TOP NEWS AFFECTING THE STOCK MARKET THIS WEEK:

-

Warren Buffett's Secret Stock Jumped Over 20% This Past Week Alone!!! (Source)

Stocks mentioned: $BRK.B, $UNH, $CVX, $STZ, $POOL, $NUE, $LEN

Last week in our newsletter, we flagged the growing rumors that Warren Buffett’s, Berkshire Hathaway (BRK.B), was quietly accumulating shares of UnitedHealth Group ($UNH). At the time, this was an educated guess based on attractive valuations, it being an insurance stock that Buffett tends to gravitate towards historically, the fact that he owned UNH back in 2006, and finally all the insider/political/"Super Investor" buying activity over the past couple months. All of this led us to believe that UNH was the most likely candidate to be Buffett's secret stock he was buying. On Thursday, the truth came out: Buffett’s new undisclosed stock buy was indeed UNH. This confirmation is critical because it validates the signals we’ve been tracking for months within the CEO Watchlist Investment Club and sets the stage for what could be one of the highest-conviction healthcare investments of the next few years.

Why is this purchase so significant that the stock rallied 12% on Friday? The reason is because Buffett doesn’t make new bets lightly. Historically, his new positions start at 0.1% or less of Berkshire’s portfolio, but this time, his UNH purchase was over six times that size. That’s not a dabble, it’s a declaration that he's serious about building this position. UNH wasn’t just another line item alongside his other new buys like Chevron ($CVX), Constellation Brands ($STZ), Pool Corp ($POOL), Nucor ($NUE), and Lennar ($LEN). It was the headline move. And when Buffett makes a statement-sized position, investors should pay attention. Add to this the fact that UNH’s valuation has compressed dramatically, trading at levels not seen in years, and the setup looks eerily similar to past moments when Buffett quietly bought into cyclical lows.

What’s striking, and what virtually no one else in financial media has pointed out, is that this isn’t Buffett’s first time owning UnitedHealth. Like we mentioned in last week's newsletter, back in 2006, Buffett began building a UNH position that grew into nearly $300 million by 2008. He exited with a 379% gain in just two years. That playbook should sound familiar: identify a high-quality insurer trading at distressed valuations, scale in aggressively, and ride the rebound. If history rhymes, Buffett’s re-entry could mark the beginning of another massive upcycle for UNH. Given the stock is still down over 50% from its highs, there still seems to be a lot of room to run to the upside, even after its 12% pop on Friday. It also doesn't hurt that UNH pays you roughly a 3% dividend just to hold it in the meanwhile.

Skeptics will argue that healthcare faces enormous political risk: regulatory scrutiny, election-year uncertainty, and rising cost pressures could all weigh on margins. That’s valid. But UNH is not a speculative biotech, it’s a diversified healthcare giant with scale, infrastructure, and a balance sheet that gives it room to maneuver. Moreover, for the people that argue that UNH is facing a ton of political risk and regulatory issues, we would like to point those people to all the politicians, Republicans and Democrats, that have been buying this stock up alongside Buffett, CEO's, and all the other "Super Investors". It makes it really hard to ignore the bull case when every single major investor seems to be buying this stock while it's still down 50% from its highs. Markets are forward-looking, and the confluence of buyers suggests that the worst may already be priced in.

Here’s the final takeaway: Buffett’s UNH purchase isn’t just another trade, it’s a rare, high-conviction signal in a frothy market where real value is scarce. The stock’s swift 20% move in under a week demonstrates just how underpriced it was when we flagged it in last week's newsletter, and we continue to believe another 20% upside in the short to medium term is realistic. For patient investors, the parallels to Buffett’s 2006 entry are too strong to ignore. In a market searching for what’s next, UnitedHealth isn’t just a defensive healthcare play, it’s shaping up to be one of the few inevitable winners hiding in plain sight.

Warren Buffett wasn’t the only one ahead of the curve. When Buffett was secretly building his position in UnitedHealth, our Investment Club Members had already spotted the opportunity and many of them are celebrating incredible wins this past week because of it. That’s the power of being part of the CEO Watchlist Invesment Club, a community that gets early access to all of our research, stock watchlists, real-time stock portfolio updates, and our option/stock strategies. If you’re not inside the Club yet, you’re missing the chance to see these ideas before they hit the headlines. Don’t sit on the sidelines while others are cashing in. It's time to invest in yourself! CLICK HERE to claim your $200 OFF discount code, available today, and step inside the Investment Club before the next big move happens.

-

Earnings Season Week 6 Is Here! 3 Stocks We're Watching! (Source)

Stocks mentioned: $CRWV, $NBIS, $DE, $AMAT, $ASML, $LRCX, $KLAC, $PANW, $CRWD, $MSFT, $HD, $INTU

-

"Super Investor" Spotlight: David Tepper, The Billionaire of Appaloosa! (Source)

Stocks mentioned: $UNH, $TSM, $INTC, $RTX, $AMZN, $FXI, $BABA, $JD, $BIDU, $PDD, $WYNN, $LVS

INSIDER TRADES FROM THE WEEK:

1. Bausch Health (BHC) - John Paulson, Director, bought ~$312,000,000 of BHC stock on August 14, 2025, and it was reported to the public later that same day. (Source)

2. Alkami Technology (ALKT) - General Atlantic, 10% owner of the company, bought ~$30,000,000 worth of ALKT stock between August 11-13, 2025, and it was most recently reported to the public on August 13, 2025. (Source)

3. Eli Lilly (LLY) - David Ricks, CEO, bought ~$1,000,000 of LLY stock on August 12, 2025, and it was reported to the public later that same day. (Source)

Over 2,000 people have already signed up for my FREE Masterclass video on how to unlock my exact strategies for finding winning stock/options trades! I'll share everything including how to find what Politicians and CEOs are buying. Don’t miss your chance to get in for FREE before spots fill up!

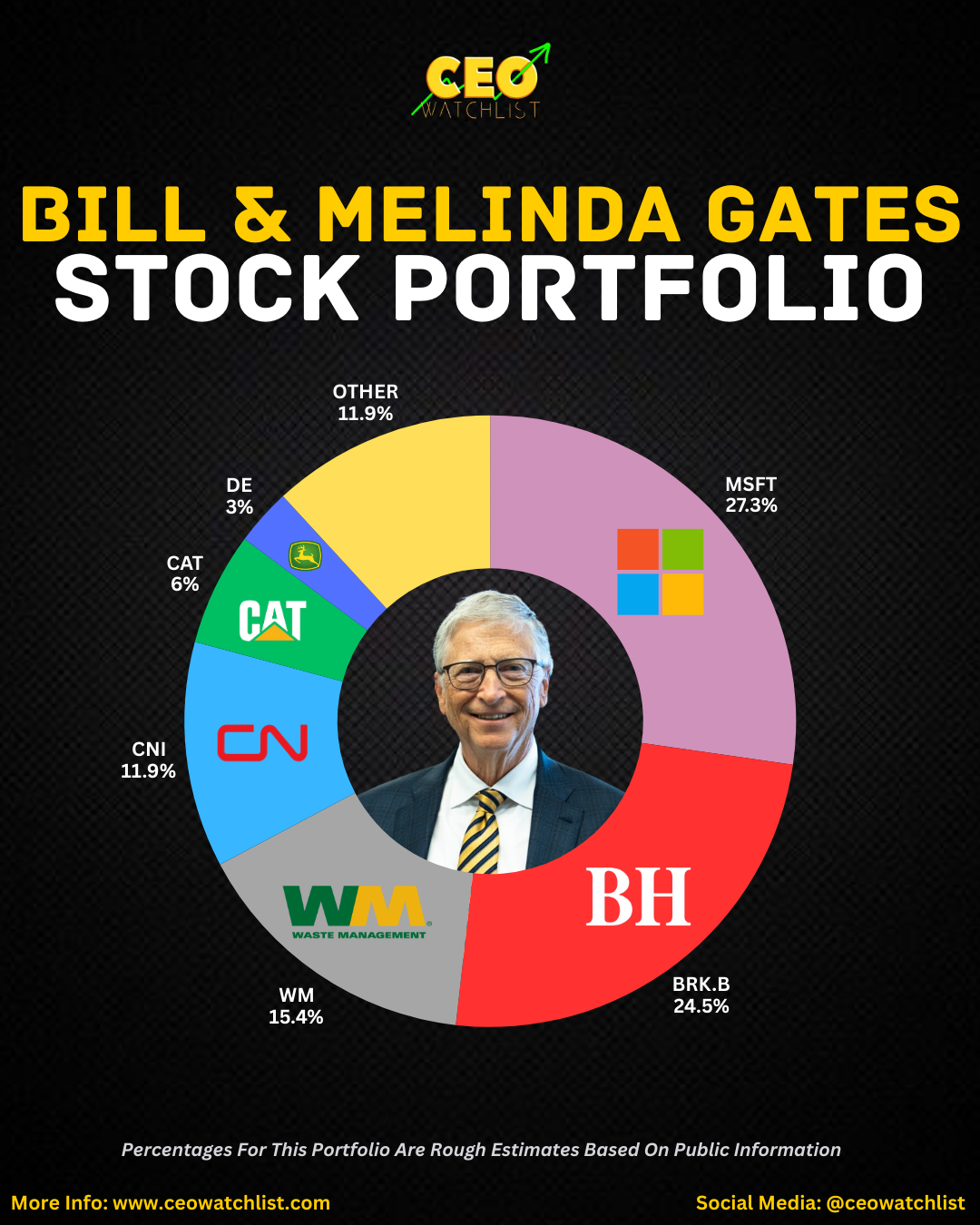

INFOGRAPHICS FOR THE WEEK:

CONTACT US: [email protected]

Responses