TOP NEWS AFFECTING THE STOCK MARKET THIS WEEK:

The 25 Year Old Who Turned $250 Million Into $14 Billion Just Bought A New Stock, and It's His Biggest Position He's Ever Owned!!! (Source)

Stocks mentioned: $INTC, $BE, $SNDK, $IREN, $CRWV, $HUT, $CORZ, $NBIS, $NVDA, $META, $MSFT

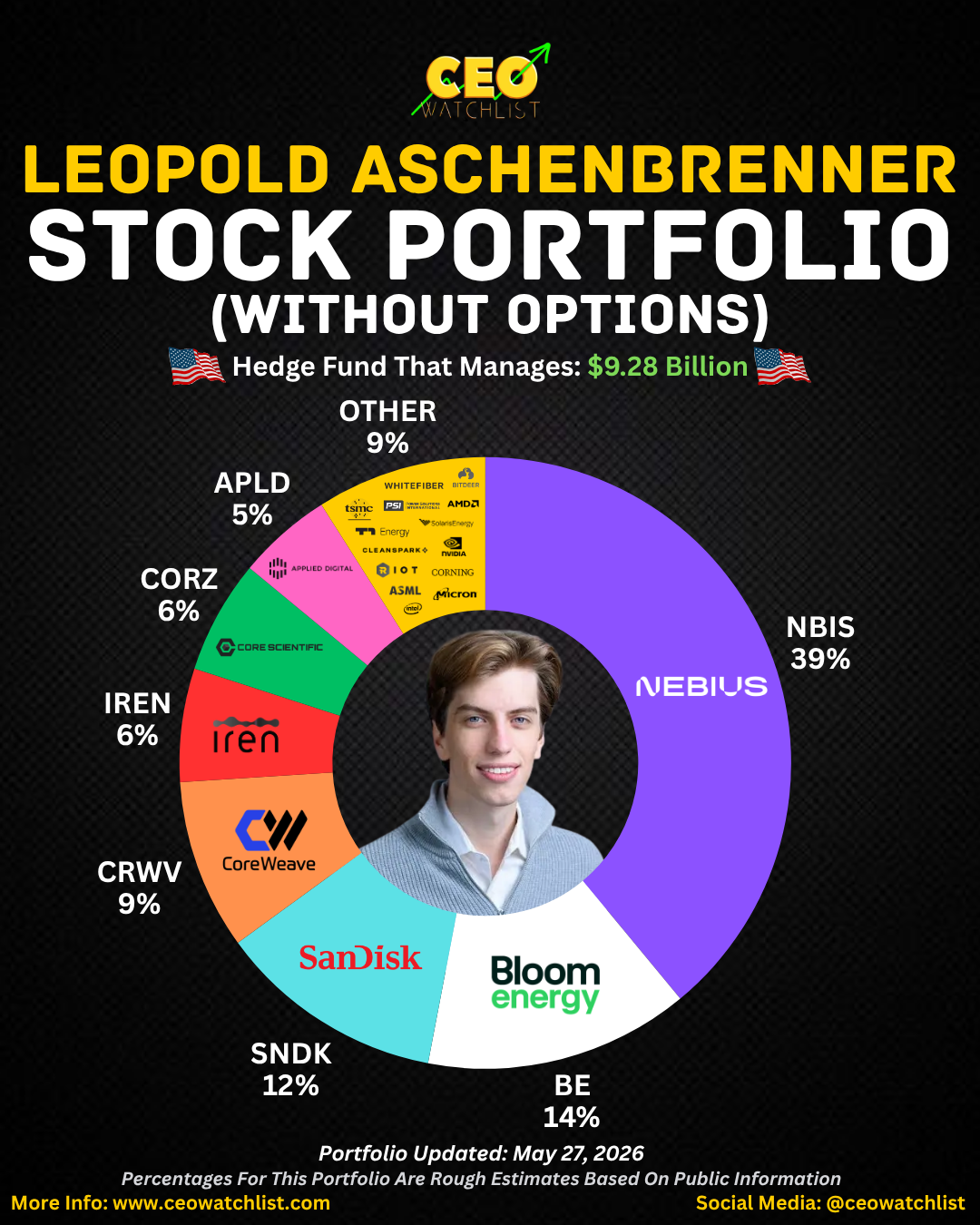

If you've been anywhere near finance social media in the last 12 months, you've probably heard the name Leopold Aschenbrenner. For those who haven't, here's the short version: he's a 25-year-old former OpenAI researcher who, after getting fired in 2024, published a 165-page essay arguing that superintelligent AI could arrive as soon as 2027. Then he did something even more interesting, he put his money exactly where his mouth was. He launched a hedge fund called "Situational Awareness LP" with about $250 million in starting capital, and that fund has since grown to $13.7 billion in assets under management in under two years. That's not a typo. From $250 million to nearly $14 billion. The returns on some of his individual positions have been nothing short of incredible. Intel (INTC) is up 190% year-to-date, Bloom Energy (BE) is up 180%, and SanDisk (SNDK) has surged over 500%. That track record is why, when Leopold moves, people pay attention. His fund has become one of the most closely watched in the world right now, and for good reason: the guy has a thesis, he sticks to it, and it keeps working.

So here's why this week matters. For a while now, the neocloud trade, think companies like IREN Limited (IREN), CoreWeave (CRWV), Hut8 (HUT), and Core Scientific (CORZ), basically the picks-and-shovels players building the physical infrastructure the AI boom runs on, has been well-mapped by Aschenbrenner watchers. His portfolio has included concentrated positions in these names among others, but one name was always conspicuously missing from his filings: Nebius (NBIS). And that bothered us, because in our view, Nebius is the best neocloud name out there; cleaner balance sheet, better partnerships, more institutional backing, purpose-built for AI from the ground up. We kept wondering why Leopold wasn't in it. Turns out, he was. He just wasn't telling anyone yet, and there's a very specific legal reason for that.

Here's the mechanism worth understanding, because this is where it gets interesting. Under SEC rules, when an investor acquires more than 5% of a public company with passive intent (meaning they're not trying to take control of the company), they're required to file what's called a Schedule 13G, which is a shorter, less invasive disclosure than the standard Schedule 13D, reserved for investors who are not acquiring shares with the intent to influence or control the issuer. The key wrinkle is the timing: for passive investors, the filing is due within five business days of crossing that 5% threshold, not before, and not during the accumulation process. That means an investor can quietly build a position for weeks or even months below that 5% line and owe the public absolutely nothing. No disclosure required. Hidden in plain sight. That appears to be exactly what happened here.

Whether Leopold was methodically building this stake over time or acquired a large block all at once, the moment he crossed 5%, the clock started, and the filing hit. According to the Schedule 13G, Situational Awareness now owns 12.41 million shares, representing a 5.6% stake in Nebius. That makes his fund the largest single shareholder in the entire company. Not 5.6% of his portfolio. 5.6% of Nebius itself, as a business. This is a very different and much more significant statement. When you strip out his options exposure and look purely at his stock holdings, this Nebius position represents roughly 39% of his entire stock portfolio. By a wide margin, this is the single largest stock purchase he has ever made.

Now, for those who aren't as familiar with Nebius, quick background, because this company deserves more attention than it gets. Nebius is an AI infrastructure provider spun off from Yandex, the once Russian internet giant known as "Russia's Google", and has evolved into a core AI compute platform focused on GPU clusters that support training and running AI models. Think of it like Amazon Web Services, but purpose-built specifically for AI workloads rather than general computing. The company has been stacking up enterprise partnerships at a pace that's hard to ignore. Nebius secured a $27 billion computing supply deal with Meta and a $2 billion strategic investment from Nvidia (NVDA). That NVIDIA piece specifically matters, Jensen Huang doesn't write $2 billion checks to companies he doesn't believe in. In September 2025, Nebius and Microsoft signed a multiyear AI infrastructure agreement worth $17 billion in expected revenue. That's Meta (META), NVIDIA, and Microsoft (MSFT) all in the same company's corner.

On the financial side, Nebius reported 684% year-over-year revenue growth in Q1 2026. The bull case is simple: as AI compute demand continues to compound, Nebius is one of the few companies with the infrastructure, the partnerships, and the GPU supply relationships to absorb that demand at scale. It's not speculative. The revenue is already showing up. To be fair, bears will point to the stock's run already being significant, Nebius shares have surged more than 151% in 2026 alone, and question whether the valuation has gotten ahead of itself. That's a reasonable pushback. But when a company is growing revenue nearly 700% year over year with hyperscaler-level partnerships, the traditional valuation frameworks start to look a little less useful.

Here's the bottom line; Leopold Aschenbrenner has been right about AI infrastructure before most people understood why it mattered. He started with $250 million, has turned it into nearly $14 billion, and the stocks he's publicly announced have moved dramatically after disclosure. And now, quietly, without telling anyone, he built what is by far his largest single stock position in the one neocloud name we've always thought was the most underappreciated of the group. As Aschenbrenner himself put it: "The AI power needs bet has become the dominant macro theme in technology. Companies controlling compute capacity will capture enormous value during the race to AGI." He didn't say that abstractly. He said it while sitting on a $2.6 billion stake in Nebius. Social media is just beginning to pick this up, and we think once the broader retail audience processes what a 5.6% ownership stake at 39% portfolio weight actually means coming from this particular investor, the reaction in the stock could be substantial. We think Nebius is a name that should be trading at $300 a share without much of a stretch. The filing was public. The position was enormous. And the one person in markets with perhaps the deepest conviction on AI infrastructure just told you, through his actions, exactly what he thinks the best play is.

Earnings Season: 1 Big Winner From Last Week and 3 Big Winners For This Week... (Source)

Stocks mentioned: $DELL, $PANW, $AVGO, $PL

Every earnings season has that one report that stops you in your tracks. This week, it was Dell (DELL). While most companies were out here managing expectations and playing it safe with guidance, Dell walked in and completely blew the roof off. The stock jumped over 30% in a single day, its best day ever, and Wall Street was left scrambling. One analyst at Melius literally said he'd "never seen anything like it." That's not a quote you hear often from people who've been doing this for decades.

So what happened? Dell put up $43.8 billion in revenue for the quarter, up 88% from a year ago. Earnings came in at $4.86 per share when analysts were only expecting $2.94. The gap between expectations and reality was enormous. The reason? AI servers. Dell's AI-optimized server business brought in $16.1 billion this quarter alone, up 757% year over year. To put that in perspective; a year ago, AI servers were a promising side business for Dell. Now they're the whole game. The company booked $24.4 billion in brand new AI orders in a single quarter and raised its full-year AI server revenue target to $60 billion. The CEO put it simply: "The AI opportunity shows no signs of slowing." Hard to argue with that when the numbers look like this.

Here's why this matters beyond just the Dell trade. When a company this big, one that's literally selling the physical hardware that powers AI, posts numbers like these, it tells you something important: AI spending isn't slowing down, it's compounding. That's the backdrop heading into next week, where we're watching three very different names report earnings. Each one tells a different piece of the same story.

Stocks we're watching this week:

- Palo Alto Networks (PANW) - Reports Tuesday, June 2. Palo Alto is the biggest pure-play cybersecurity company out there, and this quarter is going to be an interesting one. Revenue is expected around $2.94 billion, up about 29% year over year. The thing to understand here is that Palo Alto just finished two massive acquisitions back to back, a $25 billion deal for CyberArk and a $3.4 billion purchase of Chronosphere. Think of it like a restaurant chain that bought two other restaurant chains simultaneously. The food might be great, but the integration costs are real and they're hitting the bottom line right now. The market is going to want to see that the company can digest these deals while still growing its core business. Their "platformization" strategy, basically convincing big enterprise customers to ditch a bunch of different security vendors and just use Palo Alto for everything, is the long-term thesis, and any update on that momentum will move the stock.

- Broadcom (AVGO) - Reports Wednesday, June 3. This might be the most anticipated report of the week. Broadcom is the company designing custom AI chips for the biggest tech companies in the world, we're talking Google, Meta, and others. These aren't off-the-shelf chips like Nvidia GPUs. These are purpose-built accelerators designed specifically for each customer's AI workload, and that's a serious competitive advantage. The company itself already told you what to expect: $22 billion in revenue and $10.7 billion in AI chip revenue specifically. That AI chip number would be up 140% from a year ago. So the question isn't really "will Broadcom have a good quarter", it's "do they hit or beat that $10.7 billion number?" Broadcom also owns VMware, the enterprise software business they bought in 2023, which is quietly generating high-margin cash that funds everything else. This is a company that's firing on every cylinder right now.

- Planet Labs (PL) - Reports Thursday, June 4. This one is a little different; smaller, earlier stage, and more speculative. Planet operates the world's largest fleet of Earth-imaging satellites. Every single day, their satellites photograph the entire planet. They sell that data and imagery to governments, militaries, and commercial clients. Revenue is expected around $90 million for the quarter, which would be roughly 37% growth year over year. The defense and intelligence segment is what's really driving the business, governments are paying premium prices for real-time satellite data in a world that's gotten a lot more geopolitically tense. Planet also just launched three new high-resolution "Pelican" satellites via SpaceX in May, which expands their imaging capability. The company is guiding for $415–$440 million in full-year revenue, a big step up from the $308 million they did last year. They're not yet consistently profitable, but free cash flow just turned positive and the backlog grew 79% to over $900 million. This is a higher-risk name, but if you believe the world is moving toward a real-time intelligence economy, Planet is positioned right in the middle of it.

Step back and look at what this earnings season is actually telling us. AI infrastructure spending has moved from narrative to hard financial reality, and it's showing up across hardware, chips, software, and now even space. Dell proved this week that the companies building the backbone of the AI economy are being rewarded in ways that caught professional analysts completely off guard. Next week, Palo Alto, Broadcom, and Planet Labs each give us a window into a different corner of this ecosystem. Together, they'll either confirm the picture Dell just painted, or complicate it. Either way, earnings season is doing exactly what it's supposed to do: forcing the market to confront what's actually happening. Right now, what's actually happening is that this cycle is moving faster than almost anyone expected.

"Super Investor" Spotlight: Harvard University (Source)

Stocks mentioned: $TSM, $GLD, $MSFT, $GOOG, $UNP, $AMZN, $BKNG, $AVGO, $NVDA, $IBIT

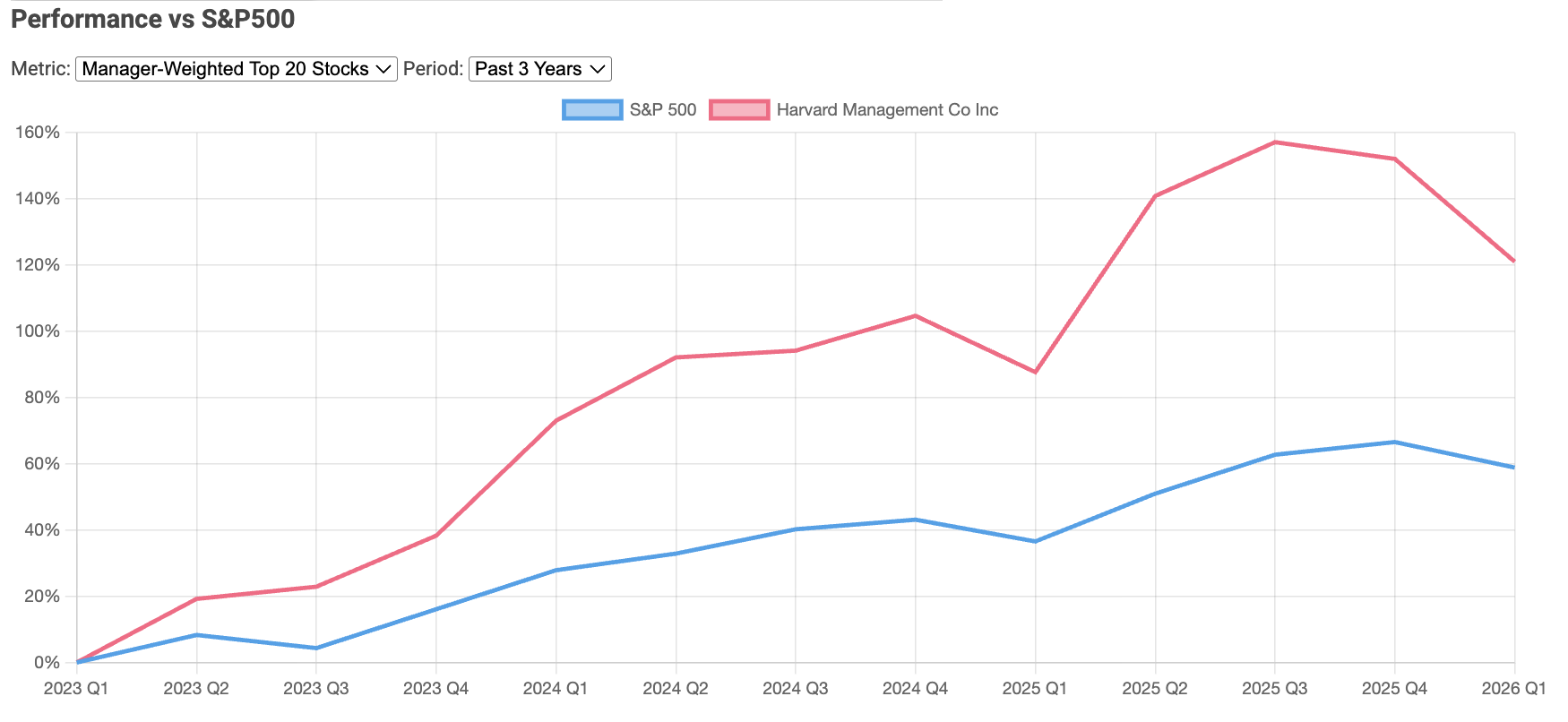

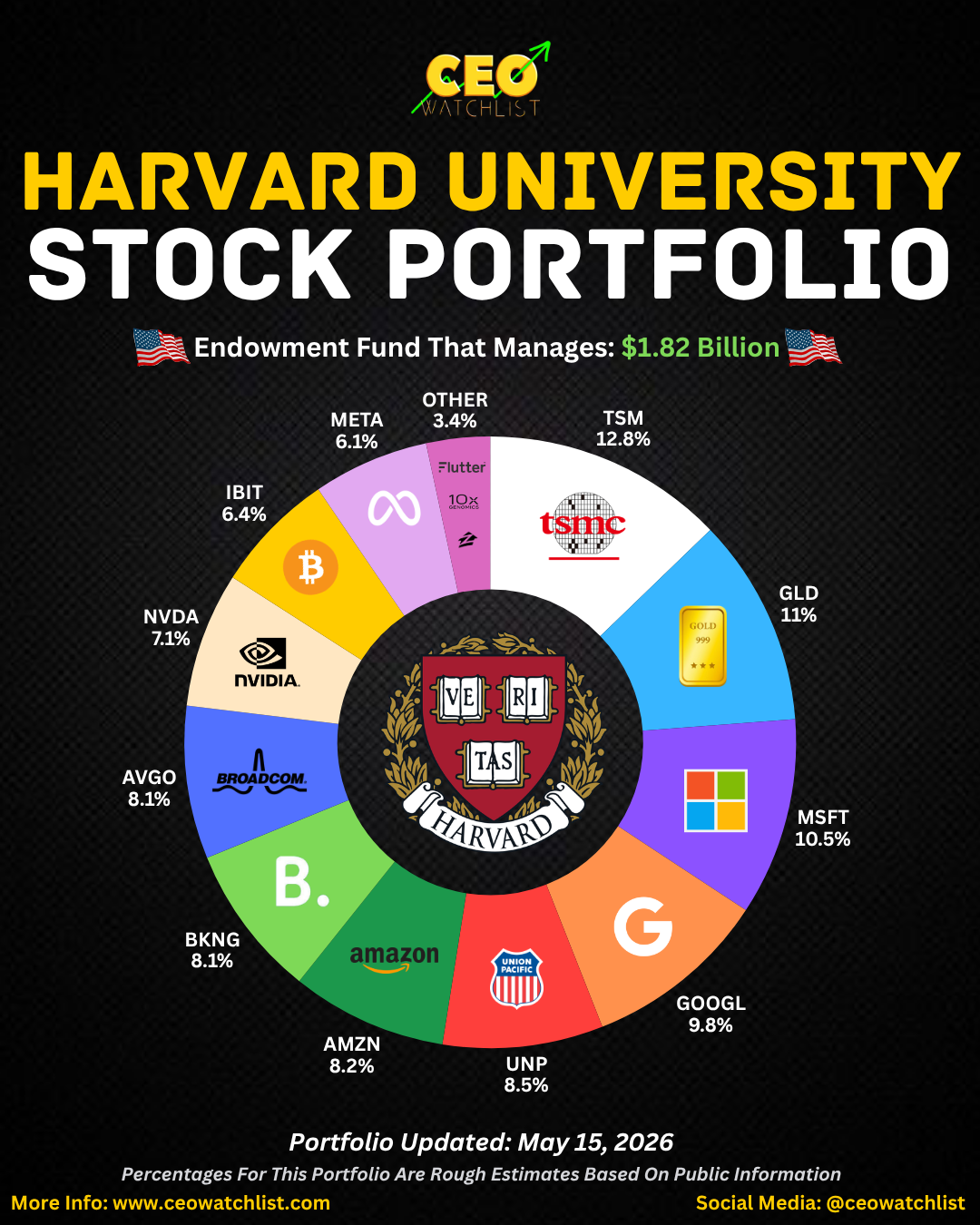

This week’s "Super Investor" Spotlight shines on the Harvard Management Company. For those that don't know, Harvard who is famous for their law school, also has a stock portfolio that they manage investments in. Luckily for us, we are able to track that information to see exactly what they are buying and selling! Managing a massive $1.82 billion stock portfolio, Harvard has built a stellar long-term track record of generating consistent, outsized returns to support academic research and financial aid. Rather than acting as a speculative hedge fund, Harvard operates as a premier long-term wealth compounder, outperforming the overall market, and simply put, making a ton of money!

In its latest strategic reshuffle, Harvard has leaned aggressively into global technology monopolies and hard assets, building a robust, diversified fortress of capital. While critics might argue that an elite university fund should focus more on high-yield bonds or standard indexing, the data reveals a high-conviction bet on digital dominance, global supply chains, and monetary hedges. The fund's allocations span a diverse mix of powerhouse enterprises, showing clear strategic intent to capture upside from artificial intelligence and massive consumer networks, balanced by a meaningful safety net.

Here is a breakdown of the top 10 positions in Harvard's stock portfolio:

- Taiwan Semiconductor Manufacturing Company (TSM) - 12.8%

- SPDR Gold Shares (GLD) - 11%

- Microsoft (MSFT) - 10.5%

- Google (GOOG) - 9.8%

- Union Pacific (UNP) - 8.5%

- Amazon (AMZN) - 8.2%

- Booking Holdings (BKNG) - 8.1%

- Broadcom (AVGO) - 8.1%

- Nvidia (NVDA) - 7.1%

- iShares Bitcoin Trust (IBIT) - 6.4%

Knowing their top positions is one thing, but what good is knowing someone's portfolio if you don't know how well their portfolio has performed? At the end of the day, peformance is what matters, because as investors our goal is to make money. When we look at Harvard's backtested data verses the overall S&P500, we see that their stock picks have massively outperformed the overall market, as can be seen below:

Harvard's blend of high-tech growth stocks and stable assets like gold have given them a clear edge on the overall market. This is why we always pay attention to any changes they are making in their portfolio, as they are one of the better performing "Super Investors" to follow. Key changes to take note of include big purchases of large-cap tech names such as Nvidia and TSM, while they also decided to sell massive amounts of crypto, including Bitcoin and Ethereum. Seems like Harvard is taking a bet on big tech and shying away from the more volatile crypto assets. Clearly Harvard is still betting on growth, but they are rotating what growth their captial is in.

In conclusion, we strongly favor the Harvard Management Company portfolio because it represents a brilliant, forward-thinking blueprint for modern asset allocation. By anchoring their capital in dominant tech monopolies like TSM, Nvidia, and Alphabet, while aggressively securing defensive anchors like Gold, they have engineered a resilient portfolio built for the future. Ultimately, Harvard’s strategic blend teaches us that the ultimate investing formula isn't about avoiding risk altogether, it's about balancing high-conviction growth with rock-solid protection.

INSIDER STOCK TRADES FROM THE WEEK:

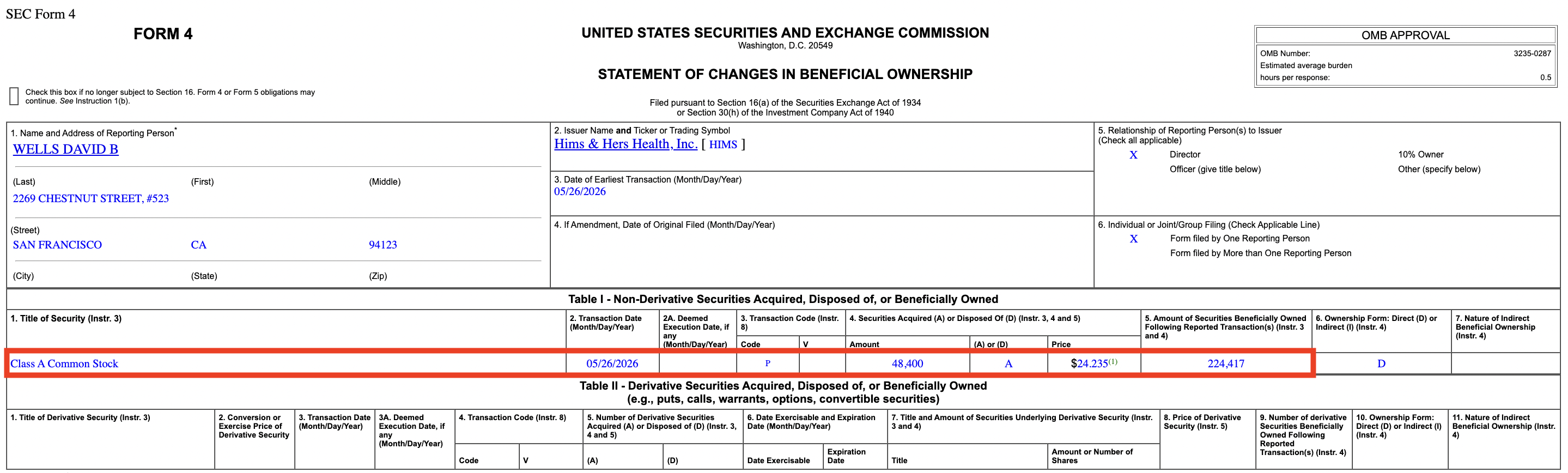

1. Hims & Hers (HIMS) - David Wells (Director, Ex-CEO of Netflix) bought roughly $1,200,000 worth of HIMS at an average price of $24.23/share on May 26, 2026, and it was reported to the public later that same day. (Source)

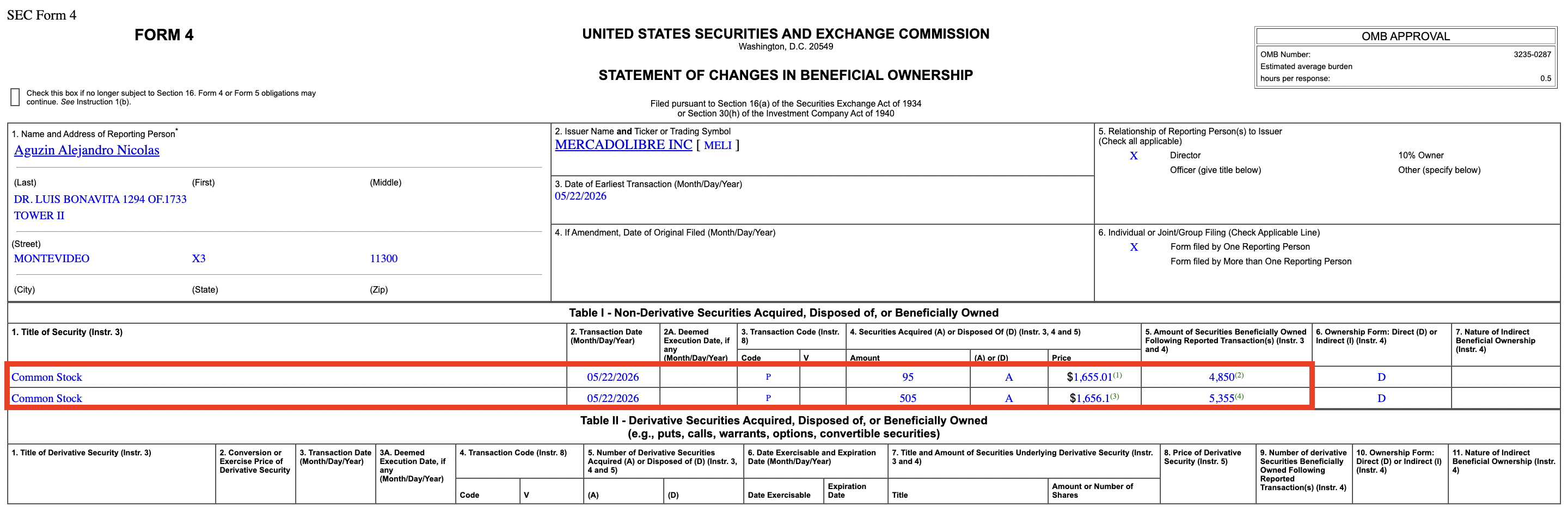

2. MercardoLibre (MELI) - Alejandro Aguzin (Director) bought roughly $1,000,000 of MELI at an average price of $1,655.93/share on May 22, 2026, but it wasn't reported until May 26, 2026. (Source)

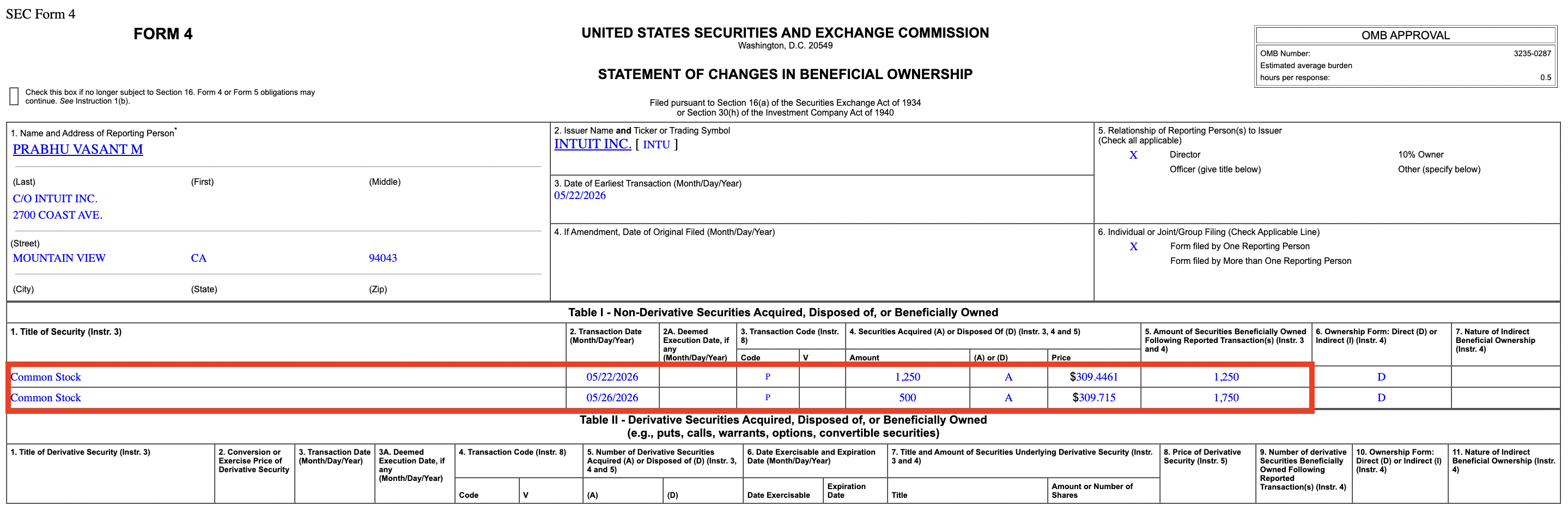

3. Intuit (INTU) - Vasant Prabhu (Director, Ex-CFO of Visa) bought roughly $500,000 of INTU at an average price of $309.52/share between May 22-26, 2026, and it was most recently reported to the public on May 26, 2026. (Source)

Over 2,000 people have already signed up for my FREE Masterclass video on how to unlock my exact strategies for finding winning stock/options trades! I'll share everything including how to find what Politicians and CEOs are buying. Don’t miss your chance to get in for FREE before spots fill up!

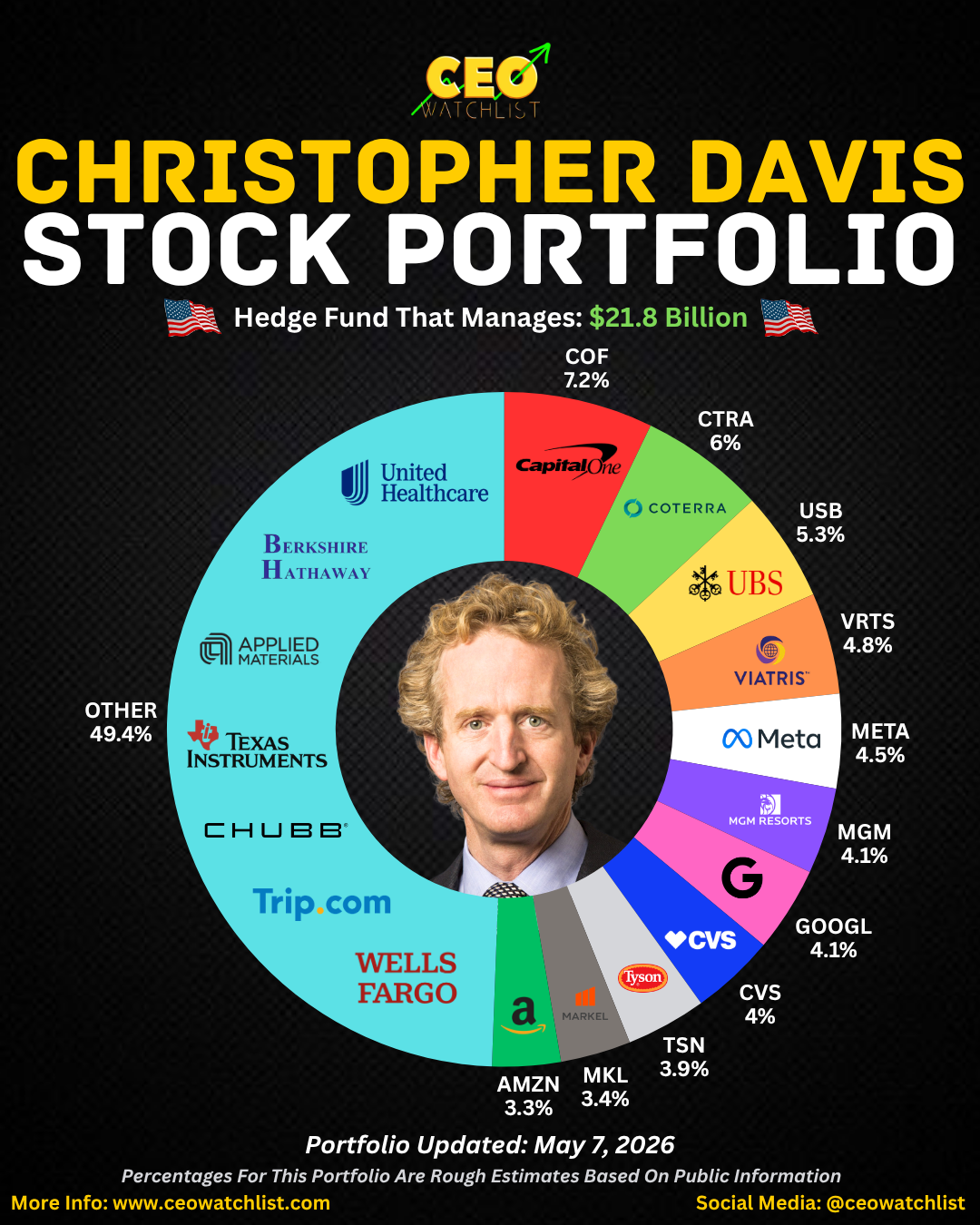

INFOGRAPHICS FOR THE WEEK:

CONTACT US: [email protected]

Responses