TOP NEWS AFFECTING THE STOCK MARKET THIS WEEK:

-

The Power Limit: Why A.I. Will Crash Without a Nuclear Grid and What Stocks We Need To Pay Attention To! (Source)

Stocks mentioned: $TSM, $CEG, $CCJ, $BWXT, $VRT, $VST

Every AI breakthrough, from LLMs to synthetic agents, is framed as a software triumph. But that framing is now dangerously obsolete. AI is no longer constrained by algorithms, talent, or even silicon. It’s constrained by electricity. Not just any electricity. We’re talking about dense, dispatchable, sovereign-controlled electrons, the kind you don’t get from wind farms in a drought or solar panels at night…we’re talking about nuclear.

The U.S. AI stack is being built on infrastructure that was never designed to support it. And the cracks are already visible. It’s no accident that hyperscalers are panic-buying substations and transformers. Or that Taiwan Semiconductor (TSM) is reconsidering fab placement in Arizona over power concerns. Or that new data center projects now come with 3–5 year delays just for grid interconnection. This is the unpriced risk sitting beneath the entire Fourth Industrial Revolution. And it’s why Trump’s recent nuclear executive order may go down as the most consequential industrial policy decision in decades.

Forget red vs. blue. This is steel vs. silicon. The executive order didn’t just signal support for nuclear, it unlocked a bottleneck that underpins the entire AI industrial base. By accelerating licensing, de-risking supply chains, and fast-tracking modular nuclear deployment, the order reframes nuclear as strategic infrastructure, not an environmental talking point. It is the clearest sign yet that the U.S. government is preparing to treat power as national security because in a world of compute supremacy, it is.

The grid isn’t just strained. It’s misaligned. Today’s generation mix was built for yesterday’s economy. But AI infrastructure demands are compounding faster than renewables can scale and unlike residential demand, compute loads are not elastic. They’re 24/7, high-density, and non-negotiable. The real constraint isn’t land, labor, or even chips. It’s electrons at scale delivered with precision, reliability, and sovereignty.

Enter the new AI Power Stack, where the winners aren’t just software devs or chipmakers, they’re the companies controlling the power rails beneath them:

- Constellation Energy (CEG): Quietly becoming the Amazon Web Services (AWS) of nuclear. With the largest nuclear fleet in the U.S., $CEG is now the critical supplier to every hyperscaler seeking 24/7 carbon-free energy. Unlike wind or solar, Constellation’s assets run hot, stable, and around the clock. In the AI era, uptime is advantage.

- Cameco (CCJ): The $TSM of uranium. Every small modular reactor (SMR) startup, every utility prepping for modular deployment, every Western government seeking to decouple from Russian fuel, they all start here. Cameco doesn’t just mine uranium, it mines optionality. And in a constrained fuel market, that becomes a control point.

- BWX Technologies (BWXT): America’s pre-built nuclear defense contractor. Already delivering micro-reactors to the Department of Defense, with deep vertical integration from fuel to fission. Post-order, they’re not just a defense play they’re a sovereign infrastructure lever. Think of them as Lockheed Martin $LMT for the AI grid.

- Vertiv (VRT): The forgotten backbone of data centers. Their tech sits behind every hyperscale rack whether it’s managing heat, power distribution, or failover inside next-gen data centers. Without Vertiv, the power doesn’t flow. As AI expands into harsher environments and edge deployments, their footprint compounds.

- Vistra (VST): Bridging legacy and future. With fossil assets transitioning into grid-supporting capacity and early bets on battery storage, Vistra is uniquely positioned to stabilize the intermittency gap while nuclear and SMRs come online. They’re not just a utility, they’re a flex operator for an unstable grid.

We are witnessing the early phase of a power stack repricing. Just as cloud built new rails for software distribution, just as semiconductors redefined national strategy, power is now the substrate of AI leverage. And the market is treating it like a side quest.

This is the mispricing. These companies aren’t energy plays, they are critical infrastructure for the post-silicon economy. Software doesn’t scale without hardware. Chips don’t scale without fabs. And fabs don’t scale without power. This is why the next superpowers won’t just dominate code they’ll dominate kilowatts of energy. Nuclear isn’t a “nice-to-have” anymore. It’s the only way to escape the physics trap we’ve built into our digital economy.

The recalibration is underway. Policy is moving. Capital is stirring. And the industrial players sitting on the right side of this shift are still priced like utilities, not infrastructure kings. By the time the rest of the market catches up, the power hierarchy will already be locked in. This isn’t about clean energy. It’s about control. And in the age of intelligence, whoever controls the power… controls the future.

-

The New Age of Defense: 5 Stocks Leading Us Into The Future (Source)

Stocks mentioned: $PLTR, $NET, $CRWD, $RBRK, $AXON

For decades, we’ve treated defense as a an industry of tanks, missiles, and troops. But in a post-industrial world, war no longer announces itself with sirens and gun fire. It slips in through code. The real battlefield is cognitive, invisible, and always-on. While governments scramble to modernize their arsenals, they’re overlooking the core constraint: defense is now a software problem, and the old guard, built for physical war, can’t solve it. A new class of tech-native defense firms is quietly rising to fill the void, not with bombs, but with algorithms, edge networks, and predictive intelligence. We’re not just going to tell you what stocks but we will also explain their potential for changing our present and future.

The war in Ukraine and rising tensions over Taiwan aren’t just geopolitical flashpoints, they’re stress tests for digital sovereignty. Cyberattacks, AI-enabled drone strikes, and real-time battlefield analytics have become standard operating procedures. This isn’t speculative futurism. It’s happening now. In this new paradigm, companies that secure data, predict threats, and enable rapid decision-making aren’t just IT vendors, they’re strategic assets. Investors who understand this shift early stand to benefit from a multi-decade replatforming of the defense-industrial complex.

At the heart of this shift are five companies redefining what modern defense infrastructure looks like:

- Palantir (PLTR) long misunderstood by Wall Street, has become the decision engine for Western militaries and intelligence agencies. Its AI Platform (AIP) is rapidly emerging as the operating system for real-time, sovereign computation.

- Cloudflare (NET) meanwhile, is securing the edge of the internet itself, acting as the programmable gatekeeper against an onslaught of cyberattacks and nation-state probes.

- Crowdstrike (CRWD) with its autonomous Falcon platform, protects enterprise infrastructure at the endpoint level, turning millions of devices into a distributed defense network.

- Rubrik (RBRK) offers zero-trust data recovery, the last line of defense in an age where ransomware can paralyze governments.

- Axon (AXON) is quietly building the digital nervous system for public safety, turning police forces and city agencies into real-time, cloud-connected units of coordinated response.

These aren’t isolated bets on “cybersecurity” or “AI.” Together, they represent a software-first defense stack for the 21st century, one that spans battlefield, boardroom, and city hall. Each solves a different bottleneck: Palantir enables understanding, Cloudflare defends the perimeter, CrowdStrike protects the interior, Rubrik ensures recoverability, and Axon governs trust and coordination on the ground. This is not just innovation, it’s vertical integration of digital defense. And yet, these companies are still priced like growth tech, not sovereign infrastructure. The market has not yet re-rated them for what they are becoming.

This is the underpriced truth: the most important defense contractors of the next decade won’t manufacture weapons, they’ll secure and govern data. The new age of defense is already underway, and it will shape everything from foreign policy to enterprise architecture. As the world fragments and institutions race to harden their digital perimeters, those who own the operating layers of trust, detection, and response will command outsize power and returns, which is why we own all 5 of these stocks. Investors who wait for consensus may be too late. This is not a trend. It’s a regime change. And it’s happening in real time.

-

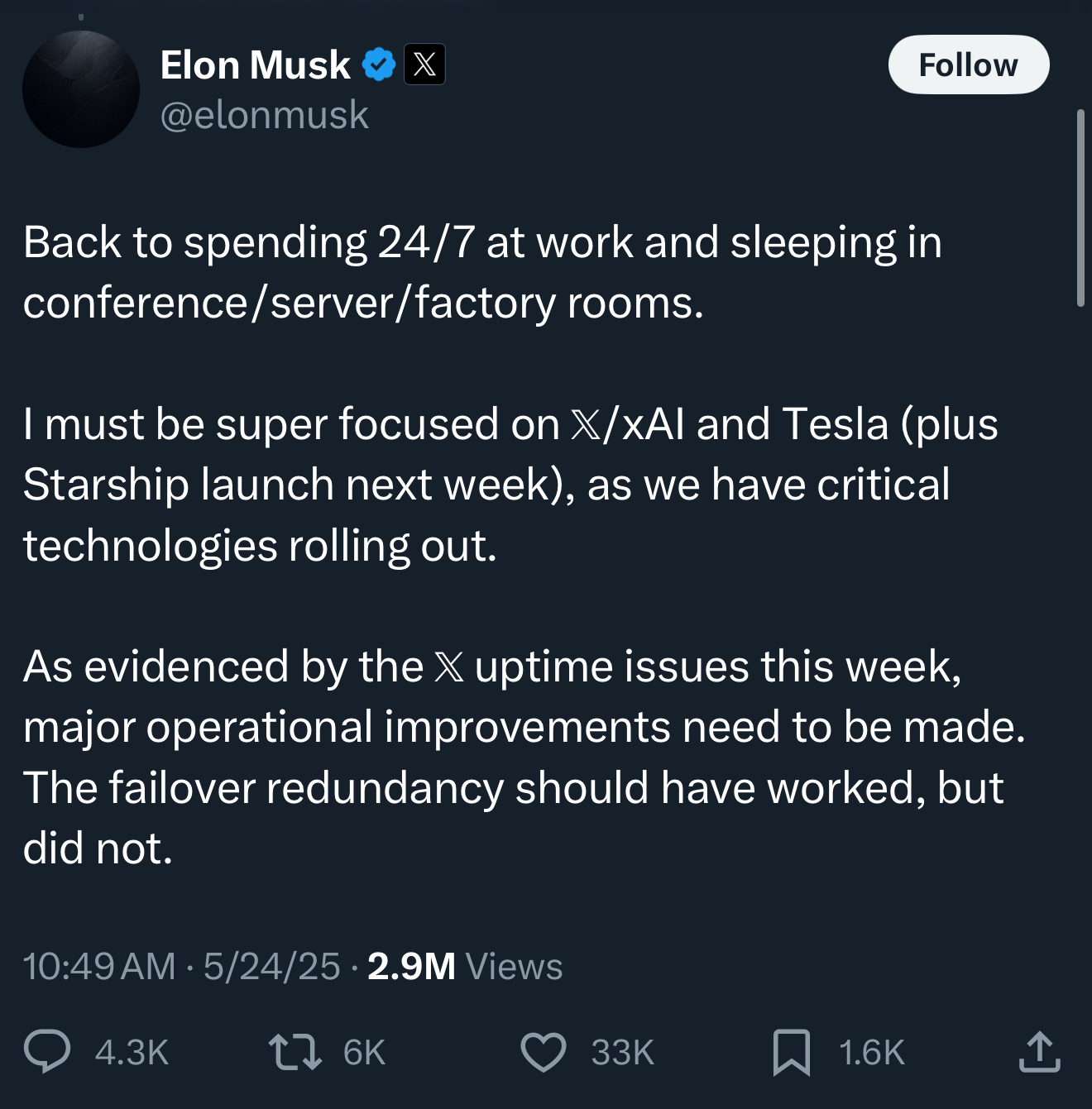

Elon Musk is Back! Is it Time to Reprice Tesla Higher? (Source)

Stocks mentioned: $TSLA, $AMZN, $NVDA, $ON, $ALB, $CGNX

Elon Musk announced on Saturday, he was returning to Tesla (TSLA) full time. Elon coming back as a full-time operator is not just about re-prioritization, it’s a catalyst for a new industrial chapter. Media narratives have framed this as a reactive move, a pivot from distractions politically, but that interpretation, which may hold some truth, misses the deeper signal…Musk is re-engaging with Tesla at the exact moment it is transitioning from a pure-play EV company to a vertically integrated automation platform. The renewed focus is not about crisis management; it’s about execution, particularly on the technologies most investors have yet to properly price…robotics.

We are on the verge of a large-scale industrial transition. The convergence of three forces: re-shoring of advanced manufacturing (bringing manufacturing back to the states), A.I.-native automation (efficiency with using artificial intelligence), and energy decentralization (generating energy away from the main grid). These are reshaping how physical goods are made and moved. Governments are backing these trends with capital such as the U.S. subsidizing domestic battery and semiconductor production like having TSM build new factories here in the states rather than in Taiwan. Within this context, Tesla is positioned not just as an electric vehicle (EV) leader but as a vertically integrated hardware (batteries/EVs/robotics) and software (full self driving (FSD)/robotic software/operating systems) AI company based in the U.S. with a unique robotics asset: Optimus. This humanoid robot initiative, currently in prototype stages, could eventually serve as a modular labor unit for Tesla’s own factories compounding productivity gains internally before expanding into broader industrial markets, similar to what Amazon (AMZN) is doing with their robots in their warehouses.

The core constraint is human labor at scale, especially for repetitive, precision-based physical tasks. Optimus is designed to address that. Tesla has the advantage of an existing industrial environment in which to train, iterate, and deploy these systems rapidly. Musk has called Optimus the most important long-term product Tesla is working on. With his renewed operational focus, there’s now a much higher probability that it accelerates from concept to deployment within the next business cycle.This renewed focus also increases the strategic relevance of ecosystem partners. Nvidia (NVDA), whose GPUs underpin Tesla’s current AI workloads, will likely remain a critical supplier in the near term, even as Tesla expands its own Dojo (Tesla's supercomputer that trains its full self drive systems) compute efforts. ON Semiconductor (ON) supports Tesla’s drive to reduce power loss and improve efficiency in EV and robotics hardware. Albemarle (ALB) remains a key input provider for Tesla’s battery ambitions, which could power not just vehicles, but robotics systems as well. And Cognex (CGNX) which is a leader in machine vision and could become increasingly relevant as Tesla builds out the sensing stack for Optimus at industrial scale.

Tesla is no longer just a car company. It’s increasingly an automation platform with leverage in energy, AI, and labor substitution. Musk’s shift back to full-time engagement is a signal that execution risk is narrowing and timelines are tightening. Investors often struggle to model breakthroughs like Optimus, but that’s precisely where asymmetric upside lives: in the underpriced, high-leverage optionality that most valuation frameworks exclude. That optionality just became more real.

Musk’s return is not just a headline, it’s a hinge point. For years, analysts asked whether Tesla could build the factory of the future. Now the better question is: what if Tesla is the factory of the future? The difference is subtle, but the market reaction won’t be.

Note: This was a post from Elon Musk on Twitter (X) about him coming back to work full time.

INSIDER TRADES FROM THE WEEK:

1. Advanced Micro Devices (AMD) - Philip Guido, EVP & Chief Commercial Officer (CCO), bought ~$1 million of AMD stock on May 20, 2025, but it was reported to the public on May 22, 2025. (Source)

2. Middleby (MIDD) - Edward P. Garden, director, bought ~$93 million of Middleby stock between May 9-21, 2025, but it was reported to the public on May 22, 2025. (Source)

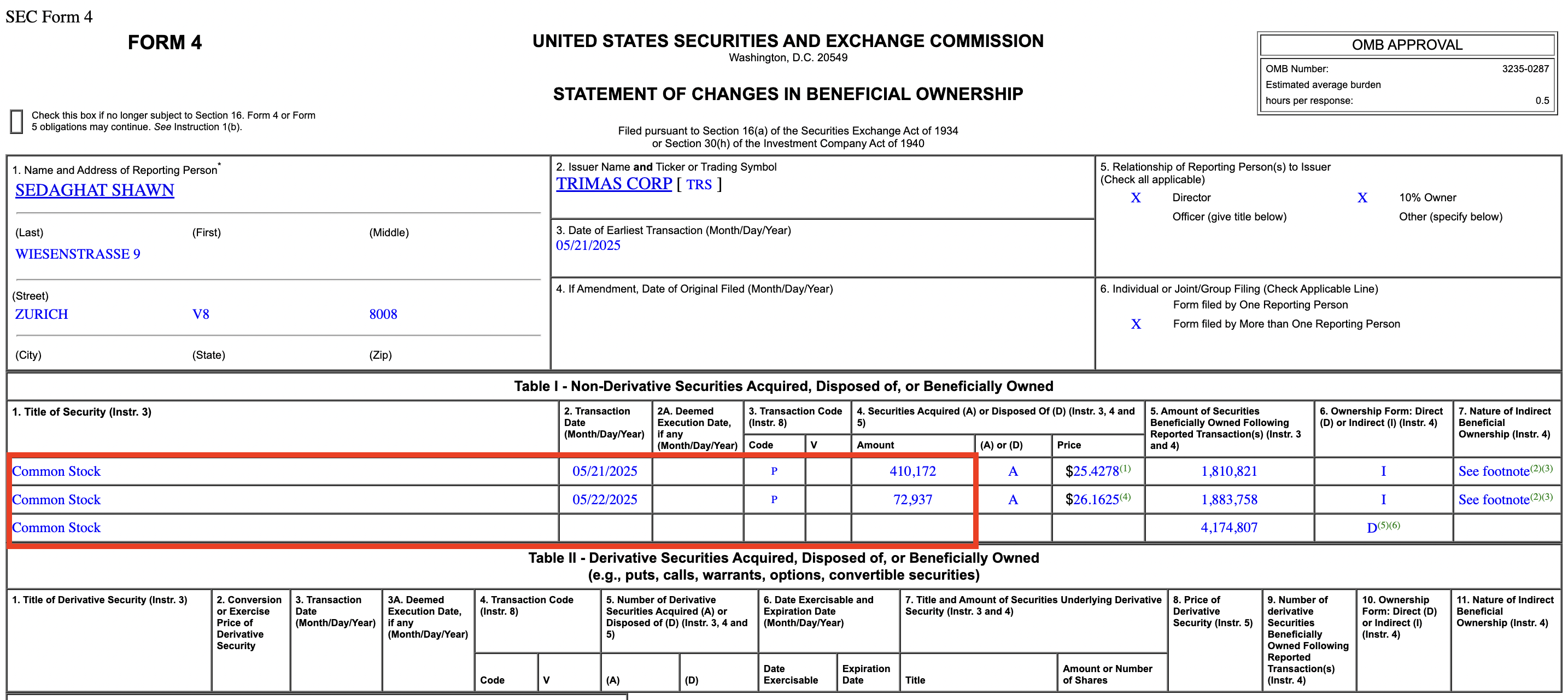

3. Trimas (TRS) - Shawn Sedaghat, director, bought ~$21.5 million worth of Trimas stock between May 19-22, 2025, but it was reported to the public on May 23, 2025. (Source)

INFOGRAPHICS FOR THE WEEK:

CONTACT US: [email protected]

Responses