TOP NEWS AFFECTING THE STOCK MARKET THIS WEEK:

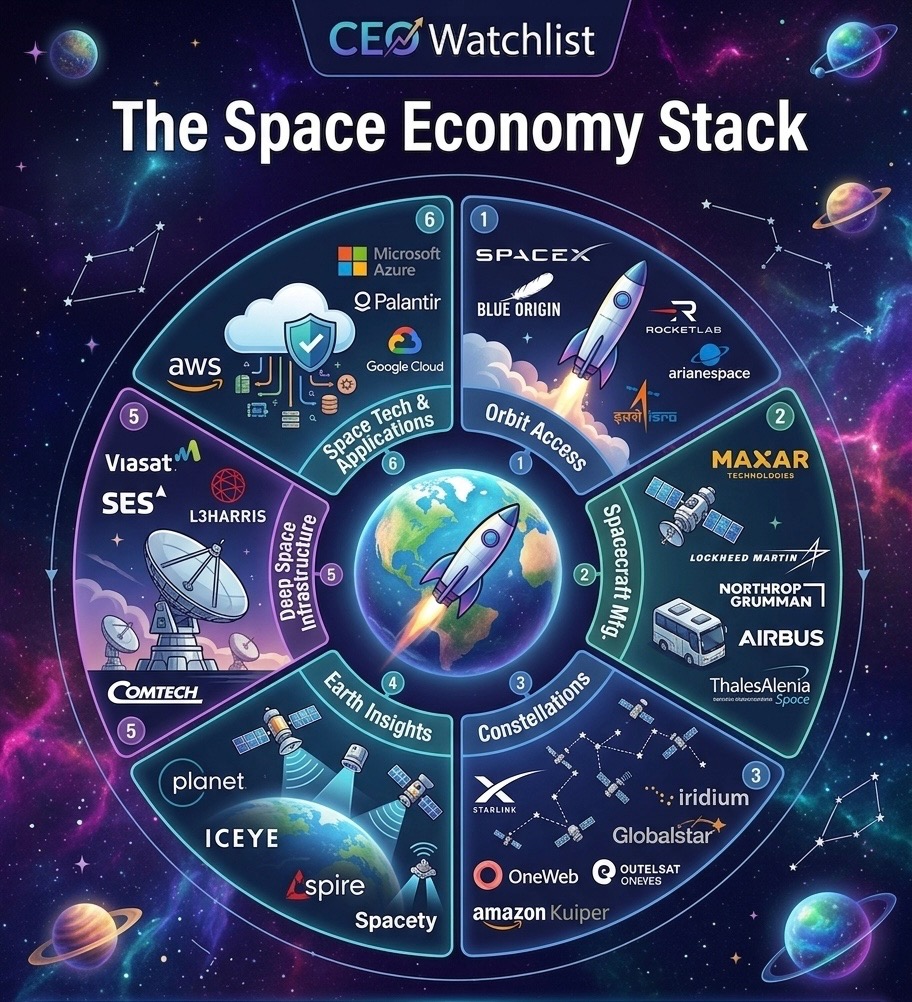

SpaceX Rockets Higher After Going Public ... But These Are The 3 Stocks We Would Rather Buy Today!!! (Source)

Stocks mentioned: $SPCX, $RKLB, $PL, $ASTS, $AMZN, $GOOG, $MSFT, $CRWV, $ALAB, $NBIS

If you weren't paying close attention this past week, you missed one of the biggest moments in modern market history. This past Friday, Space Exploration Technologies (SPCX), Elon Musk's rocket and satellite company, went public. For anyone newer to investing, "going public" happens through an IPO, which stands for Initial Public Offering. It's the moment a private company sells shares to everyday investors on the stock market for the first time, so instead of only a handful of wealthy insiders owning pieces of the company, anyone can now buy in. And this wasn't just any IPO. SpaceX listed on the Nasdaq under the ticker "SPCX" and became one of the world's biggest public companies on its very first day, valued above $2 trillion!

For those who don't know the company, SpaceX builds and launches rockets, and its crown jewel is "Starlink", a satellite internet service that beams broadband down from space to people all over the planet. Starlink is SpaceX's only profitable segment and its biggest revenue maker, which tells you a lot about where the real money is coming from. So why is the market handing this company a $2 trillion price tag? In our view, it comes down to one word: monopoly. SpaceX essentially owns the launch market with roughly a 90% market share. When NASA, the U.S. military, or a private company needs to put something into orbit, SpaceX is very often the only realistic option, and that kind of dominance is rare and incredibly valuable. Layer on Starlink's global internet ambitions and the company's push into AI and space-based data centers, and you can understand why investors are this excited about the long-term story.

We think SpaceX will likely do very well over time. Here's our hesitation, though: at $2 trillion, the stock is just a bit overcrowded. For a company that's bringing in roughly $20 billion a year, and is being valued at $2 trillion, despite their monopoly status, it's hard to wrap our head around that type of multiple. And when we say $20 billion, that's in revenue, not even their net profits. For those that don't know, SpaceX is not profitable. They reported a net LOSS of $4.3 billion in their first quarter. So as my dad used to tell me, "it's a good stock, but a bad stock price". But whether or not we think its overvalued there, the market trends to allow high valuation stocks run longer than they should, so we can't tell you whether or not the stock will go up or down from here, all we can give you are the fact, and the facts are it's a very expensive stock and very high risk to own here. When we compare it with an Amazon (AMZN) or a Meta (META), we have Amazon at a $2.5 trillion market cap, and Meta at a $1.5 trillion market cap. The difference here is, unlike SpaceX who's only earning $20 billion a year, Amazon is bringing in roughly $740 billion a year, and Meta is bringing in roughly $200 billion a year. That should put it in better perspective for those of you who haven't had a chance to dive into the financials. Now obviously there are other factors such as the growth rate going forward, as well as a multitude of other things, but all in all, I think everyone can agree that SpaceX is expensive. Great, but expensive.

Now here's where it gets interesting, and where we think the real opportunity lives. When a giant like SpaceX goes public, money doesn't appear out of thin air to buy it. A lot of that money gets pulled out of other stocks in the same sector. And that's exactly what happened. As SpaceX soared on its debut, the rest of the space sector got hammered as investors sold what they already owned to chase the shiny new name. Space stocks extended their losses after SpaceX began trading, with Rocket Lab (RKLB) dropping at least 10%, and satellite names including Planet Labs (PL) and AST SpaceMobile (ASTS) each shedding 8-10% as well. But we urge investors not to panic as this is a completely normal dynamic. Think of it like a brand-new, flashy restaurant opening on a block that already has several solid spots. On opening night, everyone crowds into the new place and the established restaurants sit half-empty, not because their food got worse, but because attention and dollars temporarily flooded to the new arrival. That's what's happening to the smaller space names right now. Their businesses didn't deteriorate. The crowd just stampeded toward the SpaceX IPO, which can be temporary.

As long-term investors, we look at that gap and see opportunity rather than a reason to panic. Here's the core thesis: if the space economy turns out to be as big as we think, it's very unlikely that one company captures all of it. Just like the internet didn't produce a single winner but instead created Amazon (AMZN), Google (GOOG), Microsoft (MSFT), and countless others, a thriving space economy should lift multiple players, not just SpaceX. And right now, several of those players are trading at meaningful discounts while everyone's distracted:

- Planet Labs (PL) - Operates a fleet of small satellites that image the entire Earth daily, selling that data to governments, agriculture, and defense customers. The stock is currently sitting around 40% off its highs.

- AST SpaceMobile (ASTS) - Building a space-based cellular network designed to connect regular smartphones directly to satellites, no cell towers needed. A genuinely ambitious play on closing the global connectivity gap, also down roughly 40% from its highs.

- Rocket Lab (RKLB) - The clearest "second mover" in launch, providing rocket launches and building spacecraft and satellite components, with its larger Neutron rocket on the way. The stock is down about 30% from its highs.

Of the 3 names, our personal favorite is Planet Labs (PL), but a very close second would be Rocket Lab (RKLB). One very bullish piece of news specifically for Rocket Lab this past week was this last Thursday, it was announced that they would be added to the Nasdaq-100. This is extremely bullish because whenever a stock is added to a major index, firms need to go out and buy the stock, so with Rocket Lab being down the day after the inclusion announcement, that this could be an opportunity to get this name at a discounted value, if you are looking 3-6 months out. At least, that is what we are personally doing. But, Rocket Lab wasn't alone, other names announced to join include: CoreWeave (CRWV), Astera Labs (ALAB), and Nebius Group (NBIS), all of which are under $80 billion market caps. So while SpaceX commands a $2 trillion-plus valuation on day one, these smaller names are being handed to patient buyers at 20-40% discounts, which to us looks far more attractive.

Let's tie it all together. SpaceX pulled off the largest IPO in history this past Friday, debuting above a $2 trillion valuation on the strength of its launch monopoly and Starlink's profitability, and we genuinely believe in the long-term story even if the stock looks crowded and richly priced at these levels. The predictable side effect was a sell-off across the rest of the sector, with Planet Labs, AST SpaceMobile, and Rocket Lab all getting knocked down as capital rotated into the headline name. But that rotation is precisely what creates the opening. If the space economy delivers, the winners will be plural, not singular, and the smaller names now sitting 30-40% off their highs (with Rocket Lab even earning a Nasdaq-100 promotion in the process) represent the kind of value gap long-term investors dream about. The crowd is staring at the rocket on the launchpad. We're keeping one eye on everything it's leaving behind.

The War In Iran Might Be Coming To A Close: What That Means For Your Portfolio... (Source)

Stocks mentioned: $NBIS, $DELL, $MRVL

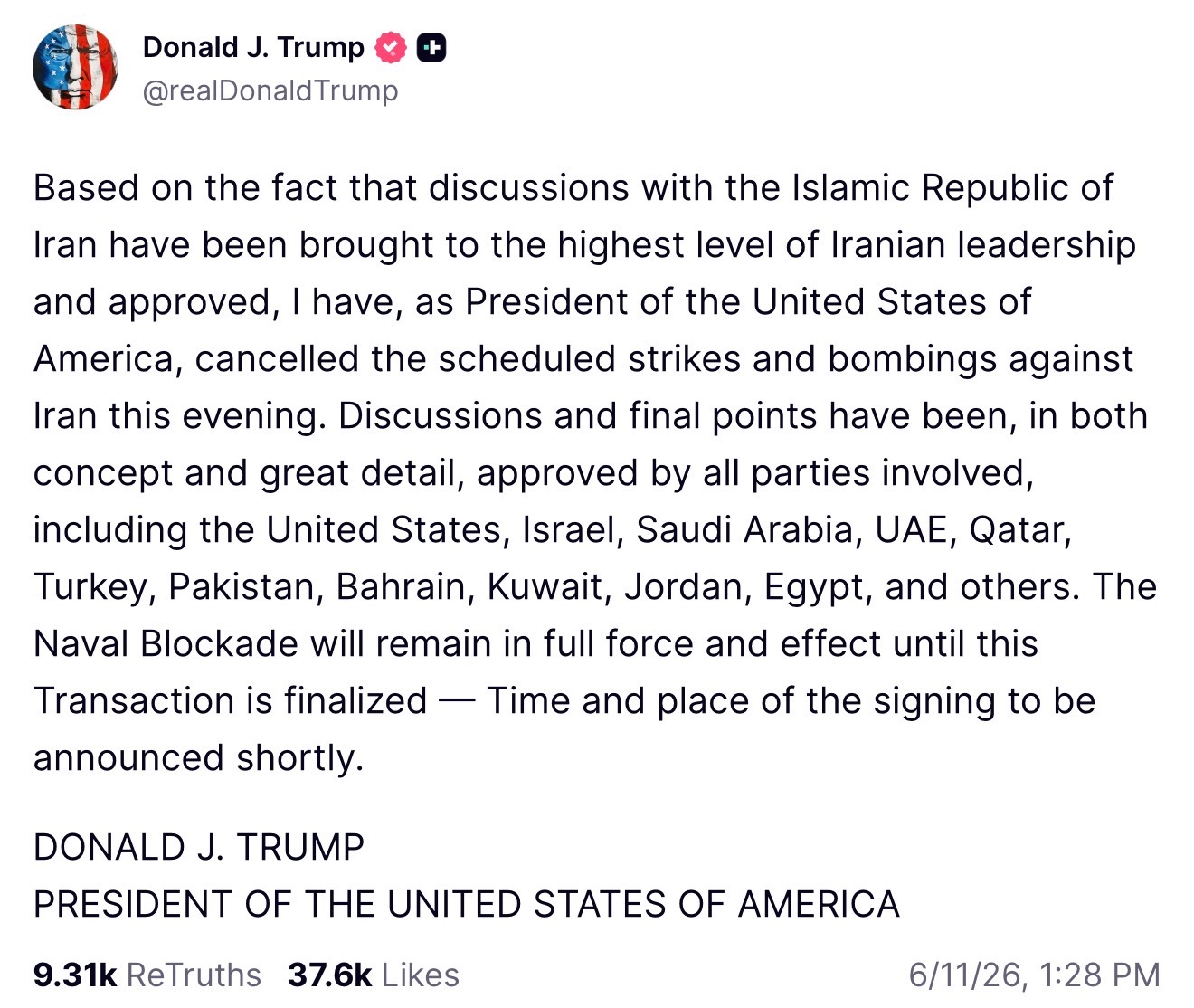

For more than 3 months now, the U.S. has been entangled in a war with Iran, and it's been rattling markets the entire time. The flashpoint has been the Strait of Hormuz, a narrow stretch of water that sounds obscure, but is one of the most important spots on the planet. Iran effectively shut it down, and roughly 20% of the world's energy supply travels through that single waterway. When you choke off a fifth of global oil and gas, prices spike everywhere, and that's exactly what's been happening, with gas and electricity prices climbing and weighing on the whole economy. Now, finally, there's real movement toward peace. On Thursday, Trump said he called off new military strikes on Iran, claiming a breakthrough in negotiations to end the war, and as of Friday, he said a deal to end the war and reopen the Strait of Hormuz could be signed "maybe over the weekend in Europe," while Pakistan's prime minister said the deal's final text had been agreed upon. After months of conflict, we're genuinely close to the finish line, at least that's what we've been told...

Here's the catch, and it's an important one. We've seen this movie before, and the ending keeps getting rewritten. Trump has said multiple times in recent weeks that the two sides were on the cusp of a deal without anything actually coming to fruition. So while there's been a lot of progress, we'd be lying if we told you this is a sure thing. Now to the part that matters for our portfolio. If this deal is real and it holds, the setup for stocks is about as bullish as it gets. Wars create uncertainty, and uncertainty is the one thing markets hate more than bad news. The moment that fog lifts, oil prices should ease, inflation pressure should cool, and investors who've been sitting on the sidelines tend to come flooding back in. Think of it like a pressure valve finally releasing. Markets have been holding their breath for 3 months, and a genuine peace deal lets everyone exhale at once. In a scenario like that, nearly everything can move up, but the names that historically run hardest are the growth stocks, the higher-octane companies whose value is tied to future expansion rather than steady dividends. We're specifically eyeing the AI and tech infrastructure complex, names like Nebius (NBIS), Dell (DELL) and Marvell (MRVL). These are the kinds of stocks that tend to get hit hardest during fear, and bounce hardest during relief, which is exactly why they're on our radar for a resolution scenario.

But here's where we have to be disciplined, because the same coin has a much uglier flip side. If this deal falls apart the way the previous attempts did, the market reaction would likely be just as violent in the opposite direction. The high-flying growth names that would soar on good news are the very same ones that would get punished hardest if the talks collapse and the strikes resume. That's the nature of high-growth stocks: they give you the most upside and the most downside. So as much as we like the bullish setup, we are not betting the farm on a politician's tweet. Smart positioning here means managing risk, sizing positions so that a failed deal doesn't wreck you, and keeping some dry powder in case things fall out. We want exposure to the upside, but we refuse to be defenseless against the downside. Conviction and caution aren't opposites here. They're partners.

So let's bring it all home. After more than 3 months of a war that's strangled global energy supply through the Strait of Hormuz and pushed prices higher across the board, we're closer than ever to a deal, with Trump calling off strikes and pointing to a possible signing this week. The progress is real, but so is the track record of near-misses and the open skepticism coming out of Tehran, so nobody should treat this as a "done deal" until it's actually signed. If it does come together, the relief rally could be powerful and broad. If it falls apart, those same names lead the drop, which is precisely why we're pairing our optimism with real risk management rather than blind faith. We're hopeful, we're watching closely, and we're ready to move the moment we get clarity. Until the ink is dry, though, we're keeping one hand on the wheel and one eye on the exit.

"Super Investor" Spotlight: David Tepper (Source)

Stocks mentioned: $AMZN, $MU, $GOOG, $UBER, $TSM, $BABA, $VST, $EWY, $NVDA, $NRG

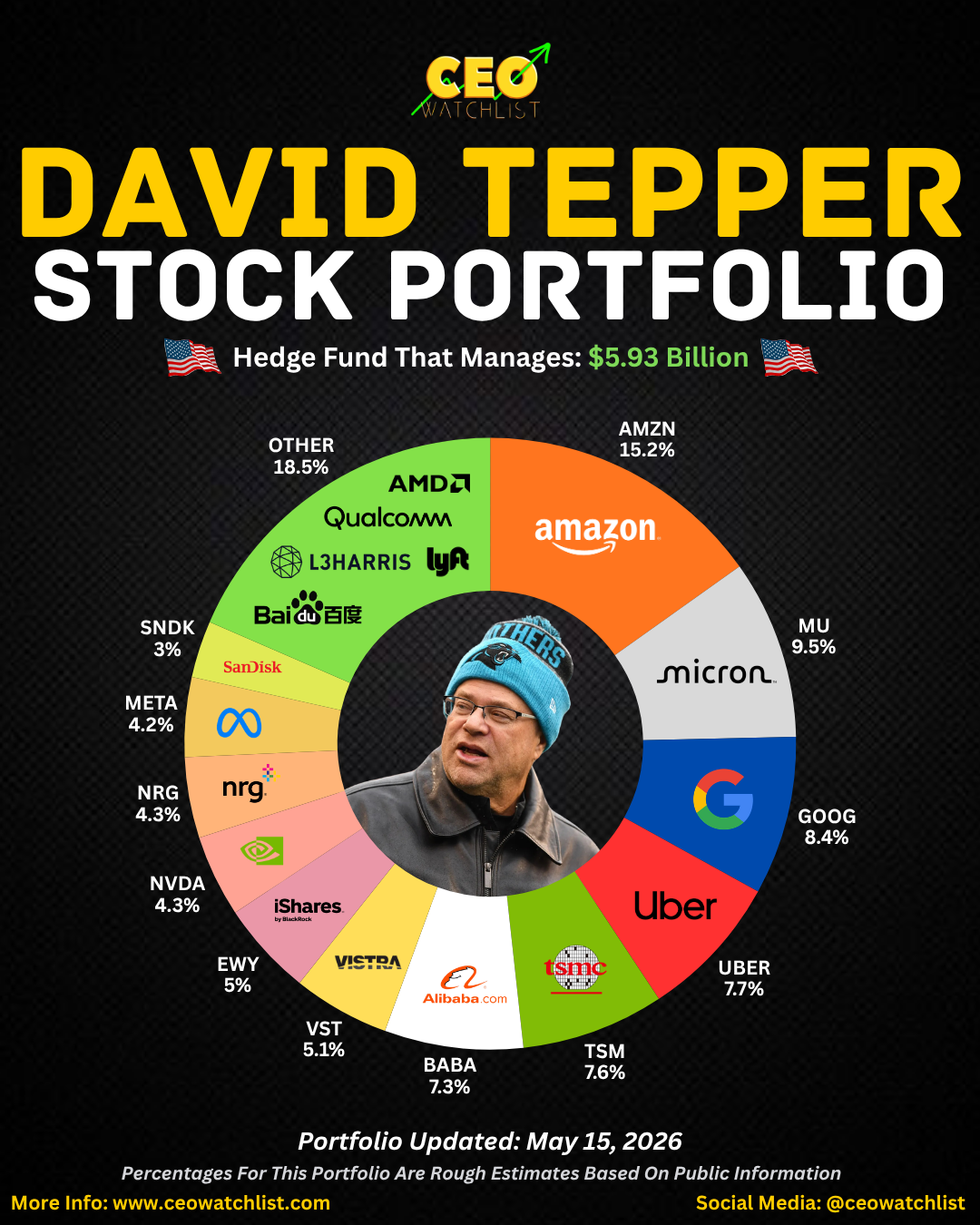

If you've spent any time in investing circles, you've probably heard people obsess over what the "smart money" is buying. That obsession has a name: "Super Investors". A "Super Investor" is a fund manager or firm with such a strong long-term track record and such deep market instincts that the rest of us literally watch their moves for clues. By law, any institution managing over $100 million has to file a 13F every quarter, which is a public document listing the U.S. stocks they own. It's basically a peek into the smart money's hand, filed up to 45 days after the quarter ends. And this week we're zeroing in on one of the most respected and aggressive minds in the game: David Tepper.

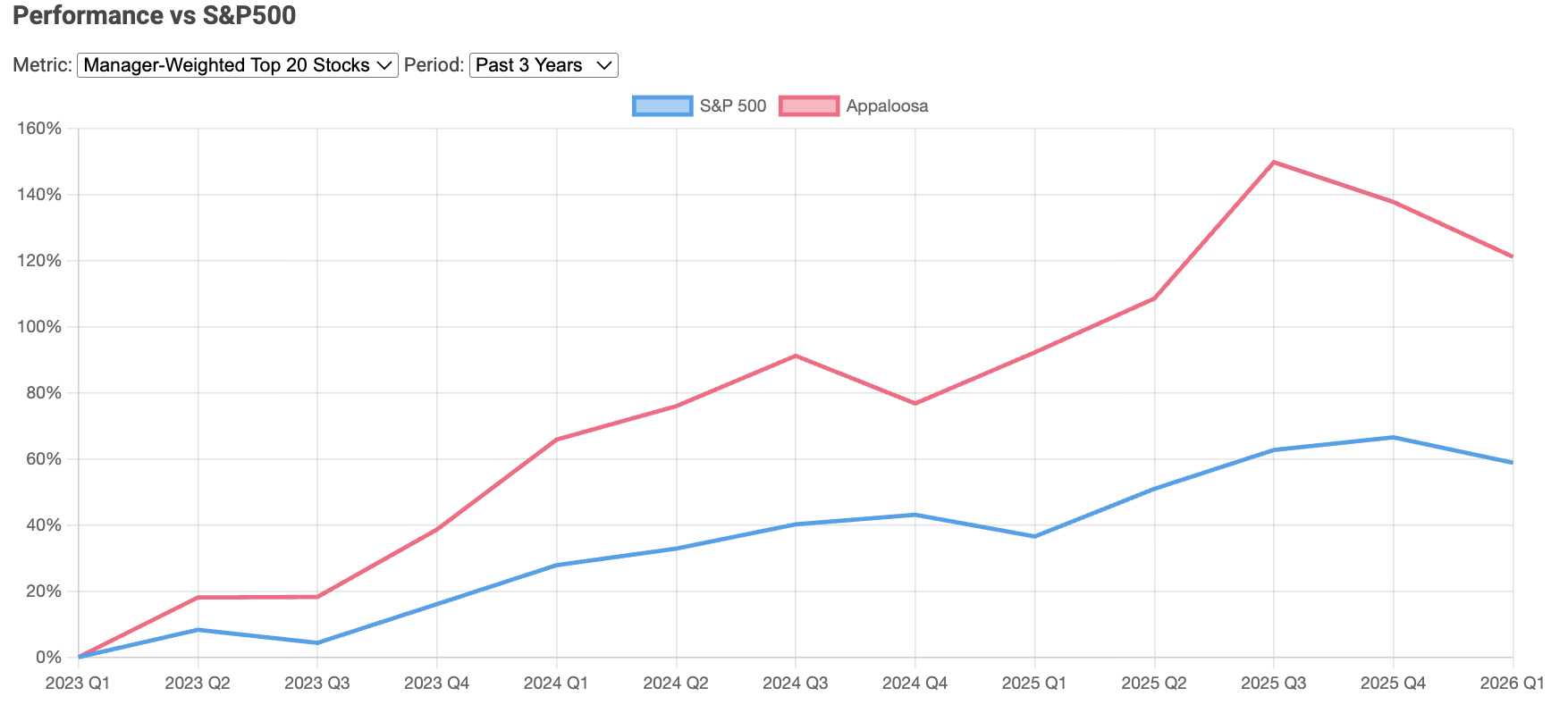

Tepper runs Appaloosa Management, the hedge fund he founded back in 1993, and he has a reputation as one of the boldest contrarians alive. His thing is buying when everyone else is panicking, then sizing up huge when he has conviction. He's also famous outside of finance as the owner of the NFL's Carolina Panthers (that's him in the Panthers beanie in the infographic below). The track record speaks loudly: over the past 3 years his manager-weighted top holdings returned roughly 121%, versus about 58% for the S&P 500 over the same stretch, as you can see below:

That's more than double the overall market's return, and it's exactly why people lean in when his 13F drops. His reported book currently manages around $5.93 billion in stocks, so with that all said, you are probably wondering which stocks he owns.

Without further ado, here are the top 10 holding in his stock portfolio, as well as the weighting for each one:

- Amazon (AMZN) - 15.2%

- Micron (MU) - 9.5%

- Google (GOOG) - 8.4%

- Uber (UBER) - 7.7%

- Taiwan Semiconductor (TSM) - 7.6%

- Alibaba (BABA) - 7.3%

- Vistra (VST) - 5.1%

- iShares MSCI South Korea ETF (EWY) - 5%

- Nvidia (NVDA) - 4.3%

- NRG Energy (NRG) - 4.3%

So what's the takeaway? Tepper's book is a masterclass in buying unloved value while still riding the AI and power megatrends everyone agrees on. The lesson isn't "go buy Alibaba," it's that the best investors hunt where fear has pushed prices down, then concentrate when conviction is high. We like this portfolio as a teaching tool because it shows discipline: diversified across themes, anchored by a massive Amazon position, but unafraid to make contrarian calls.

INSIDER STOCK TRADES FROM THE WEEK:

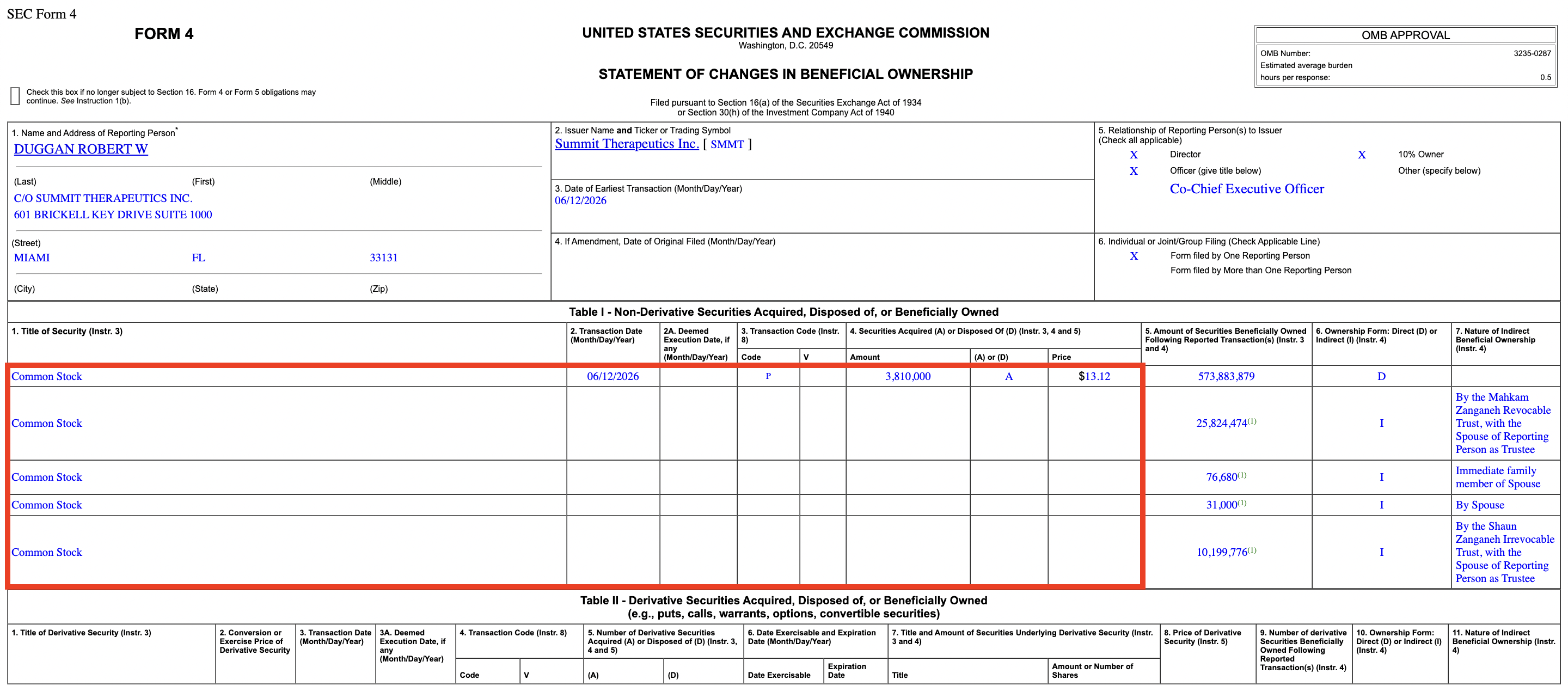

1. Summit Therapeutics (SMMT) - Robert Duggan (Billionaire, Co-CEO) bought roughly $50,000,000 of SMMT at an average price of $13.12/share on June 12, 2026, and it was reported to the public later that same day. (Source)

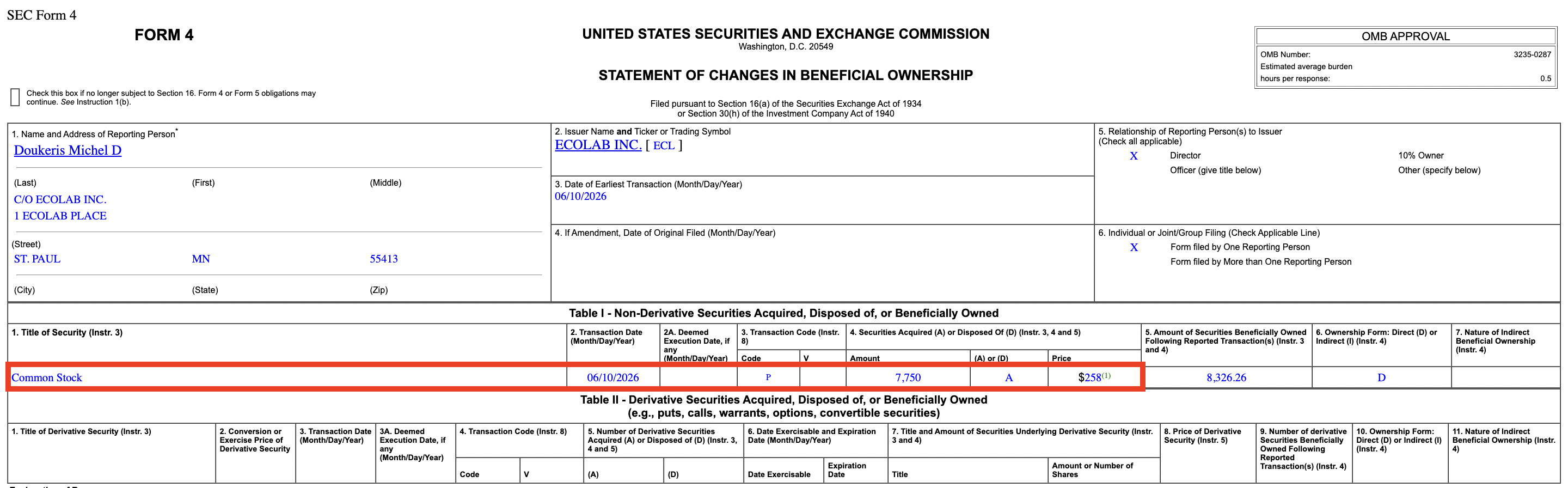

2. Ecolab (ECL) - Michel Doukeris (Director, CEO of AB Bev, the largest beer company in the world) bought roughly $5,000,000 worth of ECL at an average price of $258.00/share on June 10, 2026, but it wasn't reported to the public until June 11, 2026. (Source)

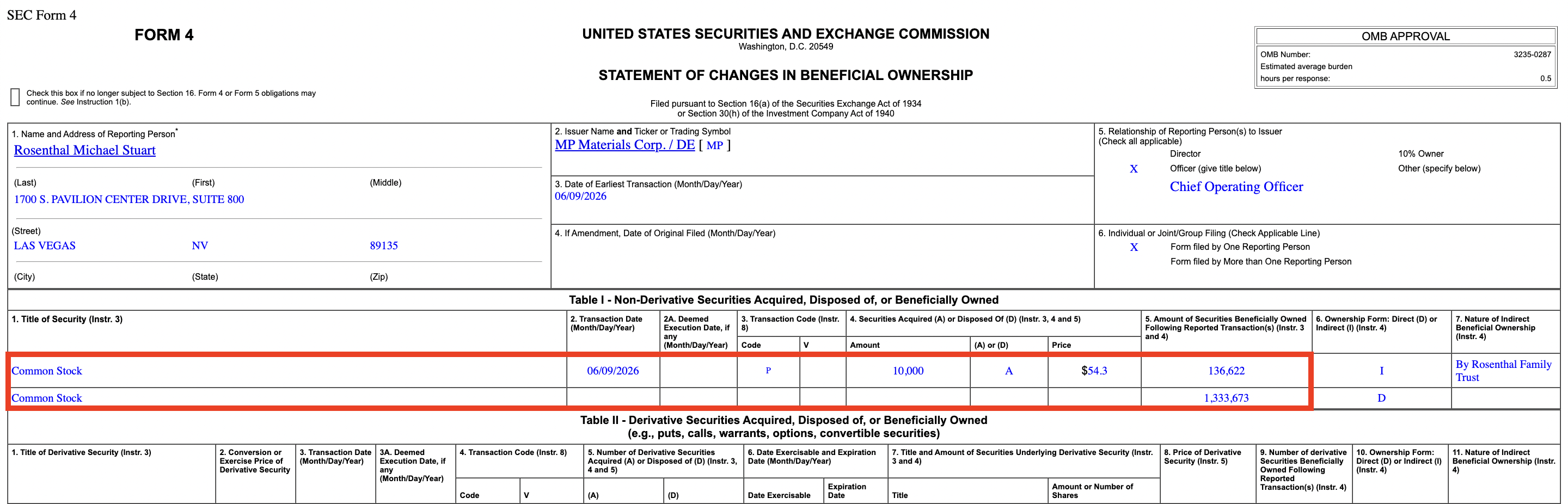

3. MP Materials (MP) - Michael Rosenthal (Director) bought roughly $500,000 of MP at an average price of $54.30/share on June 9, 2026, but it wasn't reported until June 10, 2026. (Source)

Over 2,000 people have already signed up for my FREE Masterclass video on how to unlock my exact strategies for finding winning stock/options trades! I'll share everything including how to find what Politicians and CEOs are buying. Don’t miss your chance to get in for FREE before spots fill up!

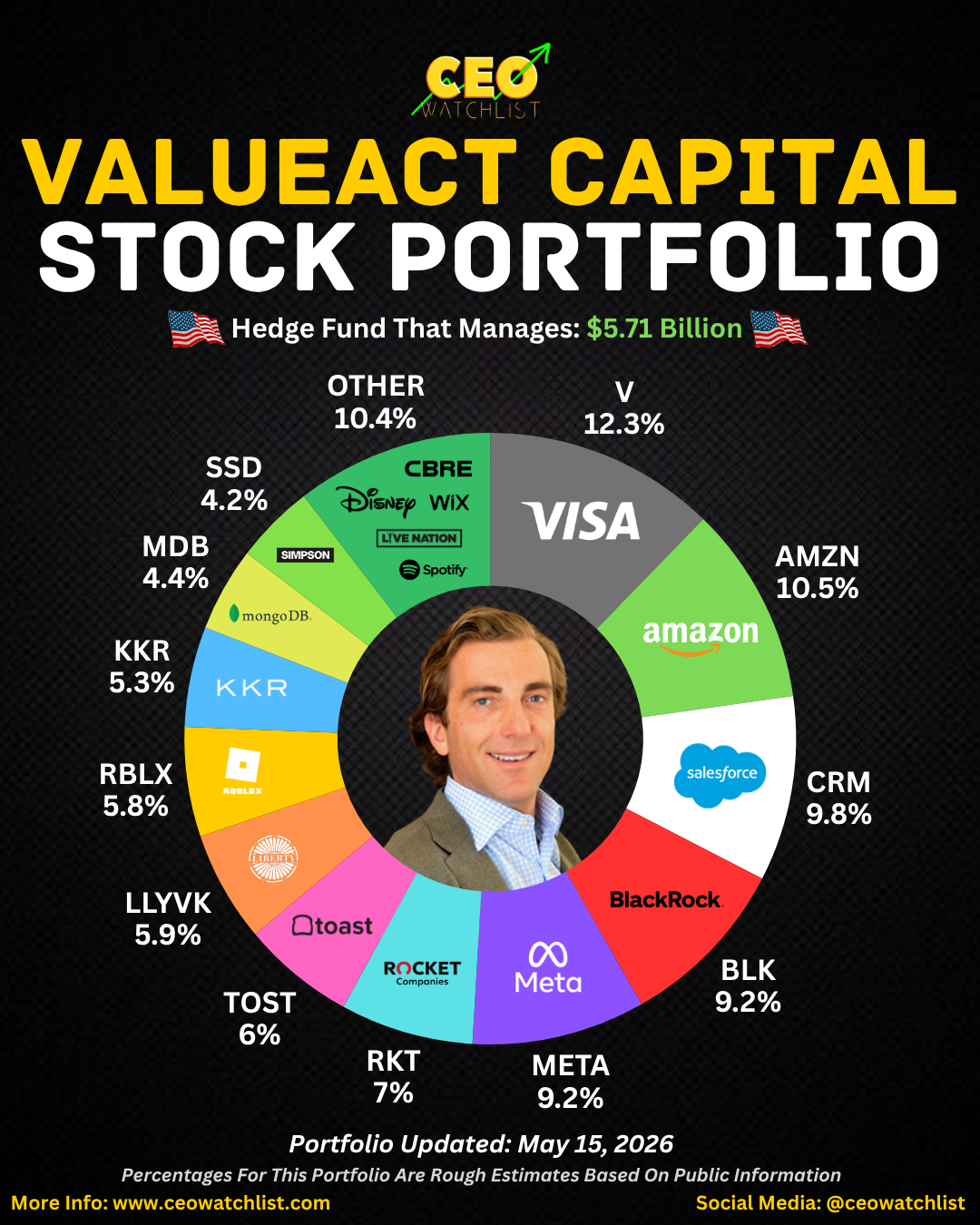

INFOGRAPHICS FOR THE WEEK:

CONTACT US: [email protected]

Responses