TOP NEWS AFFECTING THE STOCK MARKET THIS WEEK:

Earnings Season Is Here: 5 Stocks We Are Watching This Week (Source)

Stocks mentioned: $PENG, $LEVI, $DAL, $TSM, $ASML, $JPM, $GS, $NFLX

We're now officially stepping into earnings season, and it's about to come at us fast. Over the next few weeks, a firehose of companies will report how they actually performed over the past quarter, kicking off in earnest next week with a heavy lineup of major banks and a couple of big semiconductor names. For anyone newer to this, earnings season is the stretch a few times a year when public companies open their books and tell investors exactly how much money they made, whether they beat or missed Wall Street's expectations, and what they see coming down the road. It's the closest thing the market has to report-card day, and it tends to produce some of the biggest single-day stock moves of the entire year. So buckle up, because the next few weeks are going to be busy, and the action starts in a serious way next week.

We've actually already gotten a small taste of what's to come, and the early reports have been a mixed bag worth learning from. The standout was Penguin Solutions (PENG), which absolutely blew the doors off. The company delivered what's called a "double beat and raise," meaning it beat expectations on both revenue and profit AND raised its guidance for the rest of the year. Revenue jumped nearly 48% year over year on booming AI demand, and the stock rocketed roughly 18% the next day. This has been one of our favorite higher-risk, higher-reward plays in our stock portfolios over the past couple of months, so it was great to see it deliver, despite being up 200% YTD! But not every strong report got rewarded, which is the tricky part. Levi Strauss (LEVI) also posted a double beat and raise, genuinely good numbers, yet the stock dropped around 5% the following day. One last stock worth mentioning from last week was Delta (DAL), which reported Friday morning amid elevated oil prices; with fuel being one of an airline's biggest costs. But those reports are in the past, and now it's time to turn to the main event, because next week is stacked. So without further ado, let's dive into the top 5 stocks we're watching this week that will set the tone for both the AI trade, and the broader economy:

- Taiwan Semiconductor (TSM) - Reporting Thursday, July 16. TSM is the factory that physically builds the world's most advanced chips, including for NVIDIA and Apple, so its results are a direct read on how strong AI chip demand really is. We expect continued strength driven by the AI boom, and more importantly, we'll be listening closely to its outlook, since TSM's forecast is essentially a crystal ball for the entire chip sector.

- ASML (ASML) - Reporting Wednesday. ASML makes the ultra-advanced machines required to manufacture cutting-edge chips, with a near-monopoly on the technology. Analysts expect solid profit growth of around 16%, but the number everyone actually cares about is "bookings" (new orders for its machines), because that tells us how much chipmakers plan to spend building future capacity.

- JPMorgan (JPM) - Reporting Tuesday. As the largest U.S. bank, JPMorgan's report is a health check on the entire economy: how much people are borrowing, whether they're paying loans back, and how confident businesses are. We expect solid results, and CEO Jamie Dimon's commentary on the economy tends to move the whole market.

- Goldman Sachs (GS) - Reporting Tuesday. Goldman is Wall Street's dealmaking powerhouse, so its results reveal how active mergers, IPOs, and trading have been. With markets buzzing this year (think the SpaceX IPO), we expect its investment banking and trading desks to show real strength.

- Netflix (NFLX) - Reporting Thursday after the close. The stock is down roughly 19% this year on worries that subscriber growth is slowing, so this is a big test. We expect revenue growth around 13%, but the number we really care about is the advertising business, which is expected to roughly double this year to around $3 billion. If ads are scaling the way management promised, that changes the story for a stock the market has already given up on.

Here's the thing to keep in mind as all this unfolds, and it's the theme those early reports already hammered home: in earnings season, expectations matter as much as results. A company can post genuinely great numbers and still see its stock fall if investors were hoping for even more, exactly what happened to Levi. On the flip side, a beaten-down name can pop on merely "less bad" news. So as we head into next week, we're not just asking "did they beat?" We're asking "did they beat by enough to justify where the stock already is?" That's the lens we apply to every one of these reports.

Meta Is Coming For Nvidia: The 4 Must Own Stocks For Our Portfolios (Source)

Stocks mentioned: $META, $AVGO, $TSM, $GOOG, $AMZN, $MSFT, $AAPL, $NVDA, $MRVL, $AMKR

This past week, Meta (META) finally broke out, and the market is celebrating for all the obvious reasons. After spending most of 2026 in the penalty box, punished by investors terrified of its plan to spend up to $145 billion on AI infrastructure this year with no visible payoff, the company finally started showing proof that all that money could turn into actual revenue. First came the leaked report that Meta plans to sell its excess computing power to outside customers. Then on Thursday came "Muse Spark 1.1", an aggressively priced AI coding model built to go head-to-head with OpenAI and Anthropic. Once the market caught wind of this news, the stock ripped. But while everyone was staring at the shiny new AI products, Meta quietly confirmed something far more consequential, and almost nobody is talking about it. Buried underneath the headlines was the company moving forward with the third generation of its own custom-designed chip. That announcement, not Muse Spark, is the one that should have your attention.

Meta has been building a proprietary chip line called "MTIA" (short for Meta Training and Inference Accelerator) and it just advanced to "MTIA v3", designed in partnership with Broadcom (AVGO) and manufactured on Taiwan Semiconductor's (TSM) 3nm process, with plans to launch a new generation every six months through 2028. Now, why would Meta go through the enormous trouble of designing its own chips when it could just buy them off the shelf? One number answers that question. Meta estimates that running its own custom chips in its data centers delivers a 40% to 44% reduction in total cost of ownership. Read that again, because it's staggering. Nearly half the cost, simply by designing the silicon yourself instead of renting someone else's. When you're spending $145 billion a year on infrastructure, cutting your compute costs by 40% isn't a nice-to-have, it's a rewrite of your entire economic model. And here's the crucial part: Meta isn't some lone pioneer here. Google (GOOG) has been running its own TPU chips since 2014. Amazon (AMZN) has its Trainium line. Microsoft (MSFT) is building Maia. Apple (AAPL) designs its own silicon across every product it ships. Every single hyperscaler on the planet is doing the same thing at the same time, which tells you this isn't a one-company experiment. It's an industry-wide migration.

So let's break down what's actually happening in plain terms, and how we plan to profit from it. For years, everyone building AI leaned on Nvidia's (NVDA) GPUs, which are extraordinarily powerful but also expensive and chronically supply-constrained. A GPU is a general-purpose tool: it can handle almost any AI task reasonably well, which is exactly what you want when you don't yet know what you'll need. Custom chip on the other hands (called an "ASIC"), is the opposite: it's engineered to do one specific job exceptionally well. Think of it like the difference between a Swiss Army knife and a chef's knife. The Swiss Army knife is what you grab when the task is unknown and versatility matters. But if you're chopping vegetables all day, every single day, the purpose-built chef's knife is faster, cheaper, and simply better at the one thing you actually do. The hyperscalers have now been running AI workloads long enough to know exactly what they're chopping. So they're commissioning custom knives instead of paying a premium for versatility they no longer need. Cost control, performance optimization, and less dependence on a single supplier. That's the whole thesis in one sentence.

This is why we're focused on the companies sitting at the intersection of the custom chip buildout, because here's the beautiful part of this trade: it doesn't matter who wins. Whether Meta's MTIA outperforms Google's TPU or Amazon's Trainium is irrelevant to these names, because they get paid regardless of which hyperscaler comes out on top. They're selling shovels to every miner in the gold rush. So with that being said, let's dive into some of our top stocks that are sitting at the intersection of custom chips:

- Broadcom (AVGO) - The single biggest beneficiary in custom silicon. It co-designs Meta's MTIA chips, Google's TPUs, and OpenAI's chips, meaning it touches most of the major custom programs in existence. It is effectively the arms dealer of this entire war.

- Marvell (MRVL) - The other major custom-silicon design house, anchoring Amazon's Trainium program, and it also supplies the high-speed connectivity chips required to wire these massive clusters together.

- Taiwan Semiconductor (TSM) - The factory where nearly all of these custom chips physically get manufactured, including Meta's MTIA v3 on its 3nm process. Whoever designs the chip, TSM builds it.

- Amkor Technology (AMKR) - A leader in advanced chip packaging, the critical step of assembling and connecting chips into functioning units. Custom AI chips demand increasingly complex packaging, making Amkor a quiet but essential beneficiary.

Now let's be fair, because the bear case here is legitimate and worth respecting. Nvidia is not going away, and anyone reading this as "the GPU is dead" is misreading it badly. Even as Meta ramps MTIA, it's still earmarking roughly 6 gigawatts of AMD GPU capacity and millions of Nvidia chips alongside it, which tells you these companies are pursuing a multi-vendor strategy, not a wholesale replacement. Custom chips are also inherently less flexible. When AI models evolve in unexpected directions, a general-purpose GPU can pivot while a purpose-built ASIC may find itself optimized for yesterday's problem. And these custom programs have a real history of delays; Meta's own MTIA effort has slipped from its original targets more than once over its five-year life. Those are honest risks. But here's our counterpoint, and it's a simple one: a 40%-plus cost reduction is not a marginal improvement. It's a structural one. And in this industry, structural cost advantages tend to compound and win over time, even when the road there is bumpy.

Overall, Meta's breakout is being credited to Muse Spark and compute selling, and those are genuinely good news for the stock. But the announcement that will still matter in three years is the one that got almost no coverage: Meta advancing its third-generation custom chip, cutting its compute costs by more than 40%, and joining Google, Amazon, Microsoft, and Apple in a coordinated march away from renting general-purpose GPUs toward owning purpose-built silicon. That migration is a tectonic shift in how AI infrastructure gets built, and it flows straight through to the designers, foundries, and packagers who make it possible. NVIDIA will remain enormously important, and the transition will be messy and uneven. But the direction of travel is unmistakable, and it's why AVGO, MRVL, TSM, and AMKR are the names we're watching most closely. Everyone's looking at the products Meta is selling. We're looking at what Meta is building underneath them.

"Super Investor" Spotlight: Stephen Mandel (Source)

Stocks mentioned: $VST, $ASML, $CRS, $LPLA, $APP, $TLN, $TER, $CVNA, $NU, $MDLN

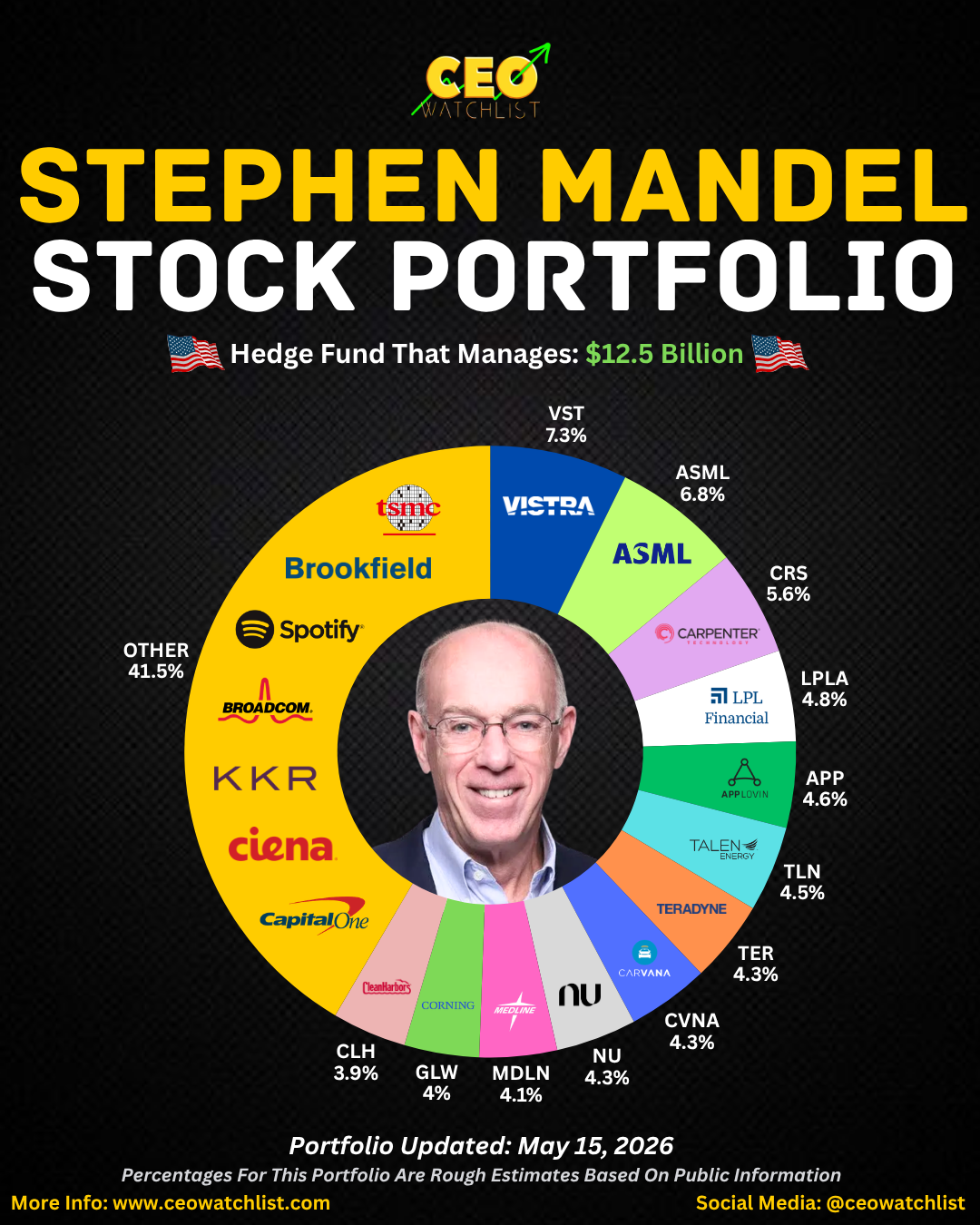

If you've spent any time in investing circles, you've probably heard people obsess over what the "smart money" is buying. That obsession has a name: "Super Investors". A "Super Investor" is a fund manager or firm with such a strong long-term track record and such deep market instincts that the rest of us literally watch their moves for clues. By law, any institution managing over $100 million has to file a 13F every quarter, which is a public document listing the U.S. stocks they own. It's basically a peek into the smart money's hand, filed up to 45 days after the quarter ends. And this week we're breaking down one of the most respected stock-pickers of his generation: Stephen Mandel.

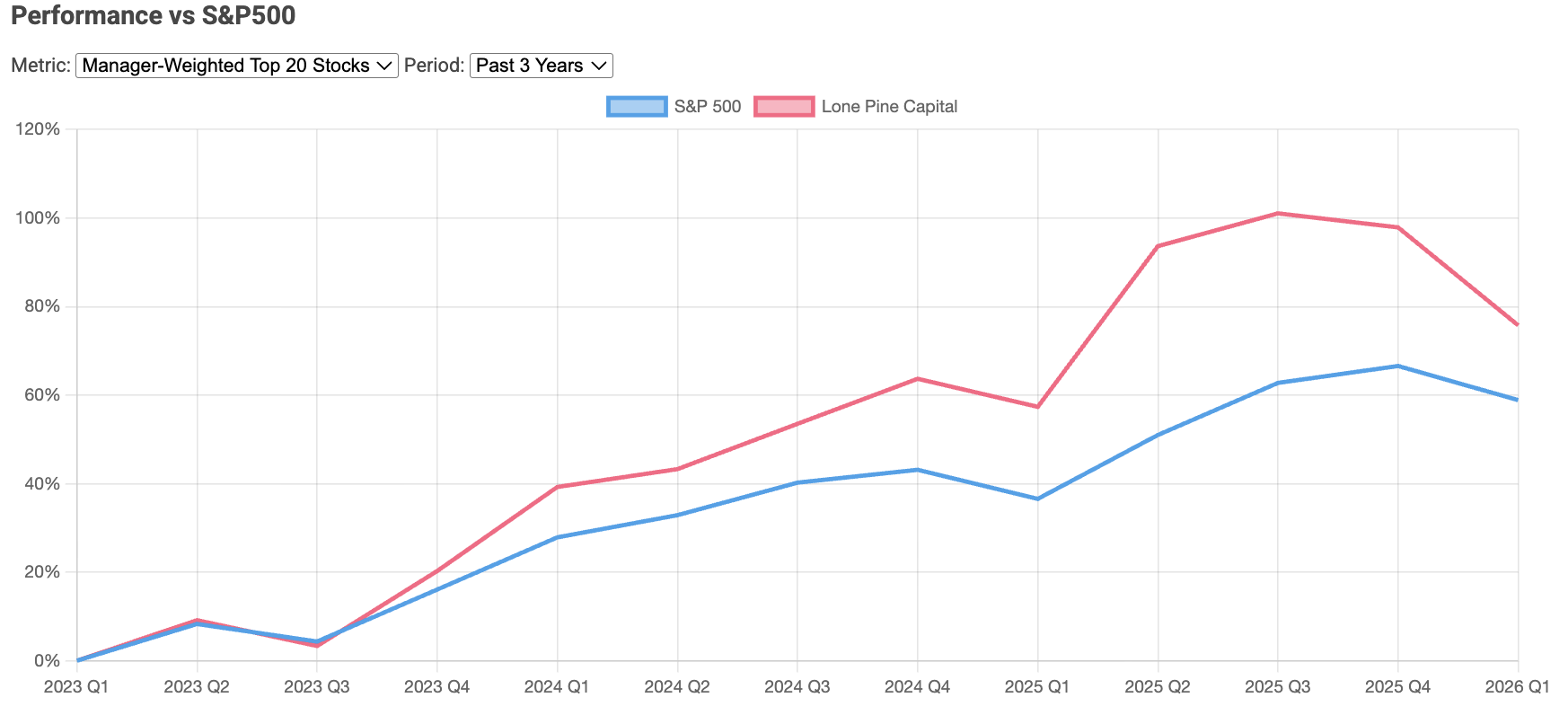

Stephen Mandel founded Lone Pine Capital in 1997. Mandel built Lone Pine into one of the most respected long/short equity shops in the world, meaning the fund bets on stocks it thinks will rise (longs) while also betting against ones it thinks will fall (shorts). He's known for deep, fundamental research and a patient focus on high-quality growth companies rather than quick trades. As you can see in the image below, his track record backs up the reputation, as over the past 3 years, Lone Pine's top holdings returned roughly 76%, versus about 59% for the S&P 500 over the same stretch:

So with that being said, let's take a look at the top 10 stocks that Stephen Mandel's has in his portfolio:

- Vistra (VST) - 7.3%

- ASML (ASML) - 6.8%

- Carpenter Technology (CRS) - 5.6%

- LPL Financial (LPLA) - 4.8%

- AppLovin (APP) - 4.6%

- Talen Energy (TLN) - 4.5%

- Teradyne (TER) - 4.3%

- Carvana (CVNA) - 4.3%

- Nu Holdings (NU) - 4.3%

- Medline (MDLN) - 4.1%

So what's the takeaway? Stephen Mandel is making a smart, multi-layered bet on the AI era, but he's expressing it through the stuff most people overlook: the electricity that powers the data centers and the equipment that builds and tests the chips, rather than just piling into the obvious mega-caps. The lesson for the rest of us isn't "go copy this list," it's watching how a world-class stock-picker finds the non-obvious beneficiaries of a giant trend, then balances them with high-quality growth names for extra upside.

INSIDER STOCK TRADES FROM THE WEEK:

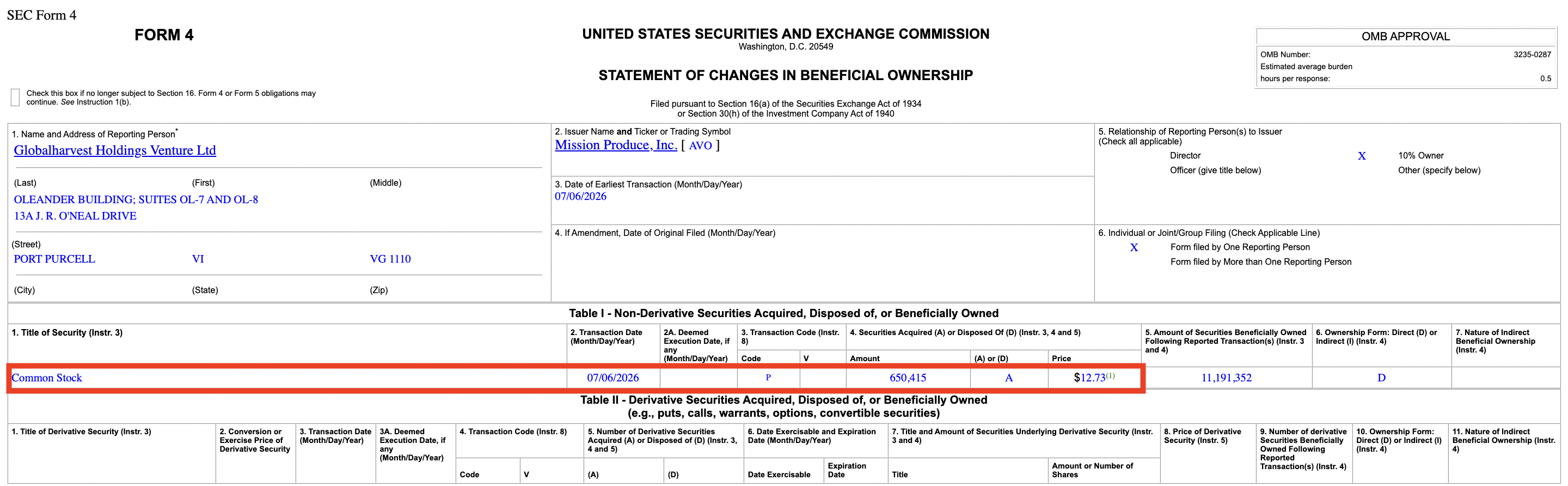

1. Mission Produce (AVO) - Globalharvest Holdings (10% owner) bought roughly $8,300,000 of AVO at an average price of $12.73/share on July 6, 2026, but it wasn't reported to the public until July 8, 2026. (Source)

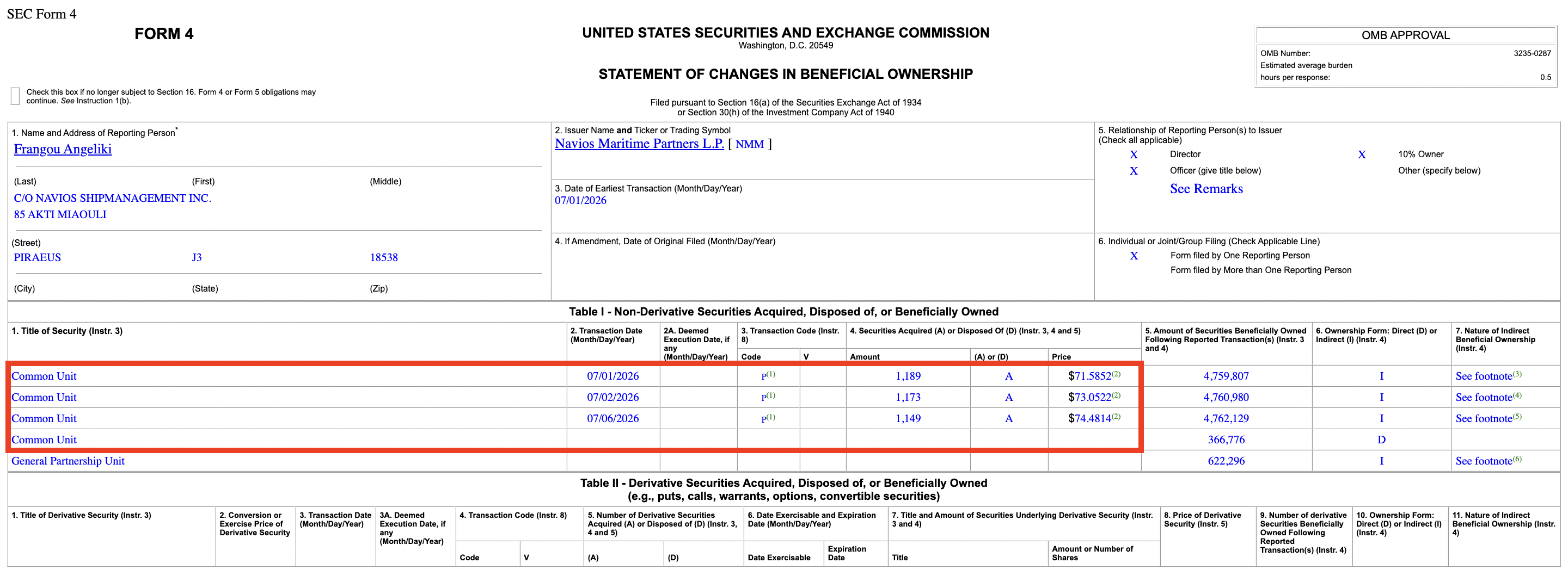

2. Navios Maritime Partners (NMM) - Angeliki Frangou (CEO) bought roughly $250,000 worth of NMM at an average price of $73.02/share between July 1 - July 6, 2026, and it was most recently reported to the public on July 6, 2026. (Source)

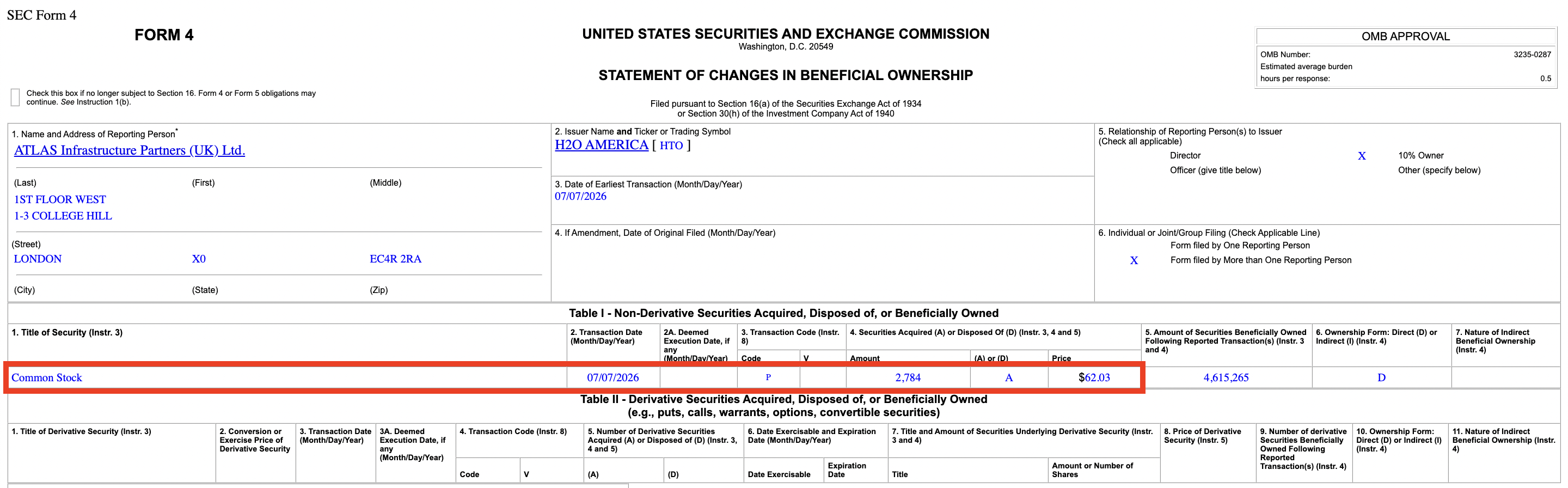

3. H2O America (HTO) - ATLAS Infrastrucutre Partners (10% owner) bought roughly $175,000 of HTO at an average price of $62.03/share on July 7, 2026, but it wasn't reported to the public until July 8, 2026. (Source)

Over 2,000 people have already signed up for my FREE Masterclass video on how to unlock my exact strategies for finding winning stock/options trades! I'll share everything including how to find what Politicians and CEOs are buying. Don’t miss your chance to get in for FREE before spots fill up!

INFOGRAPHICS FOR THE WEEK:

CONTACT US: [email protected]

Responses