TOP NEWS AFFECTING THE STOCK MARKET THIS WEEK:

-

War In The Middle East: A Buying Opportunity? (Source)

Stocks mentioned: $SNOW, $ALAB, $NBIS, $HOOD, $GLD

The U.S. didn’t just bomb Iranian nuclear facilities, it reset the global balance of power overnight. In the early hours of June 22, two American B-2 stealth bombers dropped “bunker-busting” munitions on key Iranian nuclear sites, marking the country’s most direct military escalation in the region since the Iraq War. This isn’t another tit-for-tat strike. It’s a signal: the U.S. is no longer content watching from the sidelines. And while headlines scream about the start of World War 3, we at CEO Watchlist are here to help navigate investors on what the potential outcomes could be from this, as well as how we are positioning our stock portfolios.

Here’s the hard truth...the U.S. getting involved in the Israel-Iran war is not good for the stock market. This will without a doubt increase volatility and cause investors to sell-off their risk-on assets (growth, tech, high-risk stocks). Iran will more than likely retaliate, further escalating the tensions between them and the United States. The Strait of Hormuz, through which 20% of the world’s oil flows, is now a geopolitical chokehold. Iran has already threatened to close it in retaliation, and even the threat alone has sent crude prices spiking. This bottleneck isn’t just about oil; it’s about supply chains, semiconductor shipments, and global inflation. In the short term, volatility is inevitable. But in the long term, data tells us this could be a "buy the dip" opportunity (infographic at the end of the article).

The market fears war, but investors should fear missing the rebound more. History shows that geopolitical shocks, even ones involving Iran or broader Middle East tensions, rarely cause prolonged selloffs in U.S. equities. Here are the stocks on our watchlist that we are keeping our eyes on, that could benefit if we get geopolitical de-escalation, and a return to a risk-on environment:-

Snowflake (SNOW) – Cloud data infrastructure is the foundation of AI and enterprise analytics, and Snowflake is still in the early innings of monetizing its data-sharing flywheel. War jitters delay contracts. Peace accelerates digital transformation. SNOW becomes a beneficiary of renewed enterprise spend.

-

Astera Labs (ALAB) – One of the most promising new names in the AI hardware stack, Astera enables high-speed connectivity between chips. As the AI race heats up, so does demand for faster infrastructure. Tensions abroad may rattle chips short term, but easing fear and falling yields create the perfect window for ALAB to rerate higher.

-

Nebius (NBIS) – Backed by Jeff Bezos, this lesser-known AI infrastructure play is rapidly expanding its global data footprint. With strategic investment in scalable data solutions, NBIS benefits from the global race to build sovereign AI stacks, and especially shines when geopolitical risk premiums compress.

-

Robinhood (HOOD) – The ultimate barometer of retail risk appetite. HOOD benefits directly from falling VIX, rising crypto, and renewed interest in equity speculation. War creates selling pressure and fear. Peace reignites momentum and greed. We recently highlighted Robinhood in the Investment Club, due to significant insider buying that we haven't seen in years! If you want to read how we are positioning our personal portfolios around this news, click HERE.

Now, if things were to continue to escalate, and the U.S. officially declared war on Iran, we would expect the stock market would struggle and have an even deeper sell-off. If that's the case, we would be looking to buy assets such as Gold (GLD) and defense stocks. The takeaway is simple: war panic is not always a reason to sell, it’s often a good buying opportunity, but it's also not always a reason to buy. We will continue to watch all the news coming out of the middle east, and keep Club Members updated on everything news-related and stock-related at this link HERE. Don't forget to keep a cool head during volatile times like this, and try to avoid making emotional decisions about your investments. The U.S. still remains insulated, global markets prefer diplomacy, and volatility normally will always create mispriced opportunities in the stock market...our job is to find where that opportunity is.

-

-

Semiconductor Stocks In Trouble? We Believe These 4 Stocks Can Still Win... (Source)

Stocks mentioned: $NVDA, $AMD, $ASML, $KLAC, $LRCX, $AMAT

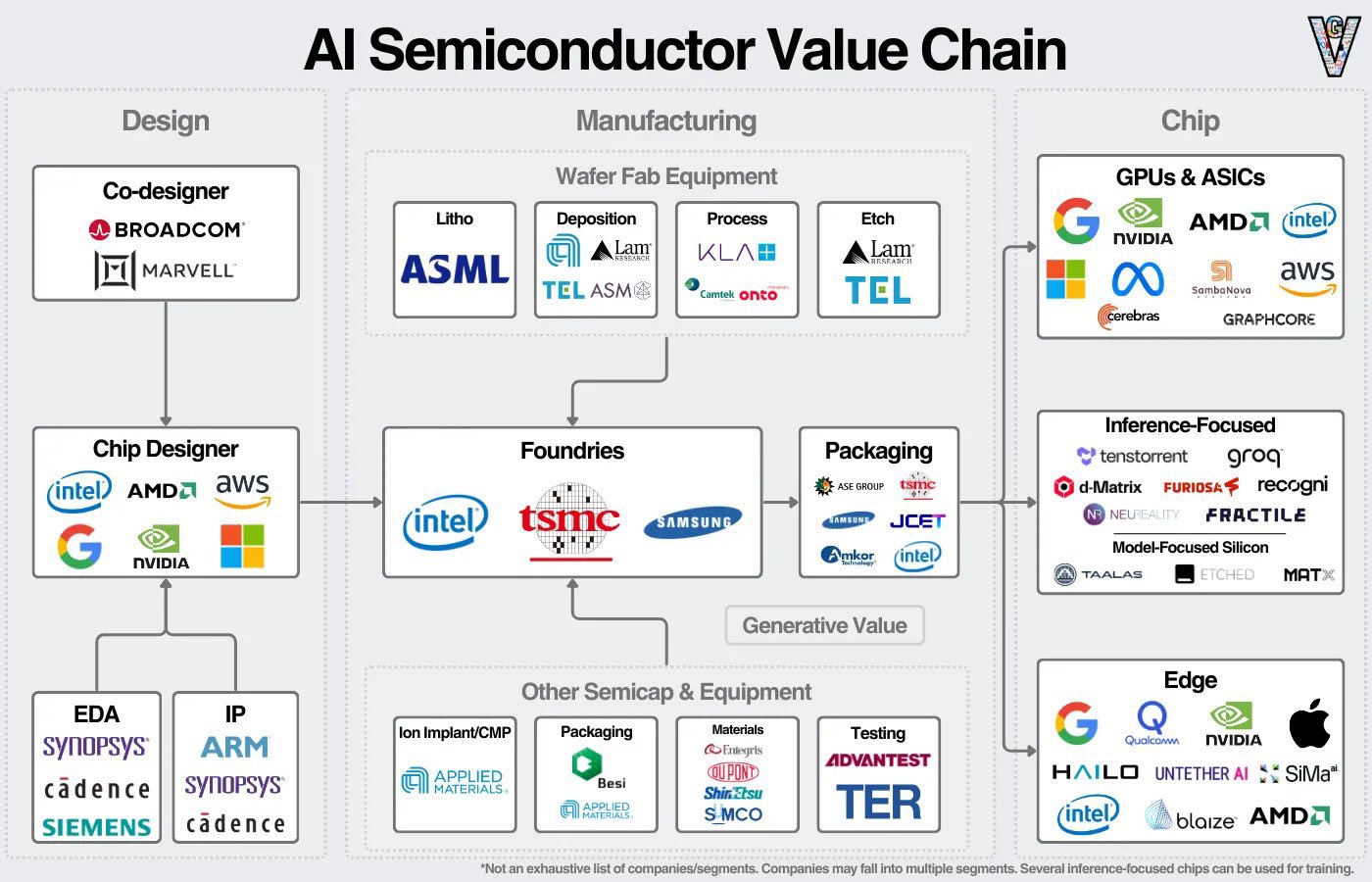

Everyone’s looking at China, but the smarter investors are looking behind the chips. Trump’s new sweeping restrictions on AI chip exports to China are rattling markets, Nvidia (NVDA) is down, Advanced Micro Devices (AMD) is volatile, and the headlines scream of geopolitical escalation. But here’s what they’re missing: these export bans don’t cut off the future of the semiconductor industry, they reroute it. The bottleneck isn’t just compute. It’s the tools that make compute possible. And we still control those.

Trump’s move this past week to further tighten AI chip restrictions is being framed as a tech decoupling event. But it’s actually an industrial consolidation. By limiting China’s access to advanced chips, the U.S. is increasing global dependence on the small handful of companies that make the machines required to manufacture any chip, AI or otherwise. The chip war isn’t about NVIDIA anymore. It’s about lithography, process control, etch, and deposition. These are the new gatekeepers. And they’re not based in China.

The real power lies with the enablers, not the designers. Here are four companies that remain well-positioned, even fortified, by this past week's policy shift:

-

ASML (ASML): The Dutch monopoly on EUV lithography is now more critical than ever. Without ASML’s machines, no country, not even the U.S. can produce leading-edge chips. China's attempts to replicate EUV tech remain years behind.

-

KLA Corp (KLAC): As restrictions increase complexity in fabs, KLA’s process control systems become indispensable. More constraints mean more inspection and metrology, which plays right into KLA’s strength.

-

Lam Research (LRCX): Lam dominates in etching and deposition, key steps in chipmaking that grow in relevance as node sizes shrink. As fabs optimize for non-EUV processes, Lam gains even more utility.

-

Applied Materials (AMAT): The broadest toolset in the industry. AMAT is uniquely positioned across logic, memory, and packaging, segments that will see sustained investment regardless of where chips are designed or sold.

The narrative isn’t “China can’t buy chips”, it’s “China can’t build fabs without us.” These tools aren’t easily replicated. They’re backed by decades of intellectual property (IP), supplier relationships, and software integration. That’s why even amid export bans, demand for these companies’ products continues to rise, sometimes from allies, sometimes even from China itself via workarounds. The point is: the choke point moved upstream, and these companies are the choke point.

The market is mispricing this, while the real power has quietly shifted to the foundational layer of the chip supply chain. Restrictions may hinder volume in the short term, but they concentrate value long term. Investors who see this shift, who bet on the picks and shovels behind the AI gold rush, will be the ones who win. The semiconductor future doesn’t belong to who uses the chips. It belongs to who enables them.

-

-

Tesla’s Next Trillion Dollars Won't Be From Their Cars...It'll Be From Their Battery Technology!! (Source)

Stocks mentioned: $TSLA, $META, $MSFT, $AMZN, $FLNC, $NEE

Wall Street still thinks Tesla (TSLA) is an automaker. That’s a mistake. The next $1 trillion wave will be built not on electric vehicles (EVs), but on infrastructure that powers the age of intelligence, and Tesla is quietly positioning itself at the center. With its latest move to build China’s largest grid-scale battery project, Tesla isn’t just exporting products. It’s exporting infrastructure dominance. The market has overlooked this pivot, and a handful of other companies are sprinting through the same door.

The macro story is bigger than EVs. As AI workloads explode and computing energy demand soars, the world is facing a power bottleneck. The future may be constrained by chips, but what good are chips if you don't have the energy to power them? This creates a new class of winners: companies that can store, route, and monetize electricity at scale. We’re entering an era where every tech company becomes an energy company, or gets left behind. We've seen this with companies like Meta (META), Microsoft (MSFT), and even Amazon (AMZN), all investing in energy infrastructure. What matters most now is control over when and where the energy flows.

Here are the stocks we believe are well positioned to capitalize on this secular convergence:

-

Tesla (TSLA) – Beyond vehicles, Tesla Energy is building global-scale battery projects that act as the backend for renewables and AI data centers alike. Megapacks are becoming the “Amazon Web Service (AWS) of energy”, programmable, deployable, and monetizable power blocks. This China project is just the start.

-

Fluence Energy (FLNC) – A pure-play energy storage provider, Fluence builds battery systems and energy optimization software that help utilities stabilize demand. It’s the less-hyped, more focused cousin of Tesla’s energy unit, and it’s rapidly expanding across Asia and Europe. This is an EXTREMELY HIGH RISK stock with just over a $1 billion market cap and poor financials, but if they can execute on their goals, anything is possible.

-

NextEra Energy (NEE) – America’s largest renewable energy utility is sitting on the kind of generation + distribution infrastructure that AI firms and cloud giants will be forced to partner with. NextEra’s real moat? It owns the grid connections and knows how to monetize volatility.

The world’s defining constraint is shifting from processing power to electricity. The companies that can bridge the two, who understand that tech runs on electrons, not just code, will become the new monopolies. Tesla is no longer just a car company. It’s an energy stack company and the market hasn’t priced that in, yet. Now, if you're an Investment Club Member with us, and haven't seen our updated stock portfolio, we actually own a few stocks mentioned in this newsletter, so CLICK HERE to access it now becuase we have made some rotations recently! However, if you're not a member yet and have been wanting to join, then CLICK HERE to join today, as we are offering access to The Club for only $150 (rather than our normal $500 price).

-

INSIDER TRADES FROM THE WEEK:

1. L3Harris Technologies (LHX) - Markwayne Mullin, Senator of Oklahoma, bought between $15,001-$50,000 of L3Harris Technologies stock on May 13, 2025, but it was reported to the public on June 11, 2025. (Source)

2. RTX Corp. (RTX) - John Boozman, Senator of Arkansas, bought between ~$1,001-$15,000 of RTX Corp. stock on May 30, 2025, but it was reported most recently to the public on June 14, 2025. (Source)

3. Perpetua Resources (PPTA) - Paulson & Co., a hedge fund and 10% owner of the company, bought ~$99 million worth of Perpetua Resources stock on June 16, 2025, but it wasn't reported to the public until June 19, 2025. (Source)

UNLOCK ALL INSIDER TRANSACTIONS BY JOINING THE INVESTMENT CLUB. JOIN TODAY FOR ONLY $150!!!

INFOGRAPHICS FOR THE WEEK:

CONTACT US: [email protected]

Responses