t, the air comes out of the balloon fast. Either way, this is the most consequential earnings event of the year. The crowd is watching. And at CEO Watchlist, we’ll be covering it LIVE, breaking it all down for our Investment Club members the second it hits. Buckle up for a wild week! -

-

Powell Finally Caves: Rate Cuts Coming ... 3 Overlooked Winners Nobody Is Talking About!!! (Source)

Stocks mentioned: $FICO, $EFX $HD

The market has spent two years obsessing over inflation and the Fed Chair, Jerome Powell, and his every word. Every Powell speech was parsed for hints of hawkishness, every CPI print became a referendum on monetary credibility. Powell has been at war with President Trump, and most of Wall Street, due to him and the Fed not wanting to cut interest rates. For those that don't know, markets tend to go up when interest rates come down. And markets tend to go down when interest rates go up. Needless to say, that's why most of Wall Street, and President Trump, have been pressuring Powell to cut rates. Powell has refused, citing concerns over inflation not being under control, but all of that changed on Friday.

Friday marked a fundamental regime shift: for the first time in this tightening cycle, Powell is acknowledging that the risks have flipped. Inflation may not be dead, but the greater threat now lies with the labor market. At Jackson Hole, on Friday, Powell finally acknowledged that there is now a shifting balance of risks that "may warrant adjusting policy". Implying that not cutting rates because of inflation may no longer be their core policy stance. Instead, this new "policy" will probably focus on lowering rates to improve the warning signs we're seeing in the labor market.

You may be asking yourself, "Why is this important?" It's important because when the Fed is worried about inflation, they tend to increase interest rates. But if the Fed wants to protect the labor market and jobs, historically, the way you do that is by lowering rates. As mentioned earlier, in the article, lowering interest rates tends to make the market go higher and that's why this hint at a shift in policy is a major market event that led stocks much higher on Friday. That pivot by Powell, though subtle in tone, seismic in implication, sets the stage for the first rate cut in September. Markets are already moving higher, but the real opportunity lies not in the obvious mega-cap tech winners, but in the companies that are structurally wired to benefit most from falling rates.The macro-thesis is straightforward. When rates decline, credit creation expands, housing activity rebounds, and consumer balance sheets loosen. That rising tide doesn’t lift all boats equally, it accelerates businesses that sit directly on the fault lines of credit access and housing demand. Today, three companies in particular stand out. Each sits at a different choke point in the credit and housing ecosystem, and each is positioned to disproportionately benefit from even a modest easing cycle. These 3 stocks are:

-

Fair Isaac Corp. (FICO) - FICO’s moat is its score, the industry standard that underpins virtually every consumer credit decision in the U.S. Roughly half of its revenue comes directly from credit scoring, with the rest coming from software analytics. The controversy around recent price hikes has weighed on the stock, causing it to be down by over 25% year-to-date. But that pessimism misses the larger picture: volumes. When mortgage and auto lending pick up in a lower-rate environment, the number of FICO scores requested surges. Volume growth in a monopoly-like business model means operating leverage, higher cash flow, and a re-rating of the stock. In short, the headwind of regulatory scrutiny is real, but the tailwind of normalized credit demand is far more powerful. That's why, when we get rate cuts, FICO will be one of the biggest winners!

-

Equifax (EFX) - Unlike FICO, Equifax has diversified away from pure credit inquiries into employment verification and workforce analytics. That diversification is precisely why the company is generating record free cash flow today despite mortgage inquiries sitting at half their historical average. But the real upside comes if credit activity normalizes. During the 2020–2021 refinancing boom, Equifax’s cash flow spiked alongside mortgage activity. Today, volumes are depressed, yet cash generation is at all-time highs, a setup that creates asymmetric upside. Rate cuts catalyze both sides of Equifax’s business: more credit pulls as mortgage rates ease, and stronger labor demand that drives its workforce solutions unit. That's why Equifax is basically in a win-win situation here. It also doesn't hurt that, due to regulations, they have taken a small market share away from FICO. We believe that both FICO and EFX are both beneficiaries of rate cuts and can rally, massively, as we begin to get them.

-

Home Depot (HD) - If FICO and Equifax benefit from the origination side of credit, Home Depot benefits from the end demand it unlocks. Lower mortgage rates don’t just drive transactions, they trigger home renovations, remodels, and consumer spending on housing improvements. Home Depot’s scale, logistics, and brand trust make it the default beneficiary of renewed housing activity. Even modest relief in financing costs can unleash deferred demand from households that have been sidelined by affordability pressures. For a retailer that thrives on durable, credit-sensitive purchases, rate cuts represent the oxygen that reignites growth, making this yet another winner when we get rate cuts.

Skeptics will argue that Powell may be bluffing, that inflation could re-accelerate, or that the Fed’s credibility constrains its ability to ease meaningfully. Those risks are real. But markets don’t move on perfection, they move on probabilities. With futures pricing in a 90% chance of a September cut, the marginal bet is whether the market has fully priced in the second-order effects. It hasn’t.

The pivot from an inflation-focused Fed to a labor-focused Fed is not just semantics, it is policy gravity. Rate cuts are coming, and when they do, the companies most levered to credit volumes and housing demand will move first and fastest. FICO, Equifax, and Home Depot aren’t just cyclical plays, they are choke-point assets in the credit and housing value chain. The opportunity is inevitable, underpriced, and closer than the market believes.

Stock trading is already hard enough as it is for beginner investors, but then when you have to track all these macro-economic events that keep creating volatility in the market, it can get extremely overwhelming. That’s exactly why we, at CEO Watchlist, track all the important news and events, on a daily basis, and report it to our students in the Investment Club. This way they don't have to worry about spending hours a day, everyday, to find where the next opportunity is in the market, especially since most people have to work a 9-5 job. Speaking of opportunities in the market, we just put out an updated report on the new stocks we bought and sold this week in preparation for rate cuts. If you are an Investment Club Member, make sure to CLICK HERE to log in and check out our updated "Stock Portfolio Update" and "Option Portfolio Update" channels. If you're not yet an Investment Club Member, you shouldn't just join because we share all of our stock and option portfolios, but moreso because of all the other services we provide in the Investment Club. We do live trading with our students Monday through Friday, in real time, as well as hold conference calls with our Club Members every week to cover stocks that Politicians, CEOs, and "Super Investors" are buying. In addition, we have an entire vault of videos/quizzes to simplify investing in the stock market, which is why everybody, even at a beginner level, can join the group and start picking this up on Day 1. What we share in this newsletter is just a small fraction of what we share with the CEO Watchlist Investment Club Members, so if you are ready to take that next step, then CLICK HERE to join the Investment Club today and because you are joining through our newsletter, we are granting you $200 OFF your subscription permanently for as long as you decide to stay with us. Don’t wait, CLICK HERE to claim your spot now and join the 1000's of others who have joined the CEO Watchlist Investment Club! -

-

"Super Investor" Spotlight: Michael Burry, The Housing Crisis Oracle! (Source)

Stocks mentioned: $BABA, $BIDU, $NVDA, $UNH, $REGN, $LULU, $META, $EL, $JD, $ASML, $VFC, $BRKR, $MELI

A “Super Investor” is a rare breed, someone whose track record shows the ability to consistently find opportunities others miss and to act with conviction before the crowd catches on. These investors, often managing billions, set the tone for markets by showing where the smartest money is moving. This week’s spotlight shines on Michael Burry, one of the most controversial and closely watched money managers of our time. Famous for calling the 2008 housing collapse years before it unraveled, which made him and his clients upwards of $700 million! Needless to say, this was one of the greatest investments of all time by any money manager. It was so great in fact, that there was an Oscar award-winning movie made about him called "The Big Short", and personally, one of the greatest financial movies I've ever seen (highly recommend watching it). Beyond the fame, Burry has built a reputation as a contrarian investor who isn’t afraid to go against Wall Street’s consensus. His trades are often volatile, he moves in and out of positions quickly, but they consistently reflect deep conviction and a sharp read on macroeconomic trends. He looks for beaten-down companies or industries trading below intrinsic value, a style inspired by Benjamin Graham’s value investing framework, but isn’t afraid to make macro calls that go against the norm. And with his latest 13F filing, he’s once again making bold moves that have the market’s attention.

In his most recent 13F filing for Q2 2025, Burry executed a sharp pivot from bearish to bullish positioning. Earlier this year, his portfolio was stacked with put options against tech giants and Chinese equities like Alibaba (BABA), Baidu (BIDU), and Nvidia (NVDA). By Q2, he had exited all of those bearish bets and replaced them with more than $500 million in bullish call options and stocks. Notable new positions included:

-

UnitedHealth Group (UNH) – Diversified health insurer which has been very popular among "Super Investors" this quarter. The stock is down 50% from its all time highs. Burry owns both call options and stock.

-

Regeneron Pharmaceuticals (REGN) – Biotech stock with a rich drug pipeline. The stock is down over 50% from its all time highs. Burry owns both call options and stock.

-

Lululemon (LULU) – Athleisure apparel company with global demand. The stock is down 60% from its all time highs. Burry owns both call options and stock.

-

Meta Platforms (META) – Digital advertising and social media powerhouse that's trading at a low valuation relative to its peers. Burry only owns call options.

-

The Estée Lauder Companies (EL) – Cosmetics giant that is down over 75% from its highs. Burry owns both call options and stock.

-

JD Inc. (JD) – Leading Chinese e-commerce platform that is down over 60% from its highs. Burry only owns call options.

-

Alibaba Group (BABA) – China's number one e-commerce and tech giant. The stock is down 60% from its all time highs. Burry only owns call options.

-

ASML Holding (ASML) – Monopoly in advanced semiconductor lithography and is trading at some of its lowest historical values. The stock is down 30% from its all time highs. Burry only owns call options.

-

VF Corporation (VFC) – Outdoor/apparel conglomerate and is down over 80% from its all time high. Burry owns only call options.

-

Bruker (BRKR) – Scientific instruments and diagnostics company, down over 60% from its highs. Burry only owns stock.

-

MercadoLibre (MELI) – Latin America’s e-commerce and fintech leader, and is similar to Amazon. Burry only owns stock.

What’s striking here is not just the diversity but the narrative behind the shift. By exiting bearish positions, most notably his puts on Chinese tech and Nvidia, Burry has removed the downside hedges that defined his positioning earlier in the year. Instead, he is leaning into healthcare and biotech, where aging demographics and constant demand make earnings resilient. He’s targeting consumer brands like Lululemon and Estée Lauder, signaling belief in the durability of consumer spending even under economic uncertainty. He’s betting on tech giants like Meta and ASML, a clear nod to the structural growth drivers in AI and semiconductors. And in perhaps his boldest stroke, he’s re-engaged with Chinese names like JD and Alibaba, but through calls, giving himself upside exposure without the unlimited risk of outright ownership in a volatile regulatory environment.

We've been very critical of Burry in the past, as he tends to shy away from growthy-tech names, which makes sense since he does tend to prefer value investing. So we can appreciate Burry taking some large positions in companies like META and ASML, two companies we really like at CEO Watchlist for many years to come. We still disagree with his overwhelmingly contrarian style of investing, in which he's buying companies that are extremely distressed currently. We just believe that there's a reason those companies are down over 50% from their highs and prefer to stick with the winners who have continued to lead this market higher. One of his contrarian plays that we actually like is UNH. We have discussed UNH in our past newsletters for months now, pounding the table on it as a great value buy. Currently the stock is up over 20% from where we've bought it, but we still believe UNH offers an asymmetric upside bet at its current valuation.

Whether or not you agree with Burry's style of investing, the lesson for retail investors is clear. Flexibility matters more than dogma. Burry didn’t stay bearish out of pride; he flipped when the facts changed. He diversified across sectors but kept the portfolio tight and intentional. He used calls as a tool to manage risk and reward, not as a gamble. And he demonstrated how to think globally, pairing U.S. healthcare and tech with international e-commerce leaders. This portfolio isn’t just a snapshot of Burry’s conviction, it’s a roadmap for how to adapt, take asymmetrical bets, stay diversified and keeping ahead of the market narrative.

In short, Michael Burry’s latest filing shows why he remains one of the most important investors to track. Although volatile, his Q2 2025 pivot from defense to offense highlights a rare ability to abandon yesterday’s strategy in pursuit of tomorrow’s opportunity. He cut his losses, pressed his winners, and spread his exposure across themes that matter: healthcare resilience, consumer strength, AI and semiconductors, and selective global growth. It’s a masterclass in conviction with discipline, and for anyone trying to navigate this market, Burry’s playbook offers a clear, urgent reminder: the best investors are always willing to change their minds.

-

INSIDER TRADES FROM THE WEEK:

1. Madrigal Pharmaceuticals (MDGL) - Baker Bros Advisors, 10% owner of the company, bought ~$36 million of Madrigal Pharmaceuticals stock on August 18-20, 2025, and it was most recently reported to the public on August 20, 2025. (Source)

2. Energy Transfer (ET) - Warren Kelcy, Director, bought ~$34 million of Energy Transfer stock between August 19-20, 2025, but it was reported to the public on August 21, 2025. (Source)

3. Elevance Health (ELV) - Susan DeVore, Director, bought ~$347,000 worth of ELV stock on August 19, 2025, but it was reported to the public on August 21, 2025. (Source)

Over 2,000 people have already signed up for my FREE Masterclass video on how to unlock my exact strategies for finding winning stock/options trades! I'll share everything including how to find what Politicians and CEOs are buying. Don’t miss your chance to get in for FREE before spots fill up!

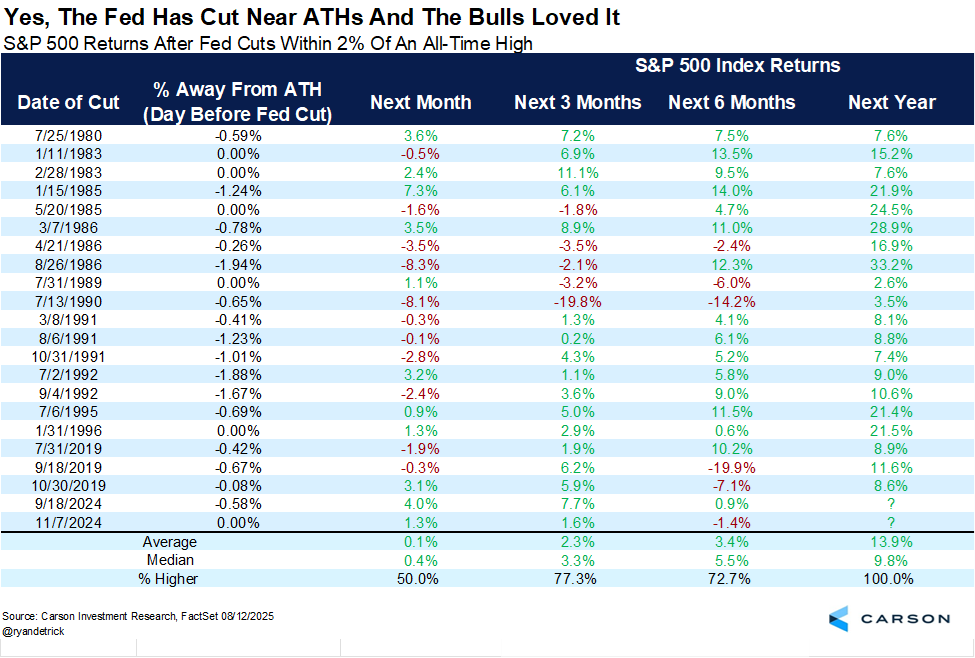

INFOGRAPHICS FOR THE WEEK:

CONTACT US: [email protected]

Responses