TOP NEWS AFFECTING THE STOCK MARKET THIS WEEK:

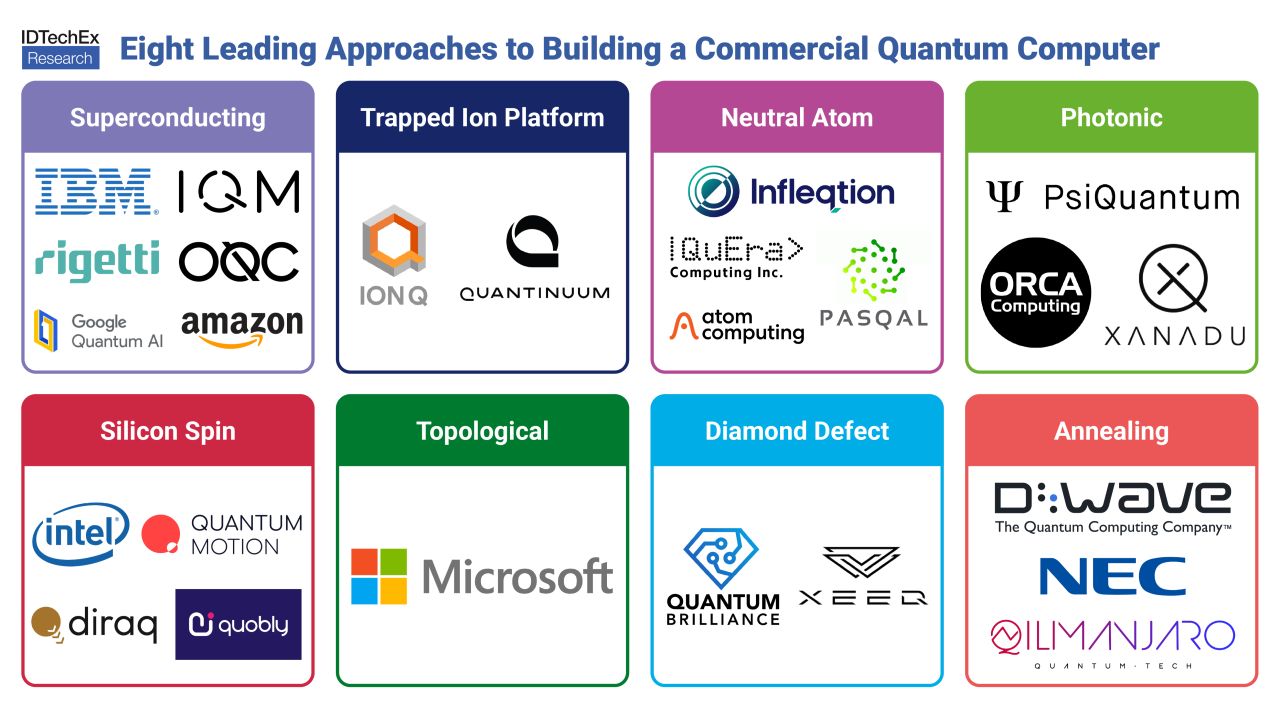

America Just Placed a $2,000,000,000 Bet on Quantum! Here Are The 5 Stocks That Are Direct Beneficiaries... (Source)

Stocks mentioned: $IBM, $GFS, $QBTS, $RGTI, $INFQ

Think of classical computers as extraordinarily fast librarians, they can retrieve and process information at blistering speed, but they still have to check every book on the shelf one at a time. Quantum computers work completely differently. They exploit the properties of subatomic physics to evaluate many possibilities simultaneously, which means certain problems that would take a classical computer millions of years to solve could be cracked in hours. Drug discovery. Unbreakable encryption. Climate modeling. Financial portfolio optimization. The potential applications are so vast that nations are now treating quantum capability the same way they once treated nuclear capability: as a strategic national asset. On May 21, 2026, the United States Department of Commerce made that priority explicit, signing letters of intent to deploy $2.013 billion across nine companies, funded through the CHIPS and Science Act, with the government taking equity stakes in return. This is not a research grant. This is an industrial policy bet.

To understand why this matters, you have to understand the race. China has committed hundreds of billions of dollars to its domestic semiconductor and quantum programs. Europe has its Quantum Flagship initiative. The U.S., for all its private-sector dominance in classical computing, has historically underfunded quantum hardware at the national level. What changed? The realization that quantum computing is not a better computer, it is a different kind of computer, and the nation that builds the foundational hardware and software stack first will control the infrastructure layer of an entirely new computing paradigm. Whichever country manufactures the world's quantum wafers, the chip-like building blocks of quantum machines, will hold a position analogous to where Taiwan Semiconductor (TSM) sits today in classical chips: irreplaceable, strategically critical, and extraordinarily profitable. The Commerce Department just signaled it does not intend to cede that position. Here are the stocks positioned to benefit most:

- International Business Machines (IBM) - IBM is the anchor of this entire program. Its $1 billion grant funds Anderon, described as America's first pure-play quantum chip foundry, and IBM is matching the government dollar-for-dollar with $1 billion of its own capital. Anderon's mandate is to manufacture quantum wafers domestically at scale. If quantum hardware follows the same economic logic as classical chips, whoever builds the foundry infrastructure first builds the moat. IBM has been in quantum since the 1980s and commercialized it as early as 2016. This grant is not validation, it's acceleration.

- GlobalFoundries (GFS) - GlobalFoundries is the only large-scale U.S.-based semiconductor foundry not primarily focused on leading-edge classical chips. That makes it uniquely positioned to pivot manufacturing infrastructure toward quantum-compatible processes. Its $375 million award positions it as the second foundry pillar in the program. Think of GlobalFoundries as the manufacturing backbone, less glamorous than the pure-play quantum names, but potentially the most operationally critical, since quantum chips still need to be fabricated somewhere.

- D-Wave Quantum (QBTS) - D-Wave is the longest-running commercial quantum computing company in the world. Its approach, called quantum annealing, is purpose-built for optimization problems: think supply chain routing, financial scheduling, protein folding. While other firms chase general-purpose gate-based quantum computers, D-Wave has been quietly generating real commercial revenue from customers who need answers to specific, hard optimization problems today. The $100 million grant signals government confidence in annealing as a near-term utility layer, not just a moonshot. Shares jumped 33% on the announcement.

- Rigetti Computing (RGTI) - Rigetti builds gate-based quantum computers using superconducting qubits, the same underlying physics approach as IBM and Google, but as a pure-play startup with a fully integrated chip-to-cloud stack. The company designs its own quantum chips, runs its own fabrication facility, and offers cloud access to its systems. The $100 million award validates Rigetti's manufacturing credibility and gives it the runway to scale qubit count and error correction, the two biggest technical bottlenecks standing between today's noisy quantum machines and practical commercial utility.

- Infleqtion (INFQ) - Infleqtion is one of the newest publicly traded names in the space, having IPO'd in February 2026, and it is a direct $100 million grant recipient. The company operates on a "neutral atom" quantum platform, a distinct architecture from the superconducting approach used by IBM and Rigetti, and one that many researchers believe offers superior scalability and lower error rates at larger qubit counts. Infleqtion's technology spans hardware and software across computing, sensing, and precision timing, with deep ties to defense applications. It holds over $440 million in cash and short-term investments against minimal debt, giving it substantial runway. Shares surged over 21% on the grant announcement.

The investment thesis here operates on two timelines simultaneously. In the near term, government money de-risks these companies' balance sheets. For early-stage hardware businesses burning cash while they scale qubit counts and reduce error rates, a $100 million non-dilutive grant is an enormous stabilizer. It buys time, and in deep technology, time is everything. The company that survives long enough to cross the threshold into fault-tolerant quantum computing, the point where errors are rare enough that the machine reliably produces correct outputs, wins the market. The government just handed several of these companies a meaningful head start in that race. In the longer term, three to five years out, the more consequential prize is the foundry infrastructure. Anderon, IBM's new quantum wafer company, could become the TSM of the quantum era if it executes. That is not a small statement. TSM is a $2 trillion company.

One important counterpoint to acknowledge: quantum computing has been "five to ten years away from practical utility" for roughly three decades. Error rates remain high, qubit coherence times are short, and no quantum computer has yet demonstrated a clear commercial advantage over a classical supercomputer on a real-world business problem. Government grants do not guarantee technical breakthroughs, and several past CHIPS Act recipients in classical semiconductors have struggled to deploy capital efficiently. Investors should size positions to reflect genuine optionality, not certainty of outcome.

The bottom line is straightforward: the U.S. government has now formally treated quantum computing as a national infrastructure priority, deploying capital with the same strategic logic it once used for nuclear, aerospace, and the internet. When a government bets at that scale and with that framing, it does not do so to lose. It restructures talent pipelines, procurement contracts, regulatory environments, and follow-on private investment flows in favor of the sector it is backing. The nine companies named in this program (IBM, Global Foundries, D-Wave, Rigetti, Infleqtion, Atom, Diraq, PsiQuantum, and Quantinuum) and the broader ecosystem around them, just became America's officially designated quantum champions. History suggests that is not a position to bet against.

Nvidia Earnings and 3 Stocks We're Eyeing This Week... (Source)

Stocks mentioned: $NVDA, $MRVL, $CRM, $SNPS

Last Wednesday, Nvidia (NVDA) put the skeptics back in their seats. The company reported Q1 fiscal 2027 revenue of $81.6 billion, a jaw-dropping 85% jump from a year ago, and then guided the following quarter to $91 billion, well ahead of Wall Street's $87 billion estimate. To put that in plain terms: Nvidia is printing money at a pace that has almost no parallel in the history of publicly traded companies, and it just told you the next quarter will be even bigger. Jensen Huang closed the earnings call with a line worth writing down: "Demand has gone parabolic". The reason is simple: Agentic AI has arrived. Agentic AI refers to AI systems that don't just answer questions, they take actions, run workflows, and operate autonomously on your behalf, like having a digital employee who never sleeps. The companies building and running these systems, your Microsofts, Amazons, and Googles, are spending at record levels to make it happen, and that spending has nowhere to go but up. The signal this quarter sent wasn't just about Nvidia. It was a verdict on the entire AI infrastructure trade.

Here's the part that matters most for investors who are paying attention to where the next dollar flows. When hyperscalers (the big cloud and tech giants) increase their capital expenditure on AI infrastructure, that money doesn't stay with just one company. It trickles down through the entire supply chain, the networking chips, the custom silicon, the optical cables, the software that designs all of it. Think of it like a construction boom: when developers pour billions into building skyscrapers, the concrete companies, the steel manufacturers, and the electrical contractors all win too. Nvidia is the foundation, but the building above it has many floors. Jensen Huang also used the earnings call to plant a flag on what he sees as the next massive wave after agentic AI: physical AI, meaning AI embedded in robots and autonomous machines that interact with the real world. He called it plainly, physical AI revenue has already reached $9 billion at Nvidia alone, and he has described this moment as the "ChatGPT moment for robotics." For those of you who have been following our past newsletters, you know that we have been covering the robotics trade quite extensively! Hearing confirmation from the CEO of the most important company in the entire AI ecosystem confirming that robotics is the next big thing, is very reassuring.

Now, eyes forward. This week brings three high-conviction earnings reports that deserve your full attention. Each sits squarely in the AI infrastructure chain, and each will tell us something specific about whether the buildout thesis is holding:

- Marvell Technology (MRVL) - Reports May 27. Marvell is one of the most important companies most people have never heard of. They design custom AI chips, called ASICs, specifically built for the major cloud companies. If Nvidia makes the general-purpose GPU that powers most AI training, Marvell makes the specialized, tailor-made chips that hyperscalers use when they want to go even faster and more efficiently for specific tasks. Think of it as the difference between a Swiss Army knife and a surgeon's scalpel. Marvell already reported record fiscal 2026 revenue of $8.2 billion, up 42% year over year, and guided fiscal 2027 to approximately $15 billion. This week's report will tell us whether that acceleration is continuing and whether the custom silicon wave is just getting started or beginning to plateau. Given Nvidia's blowout and the continued commentary around massive AI capex from every major hyperscaler, the setup looks favorable. Watch the guidance and anything management says about design win momentum.

- Salesforce (CRM) - Reports May 27. Salesforce is the world's largest CRM (customer relationship management) platform, the software that companies use to manage their sales pipelines, customer service operations, and marketing. But this year's story isn't about CRM in the traditional sense. It's about Agentforce, their AI agent product that closed over 29,000 enterprise deals since launch and reached $800 million in annualized recurring revenue, up 169% year over year. CRM has been one of the worst performing mega-cap tech stocks in 2026, down roughly 30% year to date even as the business itself has grown. That disconnect between price and fundamentals is exactly the kind of setup that creates opportunity, assuming the AI monetization story continues to hold. The question on May 27 is simple: are enterprises actually expanding their AI spend with Salesforce, or are the deal counts impressive but the revenue per deal still too small to move the needle? If Agentforce ARR continues to accelerate, the stock could reprice quickly. If not, this is a name that would be on the chopping block.

- Synopsys (SNPS) - Reports May 27. Synopsys is the most under-the-radar name of the three, and arguably the most important for understanding the long-term chip design economy. They make EDA software, which stands for Electronic Design Automation. In plain language, this is the software engineers use to design chips before those chips ever get manufactured. Without EDA tools, there are no chips, period. Every GPU, every custom AI accelerator, every advanced semiconductor running AI inference goes through EDA software first. As AI chips become more complex and the demand for next-generation designs at sub-2 nanometer scales explodes, Synopsys is in a near-monopoly position alongside a single key competitor. They already beat Q1 estimates handsomely, with revenue up 65.6% year over year, and analysts are projecting another clean beat for Q2. The bigger story here is their $35 billion acquisition of Ansys, a simulation software company, which extends their reach from chip design all the way through full systems engineering. If AI capex is the tide, Synopsys is one of the boats that rises no matter which specific chip or platform wins. Let's not forget that on the past earnings call, Nvidia specifically called out Synopsys as one of the most important companies they work with, and are actually personally invested in their stock portfolio for the company.

The picture coming out of this earnings season is increasingly clear: the AI infrastructure buildout is not slowing down, it is widening. The spending that was once concentrated in GPU purchases is now spreading into custom silicon, networking, software tooling, and enterprise applications. What Nvidia confirmed last week is that the capex cycle is structural, not cyclical. The companies placing the biggest bets on AI infrastructure are not pulling back. They are doubling down. That is the single most important macro signal for anyone invested in this theme. For those of us watching the robotics and physical AI space, Jensen Huang's comments this week served as a powerful second confirmation of a trend we've been tracking for months. The software layer of AI is maturing rapidly. The physical layer, robots that perceive, reason, and act in the real world, is now entering its own inflection point. Next week, we'll be watching how the market digests these three reports, looking for any forward guidance that signals continued strength into the second half of the year, and continuing to map out the names best positioned to benefit as physical AI moves from hype to hardware. Stay focused.

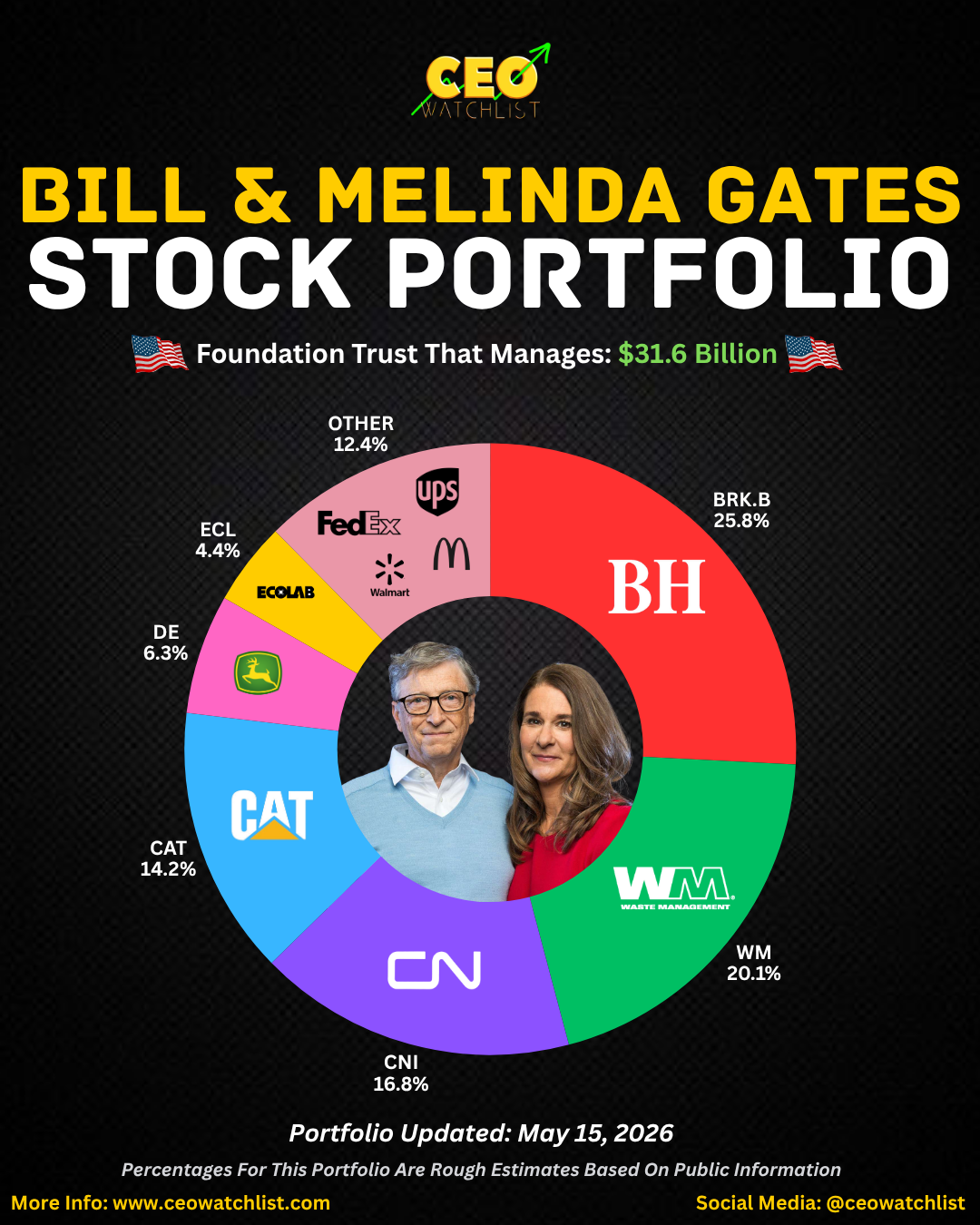

"Super Investor" Spotlight: Bill Gates (Source)

Stocks mentioned: $BRK.B, $WM, $CNI, $CAT, $DE, $ECL, $WMT, $FDX, $KOF, $WCN

This week’s Super Investor Spotlight shines on the Gates Foundation Trust, the absolute financial powerhouse backing the world's largest private philanthropic organization. For newer readers, “Super Investors” are the elite tier of institutional wealth managers who handle billions of dollars, and whose quarterly 13F filings, a mandatory SEC disclosure detailing all publicly traded equity assets, provide a transparent look at where the smart money is moving. Managing a staggering $31.6 billion portfolio, the trust has quietly built an enviable reputation for stellar long-term performance. Unlike typical speculative funds, this vehicle acts as a hyper-stable financial engine, generating predictable, compounded growth to fund global initiatives. Over the years, their highly disciplined allocation strategy has allowed them to preserve multi-billion-dollar capital reserves while navigating complex economic cycles with near-flawless precision.

However, the fund's most recent 13F filing has sent shockwaves through Wall Street due to an absolutely unprecedented strategic move: the trust completely liquidated its remaining position in Microsoft, selling 100% of its shares. This historic divestment marks the absolute end of an era, considering Bill Gates famously founded the tech giant. While the trust did not deploy capital into brand-new companies this quarter, the massive cash inflows generated from that multithreaded $3.2 billion tech exit were systematically reallocated to aggressively scale their highest-conviction holdings.

Here is a full breakdown of the top 10 stock positions that now dominate the Gates Foundation Trust portfolio:

- Berkshire Hathaway Inc. (BRK.B) - 25.8%

- Waste Management, Inc. (WM) - 20.1%

- Canadian National Railway Company (CNI) - 16.8%

- Caterpillar Inc. (CAT) - 14.2%

- Deere & Company (DE) - 6.3%

- Ecolab Inc. (ECL) - 4.4%

- Walmart Inc. (WMT) - 3.3%

- FedEx Corporation (FDX) - 2.7%

- Coca-Cola FEMSA (KOF) - 1.91%

- Waste Connections (WCN) - 1.05%

The fund's latest maneuver serves as a stark reminder that portfolio construction is not just about chasing the flashiest AI trends; it is about aligning your assets with your long-term liquidity needs and risk tolerance. By analyzing their calculated departure from Microsoft and their deep structural commitment to real-world infrastructure, we see an elegant masterclass in financial discipline. Ultimately, the trust has built a fortified, resilient portfolio designed to withstand any economic storm, reminding us all that the most reliable path to financial victory often lies in the world's most essential, enduring businesses.

INSIDER STOCK TRADES FROM THE WEEK:

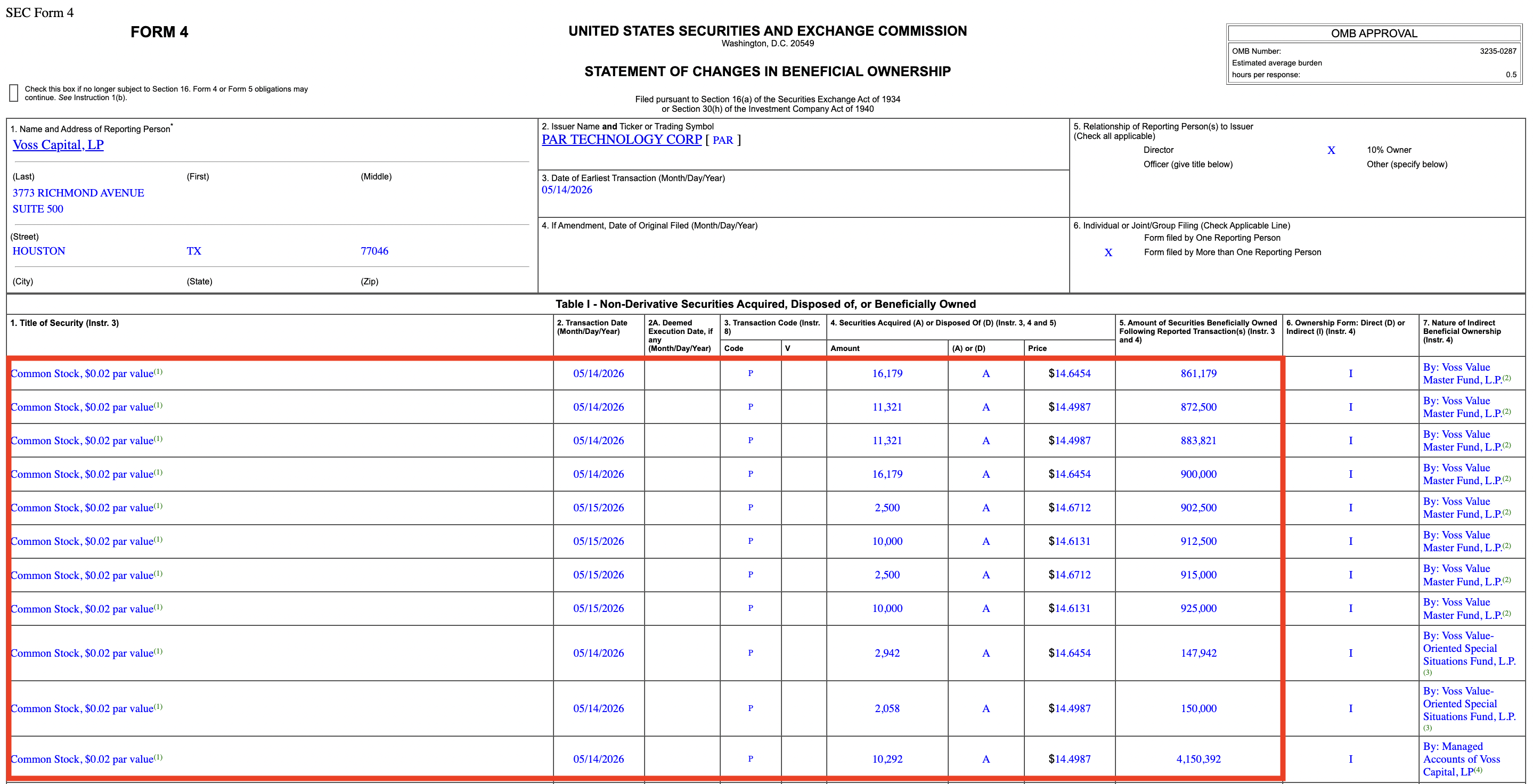

1. Par Technology (PAR) - Voss Capital (hedge fund) bought over $10,000,000 worth of PAR at an average price of $14.59/share between May 14-15, 2026, but it was reported to the public on May 18, 2026. (Source)

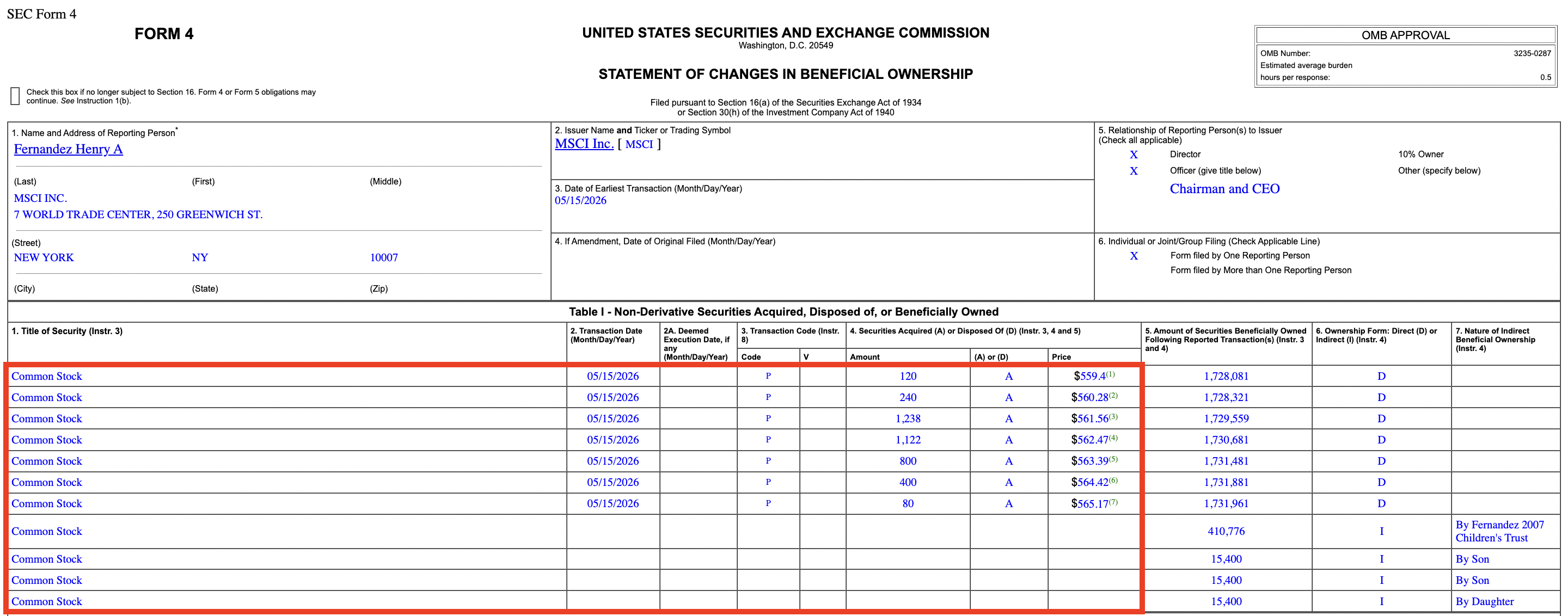

2. MSCI Inc (MSCI) - Henry Fernandez (Chairman & CEO) bought roughly $2,200,000 of MSCI at an average price of $562.40/share on May 15, 2026, but it wasn't reported until May 18, 2026. (Source)

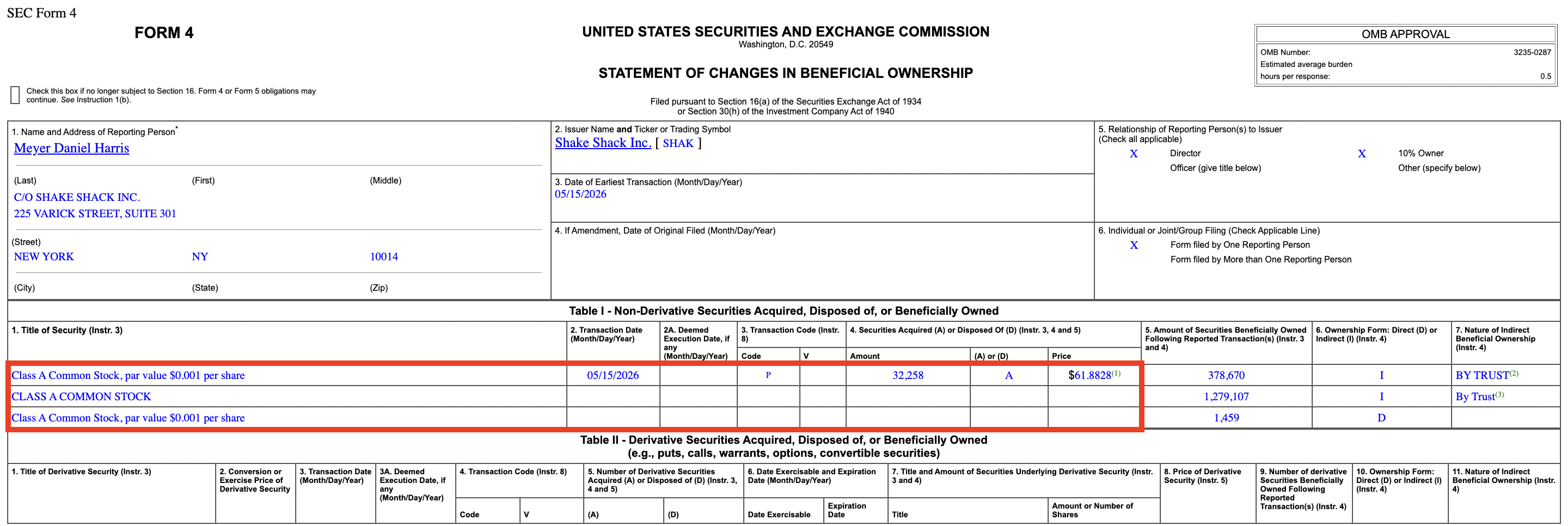

3. Shake Shack (SHAK) - Danny Meyer (director) bought roughly $2,000,000 of SHAK at an average price of $61.88/share on May 15, 2026, but it wasn't reported to the public until May 18, 2026. (Source)

Over 2,000 people have already signed up for my FREE Masterclass video on how to unlock my exact strategies for finding winning stock/options trades! I'll share everything including how to find what Politicians and CEOs are buying. Don’t miss your chance to get in for FREE before spots fill up!

INFOGRAPHICS FOR THE WEEK:

CONTACT US: [email protected]

Responses