TOP NEWS AFFECTING THE STOCK MARKET THIS WEEK:

Nvidia Claims This Is The Next Trillion Dollar Stock... (Source)

Stocks mentioned: $MRVL, $NVDA, $POOL, $CPB

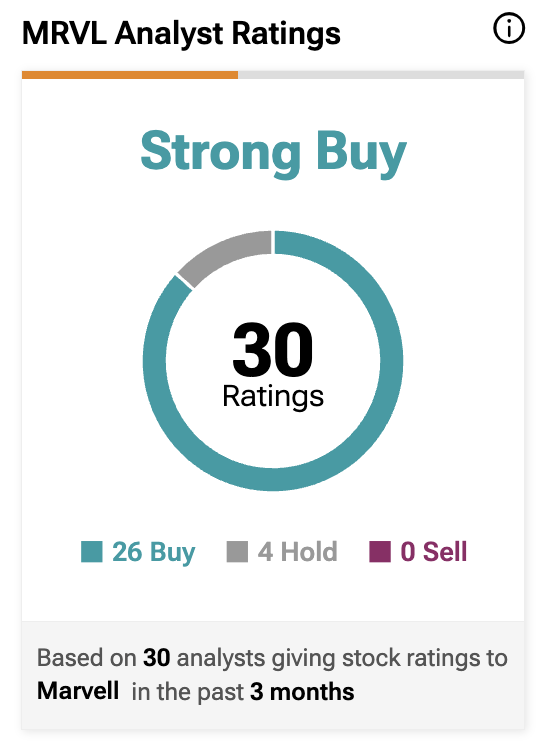

On June 2, at the COMPUTEX 2026 conference in Taipei, the most powerful man in the chip world stood on stage next to Marvell CEO Matt Murphy and said eight words that sent a $250 billion company into orbit. "Ladies and gentlemen, the next trillion-dollar company," Jensen Huang said, in reference to Marvell (MRVL). For context, Jensen is the CEO of Nvidia (NVDA), the company that essentially powers the entire AI revolution and became the first business ever to cross a $4 trillion valuation. When he points at another company and tells the world it's next in line, the market listens. And listen it did. Marvell's stock soared 32.52% on Tuesday, its biggest one-day gain ever. So why did Jensen say it? In his words: when you take a computing problem and break it into many parts and spread it across an entire data center, what becomes necessary is connectivity, and that, he said, is the reason Marvell is so essential. We agree with him, and we want to walk you through exactly why.

So what does Marvell actually do? Here's the simplest way to think about it. If NVIDIA's chips are the brains of an AI data center, Marvell builds the nervous system that connects all those brains together. The company designs networking and connectivity chips that are essential to data centers, where computing tasks get spread across thousands of connected chips that all need to share data quickly. Modern AI doesn't run on one giant computer; it runs on tens of thousands of chips working in unison, and those chips are useless if they can't talk to each other fast enough. That's the problem Marvell solves. On top of that, Marvell has positioned itself as a key supplier in custom silicon, helping cloud companies design specialized chips tailored to their specific AI workloads as they look for alternatives to standard off-the-shelf processors. Think of it like a tailor versus buying a suit off the rack. The big cloud players (Amazon, Microsoft, and others) increasingly want chips built precisely to their needs, and Marvell is one of the few shops in the world that can stitch those custom suits.

Now the bull case, and it's a strong one. The growth numbers are real, not just hype. In its first-quarter fiscal 2027 earnings, Marvell posted record revenue of $2.42 billion, up 28% year over year, beating Wall Street estimates. Looking forward, the company projects its custom chip business alone could generate more than $10 billion in annual revenue by fiscal 2029. The partnerships are blue-chip too. Marvell is backed by a strategic $2 billion investment from NVIDIA, and on March 31 the two companies formed a partnership through NVIDIA's NVLink Fusion, a rack-scale platform for semi-custom AI infrastructure. The validation goes beyond Jensen, too. Bank of America named Marvell one of two top "AI compute" stocks to buy, and the consensus across 36 covering analysts is a "Strong Buy" rating. What gets us most excited is the sectors Marvell sits in. The company plays directly in custom AI silicon and high-speed data center connectivity, including the move toward optics and photonics (using light instead of electricity to move data faster between chips), which is arguably the most important bottleneck the entire AI buildout has to solve.

Then came Friday's news, which adds a whole second engine to this story. The S&P 500 announced that Marvell will be added to the S&P 500 index, effective before the open of trading on June 22, 2026, as part of the quarterly rebalance, replacing Pool Corp (POOL) and Campbell Soup (CPB). Why does this matter so much? Because of something called forced buying. When a stock enters the S&P 500, every passive fund that tracks the index must buy shares to match the new composition, and this forced demand typically pushes the price higher in the days and weeks around the announcement and effective date. In plain terms, trillions of dollars in index funds are now legally obligated to go out and buy Marvell stock whether they want to or not. The market reacted immediately, with shares jumping 6% after-hours on Friday following the announcement. Now, in fairness, we'd be doing you a disservice if we didn't mention the other side. The stock has run extraordinarily hard, up roughly 195% year to date and 286% over the past year, and some analysts argue the valuation has gotten stretched, with the price already reflecting much of that future growth. Those are fair concerns, and momentum like this can cut both ways. But when the CEO of the most important AI company in the entire world says your stock price can quadruple, and that you're the next trillion dollar opportunity in this market, then traditional valuation metrics don't really matter too much.

Here's the bottom line. The most respected voice in the entire AI hardware world stood on a stage and personally anointed Marvell as the next trillion-dollar company, and he put Nvidia's money behind that conviction with a $2 billion investment and a deep technical partnership. The fundamentals back the story up: record revenue, 28% growth, a $10 billion custom-silicon runway, and a dominant position in the exact bottlenecks (connectivity, custom chips, and photonics) that the AI buildout absolutely has to solve. And now Marvell is being swept into the S&P 500, unleashing a wave of forced institutional buying right on top of all that momentum. Could the stock cool off after a run this hot? Absolutely, and anyone buying here should size their position with that in mind. But the long-term thesis is intact and, in our view, getting stronger. Jensen Huang sees what we see. Marvell isn't just along for the AI ride. It's one of the few companies building the road itself. When the man whose chips define this entire era tells you who's next, and the fundamentals, the partnerships, and now the index inclusion all line up behind him, you pay attention. We're on the same page as Jensen on this one.

Is It Time To Sell Big Tech? Let's Cover That, and Also What Stocks We're Eyeing To Buy... (Source)

Stocks mentioned: $GOOG, $BRK.B, $MU, $AAOI, $ASML, $NBIS, $TSM

On June 1, 2026, Alphabet (GOOG) (Google's parent company) did something it almost never does. It announced an $80 billion equity raise, its first large-scale stock offering since 2010, with the capital earmarked to fund investments in its AI compute infrastructure to meet what it called "unprecedented customer demand," including a $10 billion investment from Warren Buffett's Berkshire Hathaway (BRK.B). A day later they upsized it. The final deal priced at $84.75 billion, bumped up from the original $80 billion. To put that in perspective, no company in history has ever raised that much capital in a single deal, and Google hadn't sold equity to raise cash since 2006. So why would one of the most cash-rich companies on earth, sitting on over $100 billion in cash and generating $174 billion in operating cash flow over the prior twelve months, suddenly go raise outside money? Because the AI buildout has gotten so expensive that even Google's enormous internal cash flow isn't enough to keep pace. The company guided to capital expenditures of $180 billion to $190 billion in 2026, and said 2027 would significantly increase from there. That's the setup. Now let's talk about what it actually means for your portfolio.

Here's the part that confuses a lot of newer investors. You'd think a company spending massively to dominate the future would be a good thing for the stock, but the market often reads it the opposite way, at least in the short term. Two things spook the market here. First is the CapEx itself. CapEx (capital expenditure) is the money a company spends building physical things like data centers, servers, and chips. The more a company plows into CapEx, the less is left over to return to shareholders through buybacks and dividends, and the longer investors have to wait to see a payoff. Second, and bigger here, is dilution. When a company issues $85 billion in new stock, it's carving the same pie into more slices, so each existing share now represents a slightly smaller ownership stake in the business. Markets generally don't love either one, and that's the core reason a raise this size, even for a great reason, can be read as a near-term headwind for the stock. To be fair, plenty of smart investors see it the other way. Some analysts view the raise as an extremely bullish signal, arguing it reflects management's confidence in capturing outsized returns from insatiable AI demand, and Berkshire anchoring the deal lends real credibility. That's a legitimate counterpoint. But our read of the immediate market reaction is that spending at this scale gets treated with caution first and rewarded later.

This is where it gets bigger than just Google, because Google almost certainly won't be the last to do this. Google, Microsoft, Meta, and Amazon are collectively expected to pour roughly $1 trillion into capex this year, with total AI capex climbing even higher next year. When the biggest player in the space sets a precedent for tapping outside capital to fund the AI race, the others tend to follow, because nobody wants to be the one who blinked and fell behind on compute. We're already seeing it. Amazon raised nearly $54 billion in bond markets, Alphabet priced about $32 billion in dollar and euro notes in February, and Oracle raised $25 billion from a bond sale. And the freshest signal that was just announced on Friday by the Financial Times was that Meta is weighing a big equity raise to finance its AI infrastructure. If Meta does confirm an equity raise, we'd expect the stock to react poorly, and there's a specific reason for that. The market has a kind of PTSD with Meta and big spending. Back in 2022, when Meta poured billions into its metaverse bet with no clear payoff, the stock got absolutely crushed, falling roughly 70-80% from its highs before it recovered. Investors remember that pain. The bottom line for big tech right now: the market isn't rewarding the companies doing the spending. It's rewarding the companies receiving that spending. That's the crucial distinction, and it points directly at where the opportunity is.

So who's on the receiving end of this tidal wave of cash? When Google, Meta, Amazon, and Microsoft spend hundreds of billions building data centers, that money flows straight down the chip supply chain into the companies that make the physical guts of AI infrastructure. These are the "picks and shovels" of the AI gold rush, and they're the names we want to be watching:

- Micron Technology (MU) - A leading maker of memory chips. AI systems need enormous amounts of high-speed memory to function, and every new data center is a buyer. More CapEx means more memory demand flowing directly to Micron.

- Applied Optoelectronics (AAOI) - A photonics player. Photonics means moving data using light instead of electricity, which is faster and more efficient over the massive distances inside modern data centers. As clusters scale, this becomes a critical bottleneck to solve.

- ASML Holding (ASML) - The Dutch company with a near-monopoly on the advanced lithography machines required to manufacture cutting-edge chips. You literally cannot make the most advanced AI chips without ASML's equipment, which makes it one of the most strategically important companies on the planet.

- Nebius (NBIS) - A purpose-built AI cloud infrastructure company and one of the premier neocloud plays in the market. When hyperscalers spend hundreds of billions on AI compute, companies like Nebius that provide GPU-dense cloud capacity to enterprises and AI developers are direct beneficiaries of that demand overflow.

- Taiwan Semiconductor (TSM) - The world's largest contract chipmaker, the factory that physically produces chips for NVIDIA, Apple, and most of the industry. When AI chip demand surges, it nearly all runs through TSMC's fabs.

These are just a handful of examples; the list of beneficiaries is long. Our framework is simple: as long as the big tech CapEx spending continues, it keeps fueling this rally, and the names we want exposure to are the ones receiving that money, right up until the spending stops. That said, we have to be honest about a warning sign. This past Friday, the price action was bizarre. Despite all these spending announcements that should be bullish for the supply chain, virtually everything traded in the red. Even Marvell, fresh off a Jensen Huang endorsement and S&P 500 inclusion, fell 17% during regular trading hours on Friday. When good news gets sold across the board, that's a signal worth respecting. It tells us the broader market may be more fragile than the individual stories suggest, and it lines up with historical seasonality, where mid-term election years (like 2026) have tended to produce pullbacks before finding a bottom later in the year. So we're staying cautious here. We're not chasing. These are names on our shopping list that we want to watch and accumulate once we get clarity and the market finds its footing, not names we're piling into blindly while the tape looks shaky.

So to summarize everything, Google just executed the largest capital raise in history, $84.75 billion, to fund its AI infrastructure, and the market tends to treat that kind of spending and dilution as a near-term negative for the company doing it. We expect the other hyperscalers (Microsoft, Amazon, and especially Meta, which is already rumored to be weighing an equity raise) to follow Google's lead, which makes us cautious on owning the big tech names while their CapEx keeps climbing, particularly given the market's lingering trauma from Meta's metaverse overspend. The flip side is that all of this spending has to land somewhere, and it lands in the chip supply chain: memory (MU), photonics (AAOI), equipment makers (ASML), neoclouds (NBIS), and the foundries (TSM). The market should be rewarding the receivers of the spend, not the spenders. But Friday's broad red day, where even great news got sold, combined with mid-term election year seasonality, has us holding our cautious stance until we get clearer signs. These supply chain names are on our watchlist for when the market bottoms, and we'd rather be patient and buy with conviction than chase into uncertainty. The opportunity is real. The timing is everything.

"Super Investor" Spotlight: Nvidia Corp (Source)

Stocks mentioned: $NVDA, $INTC, $CRWV, $SNPS, $COHR, $NOK, $NBIS

If you've spent any time in investing circles, you've probably heard people obsess over what the "smart money" is buying. That obsession has a name: "Super Investors". A "Super Investor" is a fund manager, firm, or institution with such a strong long-term track record and such deep access to information that the rest of the market literally watches their moves for clues. By law, any institution managing over $100 million has to file a 13F every quarter, which is a public document listing the U.S. stocks they own. It's basically a peek into the smart money's hand, filed up to 45 days after the quarter ends. And today we're looking at one of the most fascinating filers out there: Nvidia (NVDA) itself.

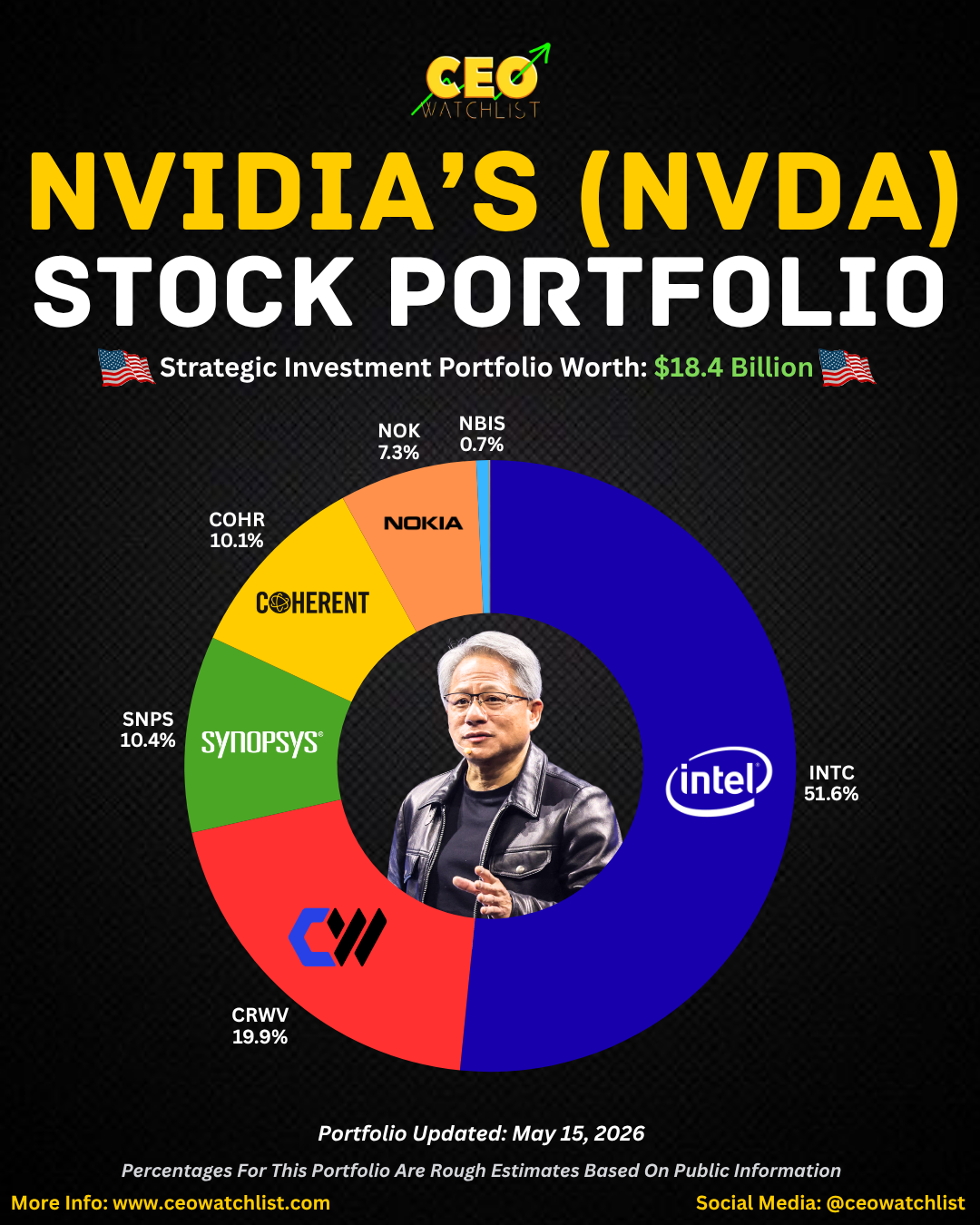

Now, Nvidia isn't a hedge fund. It's the company powering the entire AI revolution, the one selling the GPUs (the specialized chips that train AI models) that every tech giant is fighting to get their hands on. But that's exactly what makes its 13F so valuable. When the company sitting at the center of the AI buildout decides to take equity stakes in other businesses, it's effectively telling you where it thinks the bottlenecks, the demand, and the next decade of growth are hiding. Nvidia's reported stock portfolio sits around $18 billion in assets under management and it's incredibly concentrated. That concentration is the whole point. This isn't a fund spreading bets across 200 names. It's a strategic war chest.

Here's the latest snapshot from Nvidia's Q1 2026 13F, ranked by how much of the portfolio each position makes up:

- Intel (INTC) - 51.6%

- CoreWeave (CRWV) - 19.9%

- Synopsys (SNPS) - 10.4%

- Coherent (COHR) - 10.1%

- Nokia (NOK) - 7.3%

- Nebius (NBIS) - 0.7%

Let's talk about what actually moved, because the story is in the changes. Nvidia bought a new stock this quarter called Coherent (COHR). Coherent matters a lot: it makes optical transceivers and other optical networking components, the gear that shuffles data between AI chips at light speed. As data center demand for optical networking has taken off, so have Coherent shares, which are up around 350% over the last 12 months. Nvidia's stake reportedly comes as it looks to help the company increase its production capacity. Translation: Nvidia is putting money into the plumbing of AI, not just the brains. Then there's the monster add, CoreWeave (CRWV), a "neo-cloud" (a newer breed of cloud company that rents out GPU computing power specifically for AI). Nvidia increased its shares held in CoreWeave by 95%, from 24.28 million to 47.21 million, making it the second-largest holding. On the macro side, the AI infrastructure theme is clearly still the engine here, even with the broader AUM drop. One honest caveat worth flagging: these stakes are partly strategic, not purely "this stock will go up" calls. Nvidia benefits when its customers and partners thrive, so some of this is ecosystem-building. The bears would also point out that a 51.6% Intel position is enormous and tied to a turnaround story that's far from guaranteed. Fair points, and you shouldn't blindly copy any 13F.

So what's the lesson for the rest of us? Nvidia is quietly telling you the AI trade is broadening out beyond just GPUs. The money is flowing into optical networking, neo-clouds, chip design software (that's Synopsys), and even legacy giants like Intel and Nokia that sit on the supply side. That's the real signal: the picks and shovels of AI now stretch across the entire stack. We like Nvidia not just as a stock but as a compass, because few companies have a clearer view of where AI demand is heading, and this filing shows them backing optical, cloud compute, and design tooling with real capital. To recap: Nvidia runs a tight, $18B concentrated portfolio led by Intel and CoreWeave, made a new fresh bet on Coherent, nearly doubled its CoreWeave stake, and is signaling that the AI buildout is widening into networking, neo-clouds, and beyond. When the company powering the revolution puts its own balance sheet to work, it's worth paying very close attention.

INSIDER STOCK TRADES FROM THE WEEK:

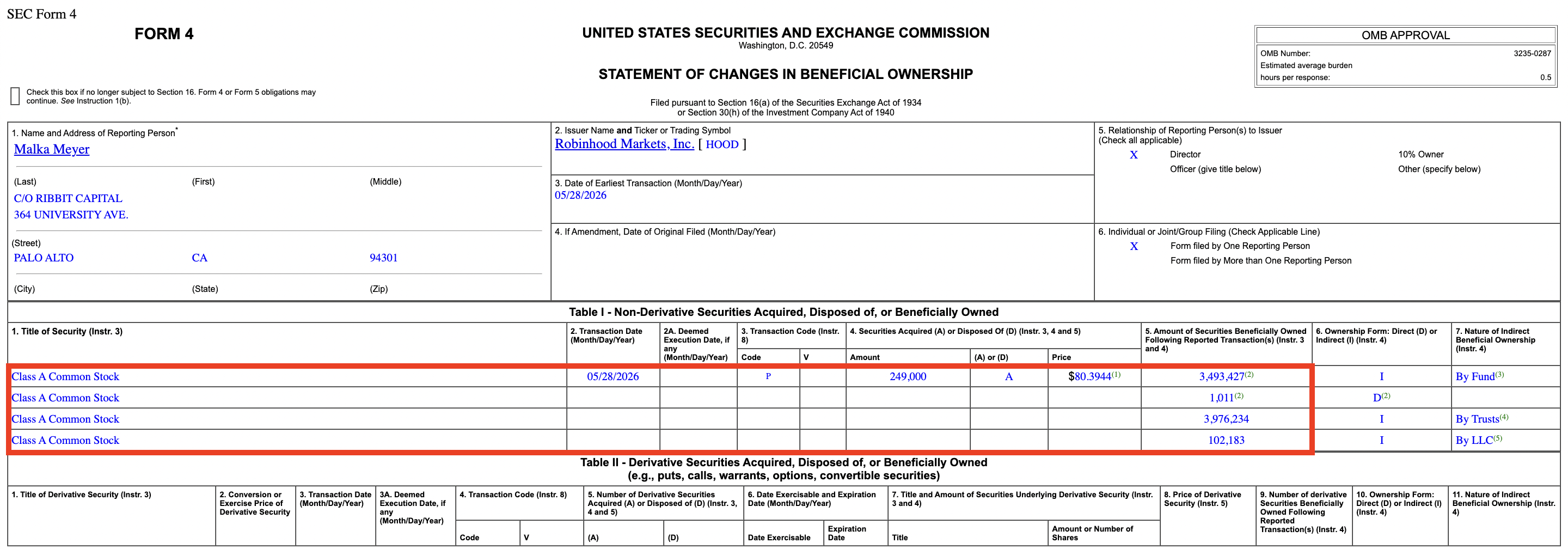

1. Robinhood (HOOD) - Micky Malka (Director and one of the original Venture Capitalists to fund Robinhood) bought roughly $35,000,000 of HOOD at an average price of $80.45/share between May 28 - June 3, 2026, and it was most recently reported to the public on June 3, 2026. (Source)

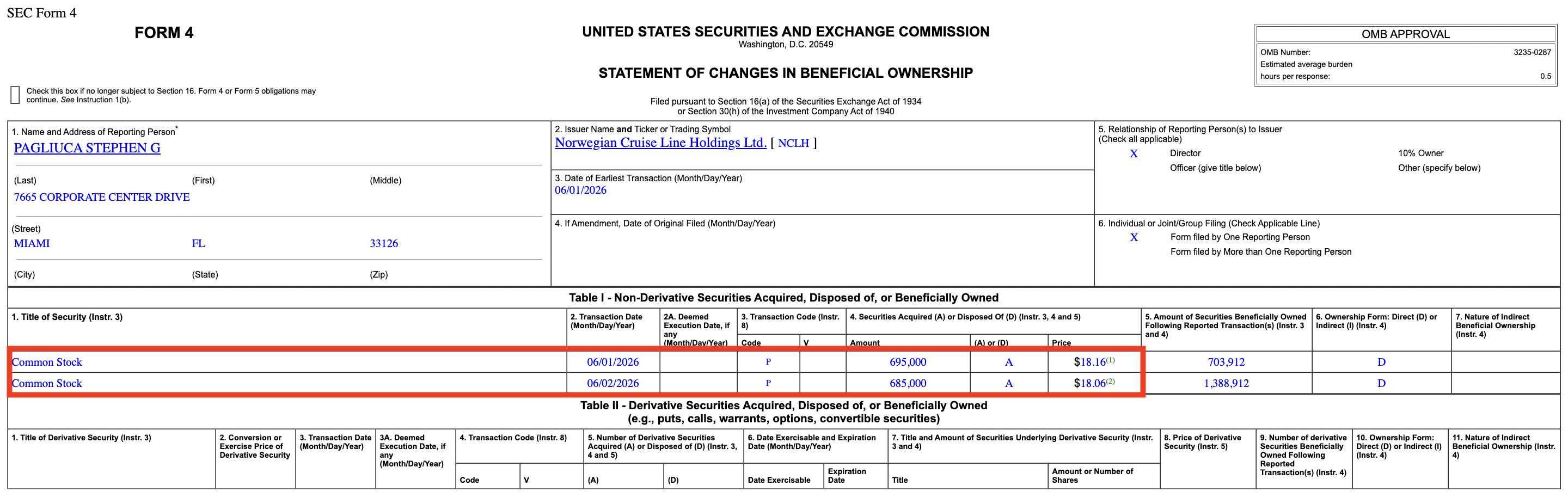

2. Norwegian Cruise Line Holdings (NCLH) - Stephen Pagliuca (Director, Billionaire, and Co-Owner of the Boston Celtics) bought roughly $25,000,000 worth of NCLH at an average price of $18.11/share between June 1-2, 2026, but it wasn't reported to the public until June 3, 2026. (Source)

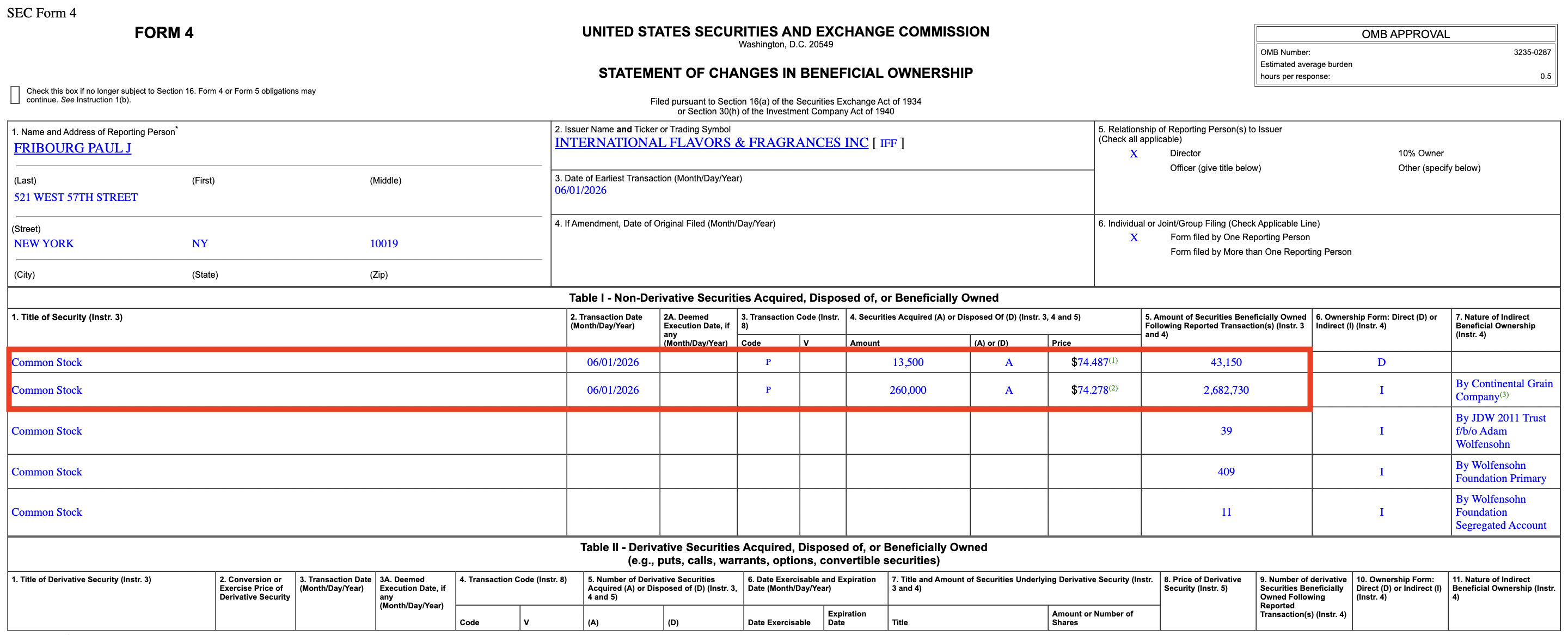

3. International Foods & Fragrences (IFF) - Paul Fribourg (Director) bought roughly $20,000,000 of IFF at an average price of $74.29/share on June 1, 2026, but it wasn't reported until June 2, 2026. (Source)

Over 2,000 people have already signed up for my FREE Masterclass video on how to unlock my exact strategies for finding winning stock/options trades! I'll share everything including how to find what Politicians and CEOs are buying. Don’t miss your chance to get in for FREE before spots fill up!

INFOGRAPHICS FOR THE WEEK:

CONTACT US: [email protected]

Responses