TOP NEWS AFFECTING THE STOCK MARKET THIS WEEK:

Major Shakeup Amongst Data Center Tech Names ... Here's The One Stock We Think Could Be A Buy... (Source)

Stocks mentioned: $META, $MU, $CRWV, $IREN, $NBIS

For most of 2026, Meta (META) has been the odd one out among the big tech giants, lagging the broader market while a name like Micron (MU) has soared. The reason was simple: spending. Meta has been pouring an almost incomprehensible amount of money into AI, raising its 2026 capital expenditure guidance to between $125 billion and $145 billion, nearly double the roughly $72 billion it spent the year before. Investors were rattled, because when a company spends that aggressively, the natural question becomes "where's the return?" That anxiety weighed on the stock all year, leaving it down more than 11% on the year while the S&P 500 climbed. So Meta was sitting in the penalty box, punished for spending without a clear payoff in sight. Then Wednesday happened, and the whole narrative flipped in a single afternoon.

On Wednesday, July 1, a report leaked (via Bloomberg) that Meta is building a cloud business to sell its excess AI computing power, essentially renting out the spare capacity in its massive data centers to outside customers. This is a big deal, and here's why it matters so much. Investors have spent all year worried that Meta's enormous spending was a black hole with no obvious way to generate a return. Selling compute changes that calculus entirely, because it turns idle infrastructure (a sunk cost) into an actual revenue stream. It's like a company that built a giant warehouse for its own goods realizing it has empty shelves it can lease out to other businesses for cash. The market loved it. Meta's stock shot up over 10% intraday and closed up roughly 8.8%, one of its strongest single-day gains of the year. And here's the subtle but powerful second implication: if Meta has enough compute to sell, that might mean it's approaching the point where it has enough for itself, which could eventually mean cooling off some of that scary capex. Think about it: a company either buys and builds because it doesn't have enough, or it sells because it has more than it needs. This leak nudged investors toward the more optimistic read.

But every action has an equal and opposite reaction, and this one hit the "neocloud" sector hard. Neoclouds are the specialized companies whose entire business is renting out AI computing power, names like CoreWeave (CRWV), IREN (IREN), and Nebius (NBIS). If Meta, one of the biggest customers and deepest pockets in the world, suddenly becomes a competitor selling the same thing, that's a direct threat to their turf. The stocks got hammered. CoreWeave dropped about 14%, and Nebius was the hardest hit of all, cratering over 17% in a single day to close around $229 per share. The fear was straightforward: a well-funded giant crashing into the neocloud space could squeeze pricing and steal customers. Here's where we part ways with the panic, though. In our view, Nebius is a phenomenal long term hold. We think we give this a couple days to shake out like it did last week, and look for buying opportunities this week in the name. The fundamentals of the company remain rock solid: Nebius reported first-quarter revenue of $399 million, up a staggering 684% year over year, and none of Wednesday's damage touched its actual operating results or its guidance. The demand for compute isn't disappearing; it's still exploding. The selloff was a repricing of fear, not of the business itself.

So let's bring it all together. Meta spent the year in the doghouse for its enormous AI spending, then a Wednesday leak revealed plans to sell excess compute, which reframed that spending as a potential revenue engine and sent the stock surging over 10% intraday before closing up nearly 9%. That same news crushed the neocloud names, with Nebius plunging 17% on competition fears, a move we think will become a buying opportunity soon, its 684% revenue growth, and the delicious irony that Meta is one of its largest contracted customers. Our take: we love Meta as a long-term pick, since it's one of the cheapest growth names in the entire market, and the ability to sell excess compute gives it valuable optionality, exactly the kind of flexibility we like to see in a business. And we still believe Nebius is the strongest neocloud play of the bunch, stronger than CoreWeave and the rest, offering the best risk-to-reward for investors who can stomach the swings. When the market panics over a product that hasn't launched and forgets the contracts already signed, that's usually the moment worth paying attention to.

OpenAI Wants to Hand Uncle Sam 5% of the Company. Here's the 3 Stocks We Think Can Benefit... (Source)

Stocks mentioned: $GOOG, $META, $INTC, $NVDA, $MRVL, $QCOM, $PENG

This past Thursday, July 2, the Financial Times reported that OpenAI, the company behind ChatGPT and arguably the most important AI lab in the world, has proposed giving the U.S. government a 5% equity stake in the company. To put a number on that, OpenAI was recently valued at a staggering $852 billion, so a 5% slice would be worth roughly $42.6 billion. CEO Sam Altman has framed this publicly as "a way to let the American public share in the upside of AI", and the pitch reportedly goes even further, suggesting that other major AI developers like Google (GOOG), Anthropic, and Meta (META) contribute matching 5% stakes into a kind of sovereign wealth fund, modeled loosely on the Alaska Permanent Fund that pays out oil dividends to Alaskans. The talks are still early and "conceptual," and it's unclear whether any rival would sign on, but the mere fact that the leading AI company is offering to make the government a part-owner is a historically controversial move. So the obvious question is: why would OpenAI voluntarily give away $42 billion worth of equity? That's where the theories gets interesting.

Before we get to the "why," let's talk about what happens historically when the government takes a stake in a company, because the track record is eye-popping. The clearest example is Intel (INTC). Back in August 2025, the Trump administration took a roughly 10% stake in the struggling chipmaker, buying 433.3 million shares at $20.47 apiece. What happened next was extraordinary: Intel's stock has surged roughly 494% since the government bought in. Let that sink in, the stock nearly 5X'd after Uncle Sam became a shareholder. Now, we have to be fair here and note the rebuttal, because correlation isn't causation. Intel's run wasn't purely because the government showed up; it rode a massive wave of AI infrastructure spending, a $2 billion SoftBank investment, and an Nvidia (NVDA) partnership too. So government ownership wasn't the only rocket fuel. But the pattern is hard to ignore: when Washington puts its own money and credibility on the line, it sends a powerful signal to the market that this company has a friend in a very high place, and investors tend to pile in behind that signal.

Here's our read on the real motivation, and it's the crux of this whole thing. We think this is almost certainly a move aimed at deregulation. Think about the basic incentive structure. If the government owns a piece of OpenAI, it suddenly has a direct financial interest in that company thriving, which makes it far less likely to slap on burdensome regulations that would slow the company down or hurt its value. It's a bit like a referee who's quietly been made a part-owner of one of the teams; that ref is going to be a lot less eager to throw penalty flags. And this matters right now because AI companies have been getting squeezed hard in Washington, facing export controls, national security reviews, and mandatory government review of their most powerful models before public release. By turning the regulator into a business partner, OpenAI is trying to transform an adversarial relationship into an aligned one. If that works, and regulations ease across the board, it wouldn't just help OpenAI; it would be a tailwind for the entire AI ecosystem. This leads us into 3 names (2 larger/lower-risk stocks and 1 smaller/higher-risk stock) that we think could benefit from lighter regulations:

- Marvell (MRVL) - The connectivity and custom-silicon leader benefits because looser rules speed up hyperscaler spending on the exact networking and custom chips Marvell specializes in. This is the company that Nvidia's CEO, Jensen Huang, said will be the "next trillion dollar company". This is a very well established name, and we consider it relatively safe for our long-term portfolios, while still offering us huge growth potential.

- Qualcomm (QCOM) - Fresh off its aggressive data center push, Qualcomm benefits because fewer restrictions on AI deployment and chip exports mean a bigger, faster-growing market for its new Dragonfly server chips. QCOM is only up roughtly 20-25% over the past 5 years so it's one of the few chip stocks that hasn't already skyrocketed. Similar to Marvell, we consider this a lower-risk play for our stock portfolios, with a large upside potential.

- Penguin Solutions (PENG) - A provider of AI infrastructure and data center integration, it benefits because deregulation accelerates the data center buildout that drives its core demand. Unlike Qualcomm, Penguin has soared 200% this year so far, but given it's $3 billion valuation, we still think there is plenty of room to run for long-term investors. We consider this the highest risk name for our portfolio, but also the one with the most upside potential.

To summarize everything we've talked about, OpenAI has proposed handing the U.S. government a 5% stake worth roughly $42.6 billion, framed as sharing AI's upside with the public but, in our view, primarily a strategic play to align Washington's incentives with the company's success and ease the regulatory pressure bearing down on the industry. History suggests government stakes can precede enormous stock runs, with Intel up nearly 494% since its government investment, though that surge had multiple drivers beyond just Washington's involvement. If this deal goes through and ushers in a lighter regulatory era, we think the names we listed above are positioned to benefit heavily.

And speaking of getting positioned to benefit heavily, we're doing something special for the Fourth of July holiday to benefit our newsletter subscribers. In honor of America's 250th birthday, we're granting you $200 OFF your membership to The CEO Watchlist Investment Club by [CLICKING HERE]. When you join, you get full transparency into our personal stock and options portfolios, the actual plays we're making with our own money, in real time, nothing held back. Every position we buy and sell, you'll see. We share all of our research inside The Club which has helped our students stay ahead of Wall Street. If you've been on the fence, this is the moment to step inside and see how we've been able to consistently outperform hedge funds and "Super Investors" like Warren Buffett! [CLICK HERE] to lock in your $200 OFF before the Fourth of July deal ends. With that said, we'll see you inside The Club!

"Super Investor" Spotlight: Daniel Loeb (Source)

Stocks mentioned: $AMZN, $TDS, $CRH, $SGI, $CRS, $MTZ, $DHR, $TSM, $APG, $LYV

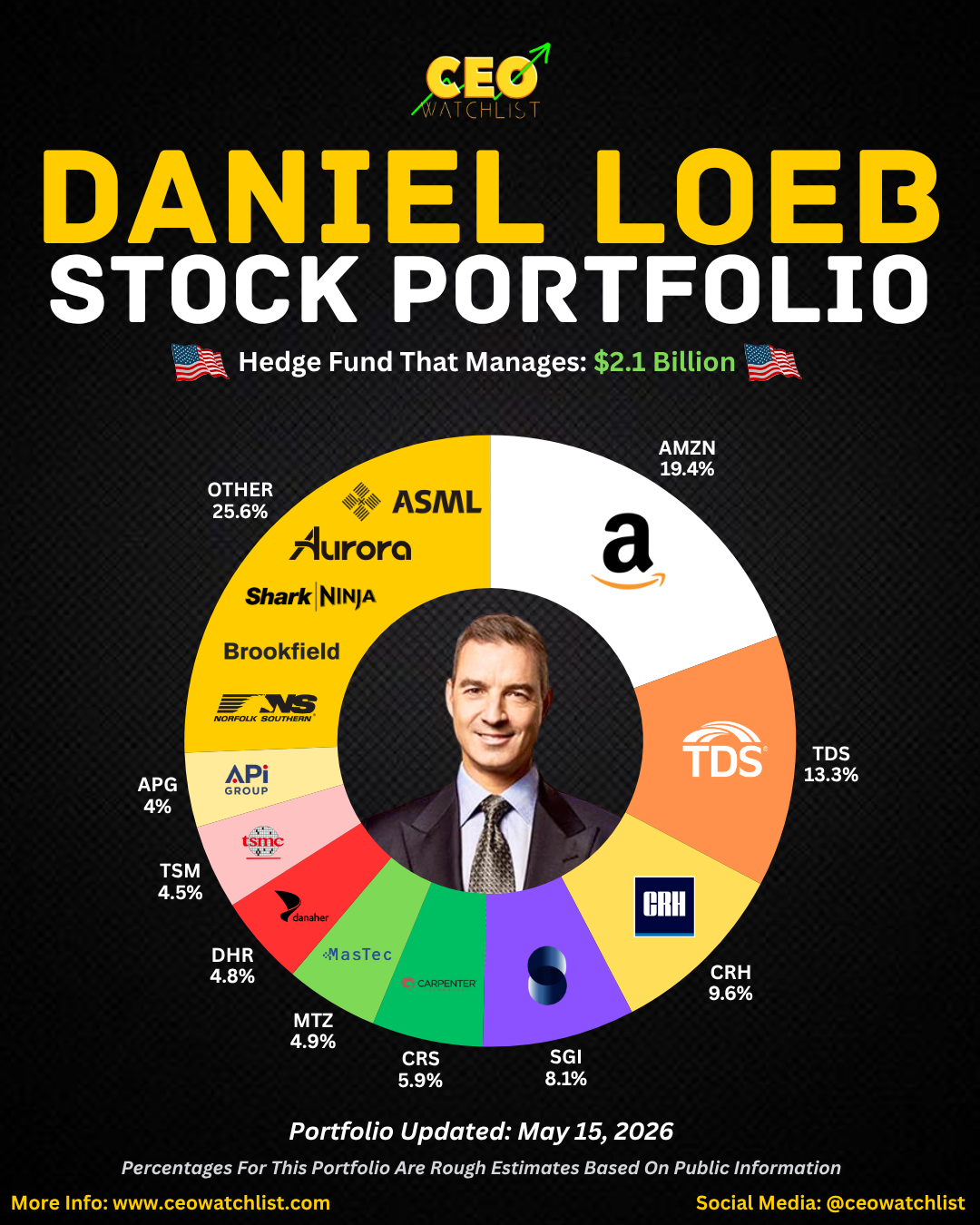

If you've spent any time in investing circles, you've probably heard people obsess over what the "smart money" is buying. That obsession has a name: "Super Investors". A "Super Investor" is a fund manager or firm with such a strong long-term track record and such deep market instincts that the rest of us literally watch their moves for clues. By law, any institution managing over $100 million has to file a 13F every quarter, which is a public document listing the U.S. stocks they own. It's basically a peek into the smart money's hand, filed up to 45 days after the quarter ends. And this week we're breaking down one of Wall Street's sharpest: Daniel Loeb.

Daniel Loeb founded Third Point in 1995, and he's built a reputation as one of the most aggressive activist investors in the game. An activist investor is someone who buys a big stake in a company and then pushes management to make changes, whether that's shaking up the board, spinning off a division, or cutting costs, all to force the stock higher. Loeb became legendary for his blunt, sometimes brutal public letters to CEOs, and Third Point has delivered strong long-term returns across multiple market cycles by mixing that activist playbook with classic event-driven and value investing. His reported public stock book manages around $2.1 billion, and as you'll see, it's a much more eclectic, value-tilted mix than the pure AI portfolios we've covered lately.

Here's the latest snapshot of Daniel Loeb's top 10 stock holdings, ranked by how much of the book each makes up:

- Amazon (AMZN) - 19.4%

- Telephone & Data Systems (TDS) - 13.3%

- CRH plc (CRH) - 9.6%

- Somnigroup International (SGI) - 8.1%

- Carpenter Technology (CRS) - 5.9%

- MasTec (MTZ) - 4.9%

- Danaher (DHR) - 4.8%

- Taiwan Semiconductor (TSM) - 4.5%

- APi Group (APG) - 4.0%

- Live Nation (LYV) - 3.4%

So what's the takeaway? Daniel Loeb is quietly telling you that not every dollar has to chase the same handful of AI mega-caps. His book pairs a giant Amazon anchor with a deep bench of industrial, infrastructure, and material names. He's betting that the boring, physical backbone of the economy is where a lot of value is hiding right now. We like this portfolio as a teaching tool because it's a refreshing reminder that thematic diversity and activist discipline still matter. In our opinion, we agree with the large weighting in Amazon and actually think it's a phenomenal buy for our stock portfolios today. We think that Amazon will outperform the S&P500, consistently, over the coming years. To recap: Daniel Loeb's Third Point runs a roughly $2.1B book led by Amazon, TDS, and CRH, with a strong tilt toward infrastructure, industrials, and materials alongside select chip and consumer exposure. When an activist this sharp builds a book this different from the crowd, it's worth understanding exactly what he sees that everyone else is missing.

INSIDER STOCK TRADES FROM THE WEEK:

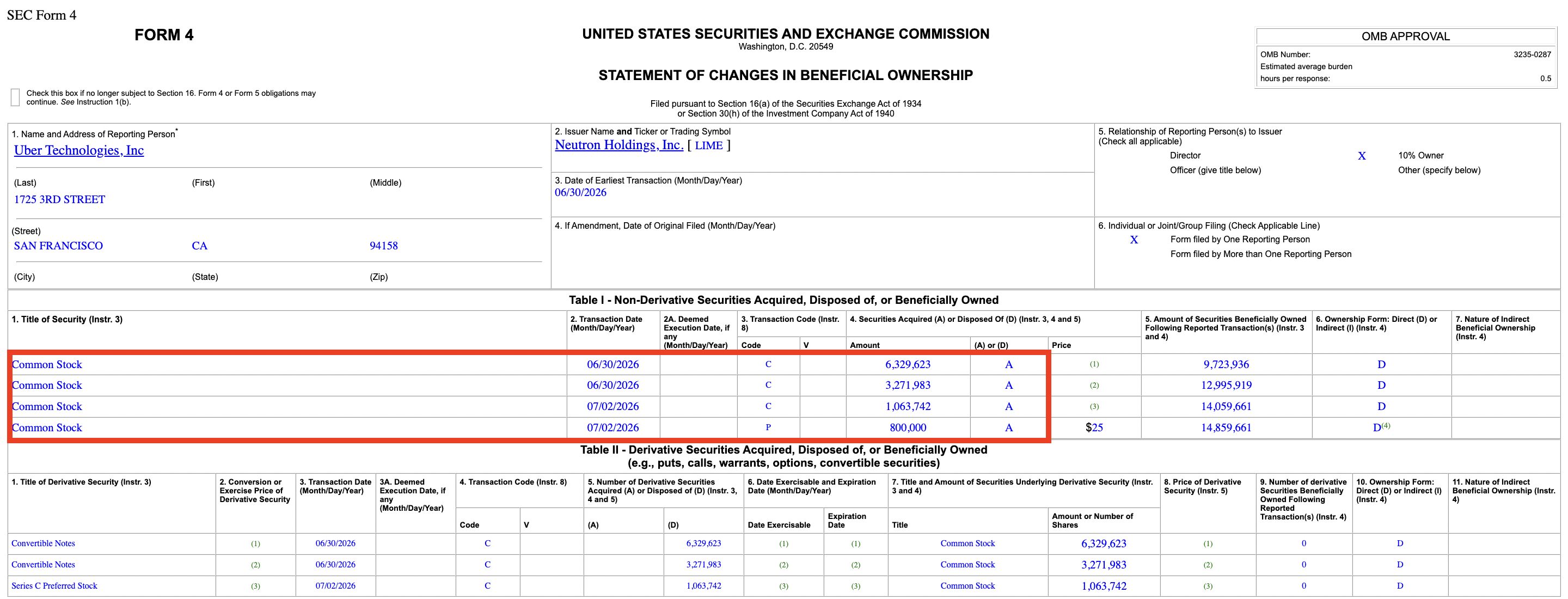

1. Neutron Holdings (LIME) - Uber (10% owner) bought roughly $20,000,000 of LIME at an average price of $25.00/share between June 30 - July 2, 2026, and it was reported to the public on July 2, 2026. (Source)

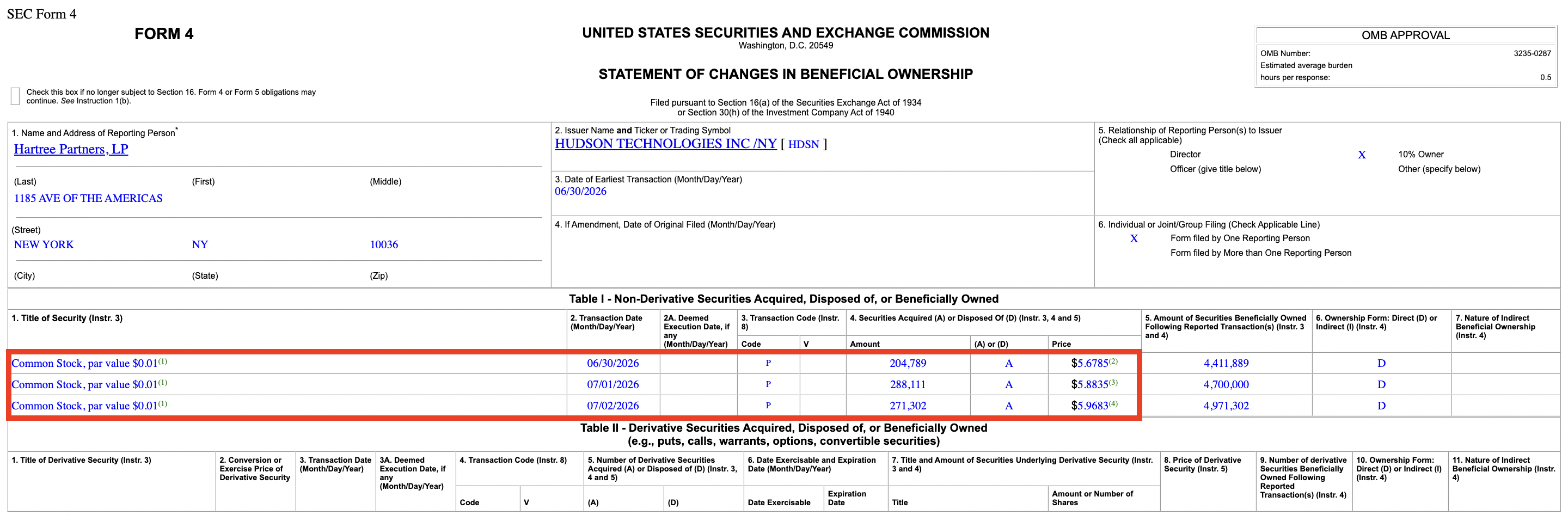

2. Hudson Technologies (HDSN) - Hartree Partners (Director) bought roughly $4,500,000 worth of HDSN at an average price of $5.86/share between June 30 - July 2, 2026, and it was reported to the public on July 2, 2026. (Source)

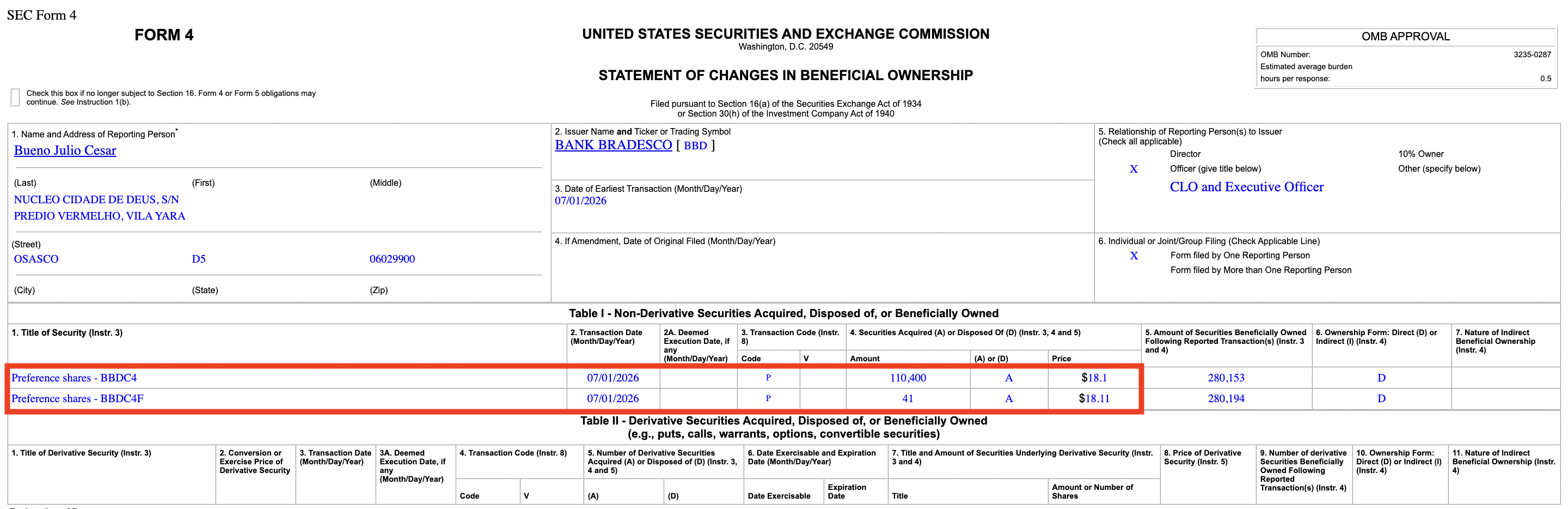

3. Bank Bradesco (BBD) - Julio Cesar Bueno (CLO & Executive Officer) bought roughly $2,000,000 of BBD at an average price of $18.10/share on July 1, 2026, but it wasn't reported to the public until July 2, 2026. (Source)

Over 2,000 people have already signed up for my FREE Masterclass video on how to unlock my exact strategies for finding winning stock/options trades! I'll share everything including how to find what Politicians and CEOs are buying. Don’t miss your chance to get in for FREE before spots fill up!

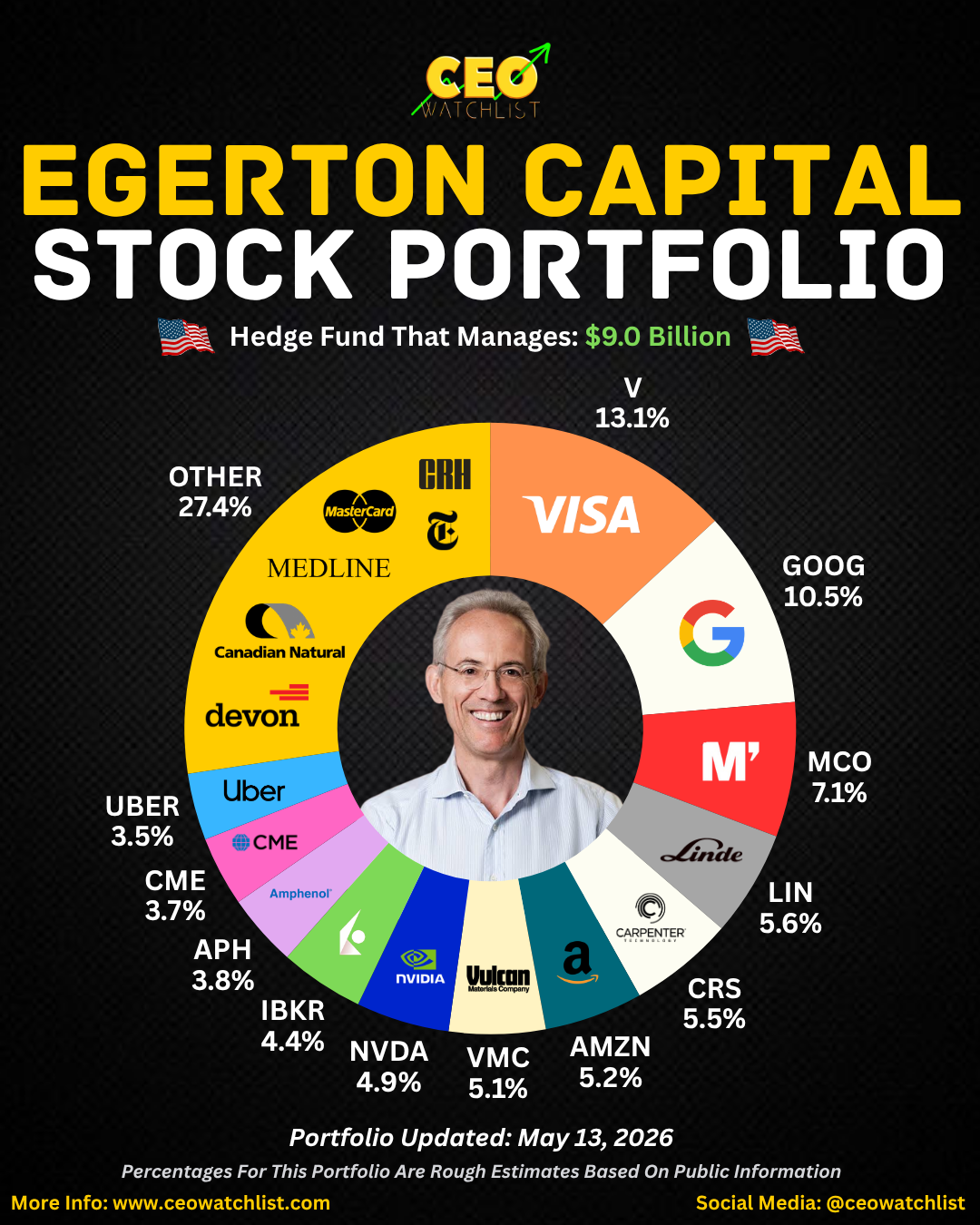

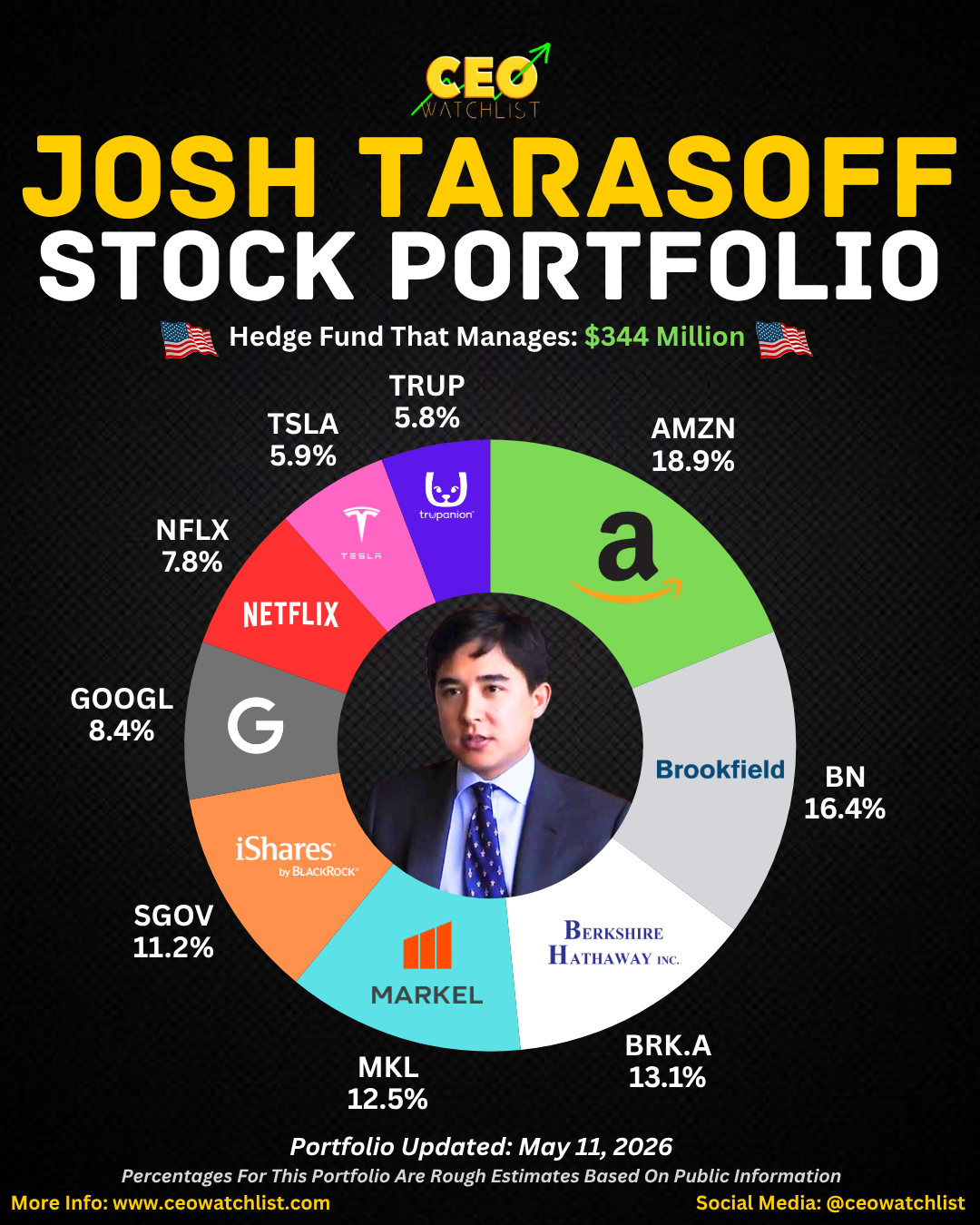

INFOGRAPHICS FOR THE WEEK:

CONTACT US: [email protected]

Responses