TOP NEWS AFFECTING THE STOCK MARKET THIS WEEK:

-

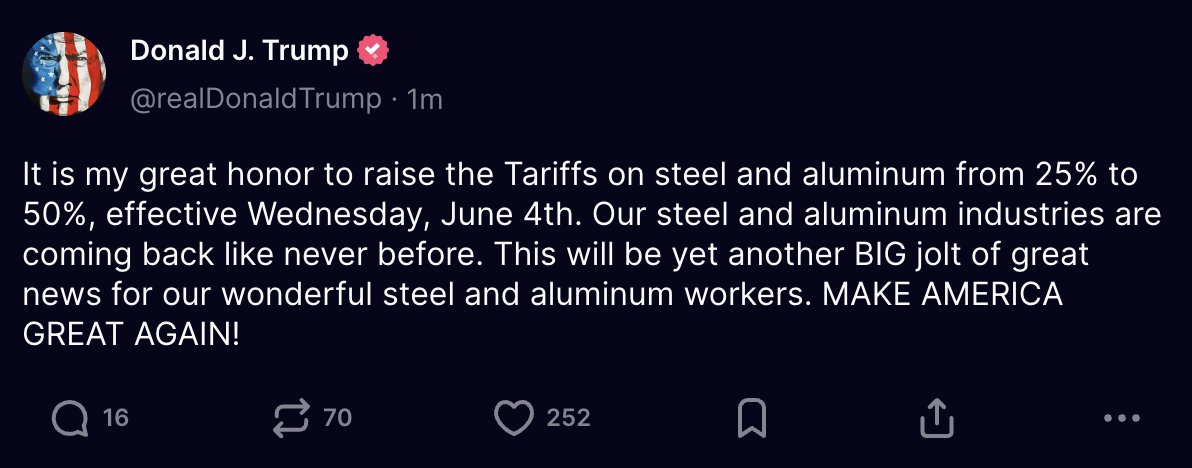

Trump's Tariff War On Steel: The 4 Stocks That Are Set To Benefit The Most (Source)

Stocks mentioned: $CLF, $NUE, $CAT, $AA

Conventional wisdom says trade wars hurt everyone. But what if that's wrong? Trump’s decision to double tariffs on foreign steel, from 25% to 50%, isn't just political theater. It’s a forced acceleration of a long-overdue reshoring movement. While pundits focus on legal battles and diplomatic blowback, investors should be asking a sharper question: Which American companies are now strategically positioned to absorb demand, command pricing power, and scale into protected market share? Because when governments set the rules, capital flows accordingly.

This isn’t 2018. Back then, tariffs were reactionary. In 2025, they’re part of a full-spectrum industrial policy shift, bolstered by AI-led infrastructure growth, national security narratives, and bipartisan skepticism toward China. The core constraint isn’t global demand; it’s domestic capacity. American industry lacks redundancy in high-quality steelmaking, fabrication, and downstream applications like construction and defense. If the courts uphold the tariffs, or even delay their repeal, the capital investment cycle in U.S. steel, aluminum, and industrial automation could reignite. The stocks best positioned? Not just the steelmakers, but the enablers of American capacity and complexity.

Here are 4 public companies primed to benefit from this reshuffling of global industrial flows:

-

Cleveland-Cliffs ($CLF) – America’s largest flat-rolled steel producer with vertically integrated operations, including its own iron ore mines. Tariff protection improves margins and gives them leverage in contract negotiations.

-

Nucor ($NUE) – A low-cost leader in mini-mill steel production with a strong clean energy narrative. Rising prices and domestic sourcing mandates increase Nucor’s pricing power.

-

Caterpillar ($CAT) – Heavy machinery demand will spike as new U.S. steel infrastructure projects gain momentum. CAT is a downstream beneficiary of stimulus and reshoring.

-

Alcoa ($AA) – While tariffs focus on steel, aluminum producers like Alcoa gain from the same supply chain trends, especially as China dominates global aluminum exports.

Most investors will over-index on legal uncertainty and headlines. Smart capital will focus on production bottlenecks, supplier lock-in, and labor dynamics. These tariffs are not a temporary political stunt, they’re a catalyst. The Biden administration’s infrastructure agenda laid the groundwork. Trump’s tariffs add enforcement teeth. And if Trump retakes the White House, expect even more aggressive industrial policy. Either way, reshoring is no longer optional, it’s strategic. And the winners will be those who front-run the capital expenditures, not just react to the headlines. The Inevitable Conclusion Ignore the noise. What’s happening is the forced rewiring of global supply chains. American industrial equities are no longer cyclical, they’re geopolitical. The market is still pricing them like the old economy, but policy is treating them like the new one. That disconnect is your alpha. The reshoring wave is real, and it's about to hit hard. For those paying attention, this isn’t just a trade war. It’s a buying opportunity.

-

-

The End of the Middleman: Tesla Isn’t Just Competing with Uber, It’s Trying To Replace It! (Source)

Stocks mentioned: $TSLA, $GOOG, $MBLY, $NVDA, $UBER

The ride-hailing economy is under attack! The real war that is being fought in the ride-hailing industry isn’t cheaper rides, it’s no drivers at all. Tesla’s ($TLSA) quiet rollout of a fully autonomous robotaxi fleet in Austin isn’t just a feature launch. It’s a paradigm shift. Investors betting on Uber ($UBER) as a tech-forward logistics play are missing a major point: if Tesla’s robotaxis work, Uber's market share will drop. The platform won’t matter when the product is integrated end-to-end. We’re witnessing the start of a complete vertical collapse in the mobility stack, and Uber’s moat could be drying up.

The automation of mobility isn’t just about cost savings, it’s about control of the customer interface and the entire value chain. For a decade, Uber has enjoyed dominance as the digital dispatcher between human drivers and riders. But Tesla’s move marks a transition from two-sided marketplaces to closed autonomous networks. The constraint has always been autonomy itself: safe, scalable, and reliable vehicles. Now that bottleneck is breaking. What’s about to emerge is a bifurcated world, where only companies that own both the vehicle and the software survive.

This shift unlocks asymmetric upside for a new class of mobility stocks:

-

Tesla ($TSLA) – No longer just an electric vehicle (EV) company, Tesla is now a mobility-as-a-service infrastructure provider. Its robotaxi network integrates manufacturing, software, and distribution into a single stack.

-

Alphabet ($GOOGL) – Waymo is another credible threat to Tesla in autonomy. Its growing fleet in Phoenix and partnership with Uber make it a kingmaker in the space.

-

Mobileye ($MBLY) – Intel’s autonomous vehicle (AV) subsidiary powers several AV platforms. If Tesla and Waymo battle for dominance, Mobileye could quietly power the rest.

-

Nvidia ($NVDA) – The compute backbone of AV. Tesla may use in-house chips, but the broader AV ecosystem is heavily reliant on Nvidia’s DRIVE platform.

-

Uber ($UBER) – A short-term survivor due to partnerships, but a long-term loser unless it pivots from dispatcher to fleet owner. Investors banking on Uber’s network effect need to rethink the risk of disintermediation.

This is not a linear transition. It’s “gradually, then suddenly.” One working fleet in Austin, then one in Miami, then 50 cities. And unlike other moonshots, Tesla controls every layer: vehicle design, AI training, charging infrastructure, and now, deployment. Uber, by contrast, must lease the future through third-party partnerships. And investors must ask: when you can hail a Tesla with no driver, no tip, and zero delay, why would you ever open Uber again? Margins won’t compress, they’ll vanish. The problem for Tesla is not a matter of "if" they will roll-out robotaxis, but moreso the "when".

Tesla has had a long history of missing deadlines and having plenty of delays. We have yet to see an actual roll-out of these robotaxis on any decent size or scale to the public. This is where the concern is for Tesla. While Tesla takes its time rolling out their robotaxis, Uber is partnering with everybody from Google's Waymo to Nvidia. Uber is not sitting on their hands and allowing Tesla to come in and eat up their market share. They are making the necessary partnerships and adapting their business model for a world that is autonomous. We don't believe Uber should be immediately dismissed just because of Tesla's robotaxi. We believe that Uber will become an AV aggregator for all of Tesla's competitors in a one-stop-shop app for all of your delivery and transportation needs. Since "time" and "price" are the two most important factors in this industry, we believe Tesla has a lot of hurdles it must face to compete with Uber at their current scale. The time it takes to get a ride is crucial for the consumer. With Uber's massive network, and Tesla's lack of one, we believe riders are going to prioritize Uber over Tesla due to the quickness of being able to get a ride. We don't believe riders are going to be willing to wait 30 minutes or more due to limited availability of Tesla's in cities, while Uber can get a ride to you in under 5 minutes in said same city. Same thing goes for pricing. Due to Uber's massive fleet, they can offer lower prices, comparable to Tesla, who had a much more limited number of vehicles and will more than likely have a higher price point for rides. For the average person hailing a ride, would they rather spend $25 to ride in a Tesla, or $10 to ride in a Honda? These are the hurdles that Tesla faces, but if they can overcome them and Uber doesn't capitalize on their current lead, then Tesla may just win this race and eliminate Uber as any serious competitor.The robotaxi moment isn’t a rumor, it’s a rupture. Investors still pricing mobility stocks based on labor-driven logistics are blind to what autonomy enables: full-stack dominance. Tesla is building not just the vehicle, but the next Uber, the next Hertz, and the next Google Maps, all in one. Uber may continue to post decent quarters, but structurally, the platform era of transportation is ending. And for those paying attention, that future is grossly underpriced.

-

-

The Bond Market Time Bomb: Why Jamie Dimon's Panic Warning Could Trigger a Massive Wealth Shift, And How to Be on the Right Side of It (Source)

Stocks mentioned: $ARKK, $TDOC, $SHOP, $BX, $BRK.B, $SLV, $GLD, $OXY

When Jamie Dimon, the most powerful banker on Wall Street, says, “You’re going to have a problem, and you’re going to panic,” the world should listen. His latest warning isn’t just about rates going higher, it’s about a systemic crack in the bond market caused by America's unchecked debt binge. The media calls it a “bond market crisis”, but investors need to reframe this moment: it’s not a crisis, it’s a reallocation. A once-in-a-generation capital rotation away from fragile, rate-sensitive assets and toward companies built for chaos.

The macro setup is now undeniable. With the U.S. debt-to-GDP ratio soaring past 120%, Treasury issuance accelerating, and foreign buyers pulling back, supply is overwhelming demand. The Federal Reserve is stuck between inflation and insolvency. This is the “crack” Dimon sees forming: an illiquid Treasury market where yields spike violently, creating volatility in everything from mortgages to megacap stocks. In this environment, highly-leveraged companies and long-duration tech stocks, especially those with unprofitable growth models, face enormous valuation risk. Names like ARK Invest ($ARKK), Teladoc ($TDOC), and Shopify ($SHOP) will be hit hardest. Investors hiding in "safe" long-duration assets are about to discover how exposed they really are.

But chaos breeds opportunity. Certain stocks are engineered for this environment, those tied to real assets, cash flow, and pricing power. Here are five that are positioned to potentially outperform:

-

$BX (Blackstone): With its growing private credit business and direct lending exposure, Blackstone is becoming the new central bank for the private economy. As traditional debt markets freeze, their influence only grows.

-

$BRK.B (Berkshire Hathaway): Sitting on over $300 billion in cash, Warren Buffett is poised to act as buyer-of-last-resort in a distressed bond market.

-

$SLV (iShares Silver Trust): Precious metals remain the ultimate hedge against sovereign debt risk, and silver offers asymmetric upside due to its industrial demand.

-

$GLD (SPDR Gold Trust): Similar to silver, but the more sought after of the two. Gold has always been a hedge for traditional portfolios to shield against volatility and downside risk in the stock market.

-

$OXY (Occidental Petroleum): Real assets, real cash flow, and backed by Buffett himself. Energy companies like Occidental stand to gain as the dollar weakens and real assets outperform.

Dimon is known to be bearish on the markets over the past 5 years, so it is no surprise to hear these statements from him. We at CEO Watchlist believe that the stock market is extremely resilient and won't crack as easily as Dimon may think. We do agree that there is reason for concern in the bond market, but we also believe this modern age investor is able to see past the negative to the inevitable good that is waiting on the other side. With that said, Dimon’s panic isn’t a forecast, it’s a roadmap. The coming dislocation in bonds will not just shake portfolios, it will rewire how capital is allocated for the next decade. The illusion of safety in government debt is cracking, and when it breaks, capital will race toward anything tangible, cash-generating, and resilient. The biggest winners will be those who don’t wait for the panic to start, but position for it now. This is why we teach our students in the Investment Club how to prepare in advance for when the market is going up or going down, that way they can make money no matter what happens in the stock market. We're releasing our latest report on the stocks we're investing in this week. If you're already an Investment Club member, CLICK HERE to access it now. Not a member yet? CLICK HERE to join and get full access to all the stocks and options we’re buying and selling every day, plus unlock 40% off with our exclusive discount code.

-

INSIDER TRADES FROM THE WEEK:

1. Joby Aviation (JOBY) - Toyota, 10% owner of the company, bought ~$250 million of JOBY stock on May 22, 2025, but it was reported to the public on May 27, 2025. (Source)

2. Lionsgate Studios (LION) - Liberty 77 Capital, a 10% owner of the company, bought ~$48 million of Lionsgate Studios stock between May 28-29, 2025, but it was reported most recently to the public on May 30, 2025. (Source)

3. Codexis Inc (CDXS) - Opaleye Management Inc., a 10% owner of the company, bought ~$5 million worth of Codexis stock on May 23-28, 2025, and it was reported to the public on May 28, 2025. (Source)

INFOGRAPHICS FOR THE WEEK:

CONTACT US: [email protected]

Responses