TOP NEWS AFFECTING THE STOCK MARKET THIS WEEK:

Nvidia’s CEO Defends Oracle After Markets Panic... And 3 Stocks That Nvidia Likes Today! (Source)

Stocks mentioned: $ORCL, $NVDA, $META, $AMKR, $CRWV, $MSFT

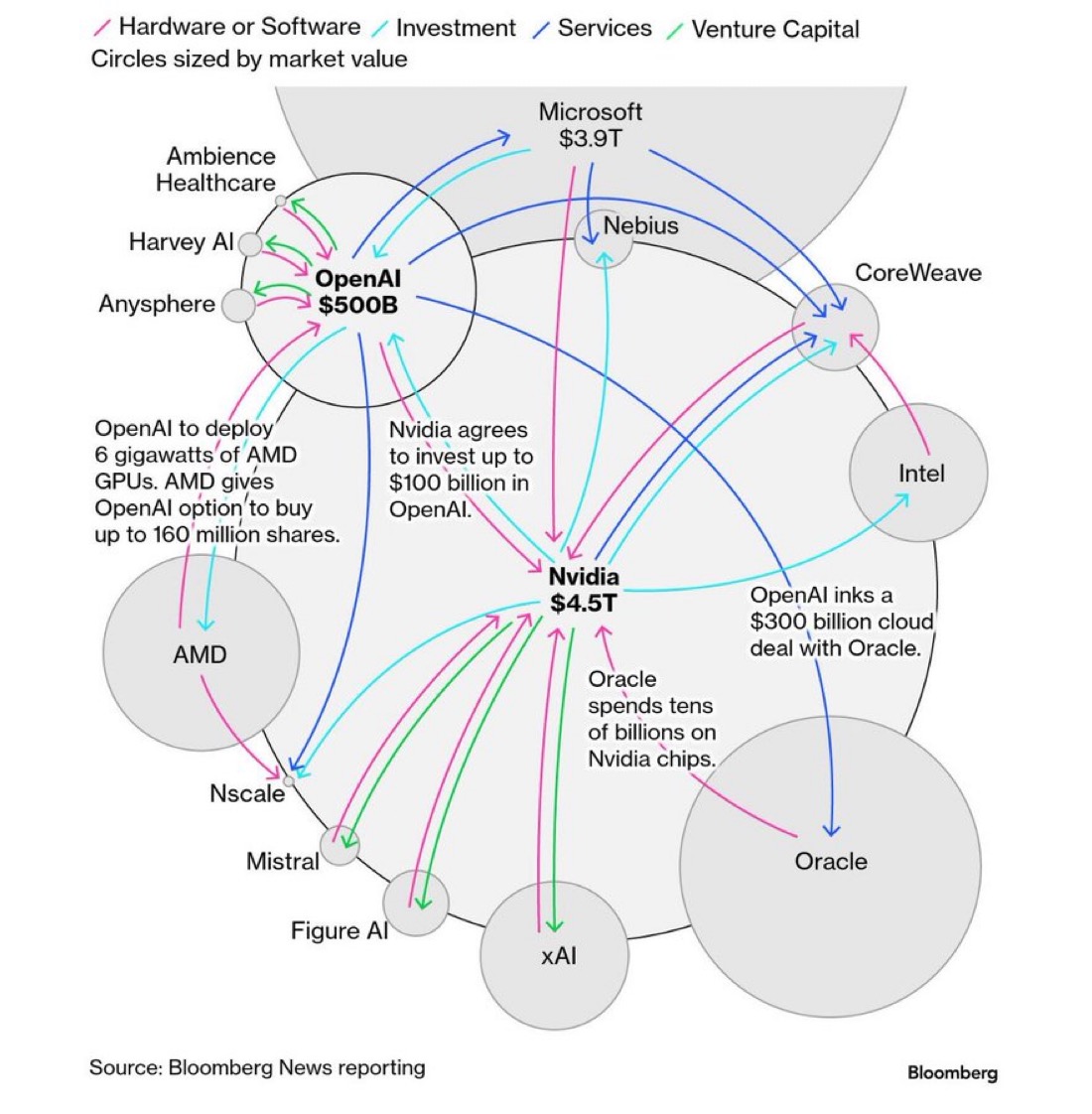

Investors have treated AI infrastructure like a gold rush, assuming whoever sells the shovels will inevitably get rich. But Oracle’s (ORCL) newly leaked internal data shows the opposite. Despite surging demand for GPU rentals, Oracle’s AI cloud margins have collapsed into the low teens, with some deals even losing money. The company made roughly $900 million renting Nvidia (NVDA) powered servers last quarter but kept only $125 million in gross profit, barely 14 cents per dollar of revenue. For a business once known for 70% software margins, this was a rude awakening that sent the stock down as much as 5% in a single day.

At the core of this problem is a structural imbalance between capital intensity and pricing power. Oracle leases most of its data centers instead of owning them, pays full freight for Nvidia’s cutting-edge chips, and must discount heavily to attract large customers like OpenAI (owners of Chat GPT), Meta (META), and Elon Musk's xAI. Power, cooling, and depreciation costs further erode profitability. In contrast, firms that control their own infrastructure or design their own chips can better absorb these costs and defend margins. Oracle’s exposure shows that in the race to supply AI compute, not all capacity is created equal.

Now, to the untrained ear, this all sounds like Oracle is in for a rude awakening, hence the big sell-off in Oracle stock earlier this week. Yet just one day after the report surfaced, Nvidia's CEO Jensen Huang stepped in to calm investors. Speaking with Jim Cramer, Huang said Oracle is “going to do incredibly well,” emphasizing that thin margins are common when ramping up a new technology. He added, “When you first ramp up a new technology, there’s every possibility that you might not make money in the beginning, but over the life of the system, they’ll be wonderfully profitable.” Huang also praised the complexity of Oracle’s operation, calling its data centers “giant supercomputers” that require massive investments in land, power, and cooling. So overall, his comments reframed the issue to show that Oracle’s low margins may reflect a more "early-stage build-out cost" rather than a flawed business model.

For its part, Oracle has highlighted that demand is booming. The company’s backlog of cloud contracts jumped 359% year over year in its fiscal 2026 first quarter, driven largely by a $300 billion compute deal with OpenAI. Oracle has also projected $144 billion in cloud-infrastructure revenue by 2030, up from just over $10 billion in 2025. Even with near-term pressure, the long-term trajectory suggests Oracle could still emerge as a major player in AI infrastructure once economies of scale kick in.

Nvidia is clearly the "hot stock" in the market right now, and all of Wall Street hangs on every word that CEO Jensen Huang says. In recent interviews, he has made some very positive endorsements to 3 key companies that we think have a lot of upside potential. Let's dive in:

- Amkor (AMKR) – “AI has ignited a new industrial revolution — and with it, the chance to reindustrialize America. Amkor’s new Arizona facility is a defining milestone in bringing this capability home. Together, we are rebuilding the supply chain — onshoring the AI technology stack that turns energy into intelligence and secures America’s leadership for the AI century.” - Jensen Huang, CEO and Founder of Nvidia

- Coreweave (CRWV) – "I believe CoreWeave is an outstanding investment," Huang stated this week during an interview with CNBC. He described CoreWeave as a "special" company that is "part of our ecosystem building out the AI infrastructure for the world".

- Microsoft (MSFT) – This week, Huang expressed regret over not investing more in OpenAI, saying, "The only regret we have after investing in OpenAI is that we didn't invest more". Now you may be wondering why this quote is an endorsement for Microsoft, and the reason is because Microsoft owns a significant stake in Open AI. Since Open AI is a private company, the only real way to get exposure through investing is by owning Microsoft stock.

The takeaway is clear: Oracle’s thin margins are not a warning about AI’s future, they are proof that the early stages of technological revolutions are often messy and capital-intensive. Investors should focus on which companies can endure that pain and emerge stronger and according to Jensen Huang, he believes very strongly in the companies leading this AI revolution. Of the 3 we listed, all in one way or another supported by Nvidia, have varying levels of risk. If we wanted to own something a bit safer and less risky, we could invest into Microsoft, but if we wanted to take on a little more risk for more potential upside, a Coreweave or Amkor would fit our portfolio strategy better. Personally we like all 3 of these companies and with the recent China/Trump tariff war escalating, we found some great buying opportunities on Friday. We have just taken new positions in a handful of tech names, in our portfolios, within the Investment Club this past week. If you're an Investment Club Member [CLICK HERE] to login, to see the new stocks we just bought. If you're not an Investment Club Member, as a thanks for being a newsletter subscriber, we are granting you [$200 OFF] the Investment Club when you join today! [CLICK HERE] to take advantage of this exclusive offer. With that said, we'll see you in The Club soon.

AMD Bets Big on OpenAI, and Wall Street Is All In with Price Target Increases, Plus 3 Stocks Poised To Benefit (Source)

Stocks mentioned: $AMD, $NVDA, $ETN $CEG, $AVGO

This past week, Advanced Micro Devices (AMD) 25% surge in a single day wasn’t just another tech rally, it was a statement of survival and ambition in an industry where Nvidia’s dominance has become near-monopolistic. To secure relevance in the AI hardware race, AMD effectively offered OpenAI, the owner of ChatGPT, 10% of its company. That move, although extreme, is a necessity for AMD at this point. It underscores how much competitive power Nvidia has accumulated and how high the barriers to entry have become in the GPU market. The deal positions AMD not just as an alternative supplier, but as a long-term partner in one of the largest AI infrastructure buildouts in history.

The macro-thesis is simple: compute is the new oil, and OpenAI just locked in a second supplier. The partnership calls for 6 gigawatts of AMD GPUs to power OpenAI’s next-generation infrastructure, with an initial 1 gigawatt deployment of AMD's MI450 series beginning in 2026. AMD’s leadership in high-performance computing, combined with OpenAI’s relentless pursuit of scale, creates a flywheel effect (AMD gains credibility and market share, while OpenAI diversifies its dependency away from Nvidia). Even Wall Street analysts couldn't deny how bullish this deal was for AMD, as Jefferies upgraded AMD from $170/share to $300/share. We don't disagree with Wall Street because although giving up 10% of your company is never a great thing, if the expected returns are many multiples of that equity stake you've given up, then a deal like this makes sense. And for a company that was recently valued at $300 billion, they are giving up 10%, which is roughly $30 billion, BUT they are estimating over $100 billion in new revenue in the coming years.

Still, the deal also highlights Nvidia’s unmatched moat. AMD’s willingness to issue OpenAI a warrant for up to 160 million shares, vesting on milestone achievements, effectively transfers future upside in exchange for immediate relevance. This shows that Nvidia’s early investment in CUDA software, developer ecosystems, and production partnerships was not just smart, it was decisive. Critics might argue that AMD’s margin dilution and delayed deployments until 2026 leave room for Nvidia (NVDA) to maintain dominance. Yet, the market is clearly pricing in the long-term upside of AMD taking market share away from Nvidia as this partnership with OpenAI develops.

With AMD willing to give up 10% of their company for a chance to take some market share away from Nvidia, this clearly shows that we are still in the early innings for AI and data centers. Being in the early innings of an AI renaissance, there is still a lot of capital to be deployed in this market. That is why we want to look at stocks that will be beneficiaries of the trickle-down affect of capital flows. Here are 3 stocks that are positioned to benefit:

- Eaton (ETN) – The silent beneficiary behind OpenAI’s and AMD’s massive infrastructure expansion, providing critical power management systems to support next-gen data centers.

- Constellation Energy (CEG) – As the backbone of power supply for data centers, CEG stands to benefit as energy demand for AI compute surges to unprecedented levels.

- Broadcom (AVGO) – Positioned as another high-performance chip supplier for AI infrastructure, offering diversification beyond GPUs into networking and custom accelerators. For hyperscalers like Amazon and Google, making their own custom chips is going to be more cost effective in a lot of cases, rather than buying chips from AMD/Nvidia. This is where Broadcom comes in, and fills that need for these big tech companies.

Our thoughts are simple: despite giving up such a large stake of their company, we believe AMD's deal with OpenAI is a net positive for the stock. When looking at the market cap difference between AMD and Nvidia, it's massive. AMD, who has a market cap of roughly $380 billion, compare it to Nvidia, who has a market cap of close to $5 trillion, if AMD can even grab a small fraction of the market share away from Nvidia, we are looking at the next trillion dollar stock in the market. In sum, this deal signals an inflection point for AMD. It's giving AMD a fighting chance against a true giant in the space, a modern-day David and Goliath moment. Question now is, does this end like the story books? Or will the underdog fail and remain in the shadows of the giant? In our view, we're betting on the prior, that AMD can become a trillion dollar company over the next few years.

"Super Investor" Spotlight: Christopher Davis (Source)

Stocks mentioned: $COF, $META, $AMAT, $USB, $MGM, $CVS, $BRK.A, $MKL, $AMZN, $WFC

On this week’s edition of "Super Investor" Spotlight, we’re looking at Christopher Davis, the third-generation money manager behind Davis Selected Advisors. Davis has produced steady, market-beating results by focusing on high-quality businesses trading below intrinsic value aka he is a value investor. His firm now manages billions across several flagship funds, and his latest SEC 13F filing gives us a clear view of what a modern value investor is betting on in today’s shifting market.

Now, for those that don't know, or if you're new here to the newsletter, a “Super Investor” is someone whose track record and decision-making are so consistent that their portfolio becomes a guidepost for others. By looking through his quarterly 13F filings, we get a rare glance inside the playbook of one of the most successful value investors. What’s immediately clear from Davis’s latest report is that he doesn’t chase trends, he builds durable conviction across finance, healthcare, and technology, sectors he believes can weather both inflationary pressures and a changing interest-rate environment.

Davis' portfolio has over 100 stocks, of which a majority are extremely small position sizings. Because of this, we tend to only look at his higher weighted positions. Obviously, when someone puts more weighting into a particular stock, it tends to reflect their conviction in the name. Here’s a breakdown of his Top 10 holdings:

- Capital One Financial (COF) – 10.2%

- Meta Platforms (META) – 8.3%

- Applied Materials (AMAT) – 4.8%

- U.S. Bancorp (USB) – 4.7%

- MGM Resorts (MGM) – 4.4%

- CVS Health (CVS) – 4.3%

- Berkshire Hathaway (BRK.A) – 4.2%

- Markel Corporation (MKL) – 4.0%

- Amazon (AMZN) – 3.8%

- Wells Fargo (WFC) – 3.5%

When we examine Davis’s portfolio composition, one theme stands out, he isn’t afraid to be overweight in financials. With tech having dominated the headlines all year, investors have been speculating on a tech bubble brewing. Because of fears of a bubble, many investors are looking for alternatives to tech. If you're one of those people, Chris Davis might be the guy that you look towards. With his strong track record and diversified value approach to investing, a portfolio like Davis' is more durable to withstand a market pullback.

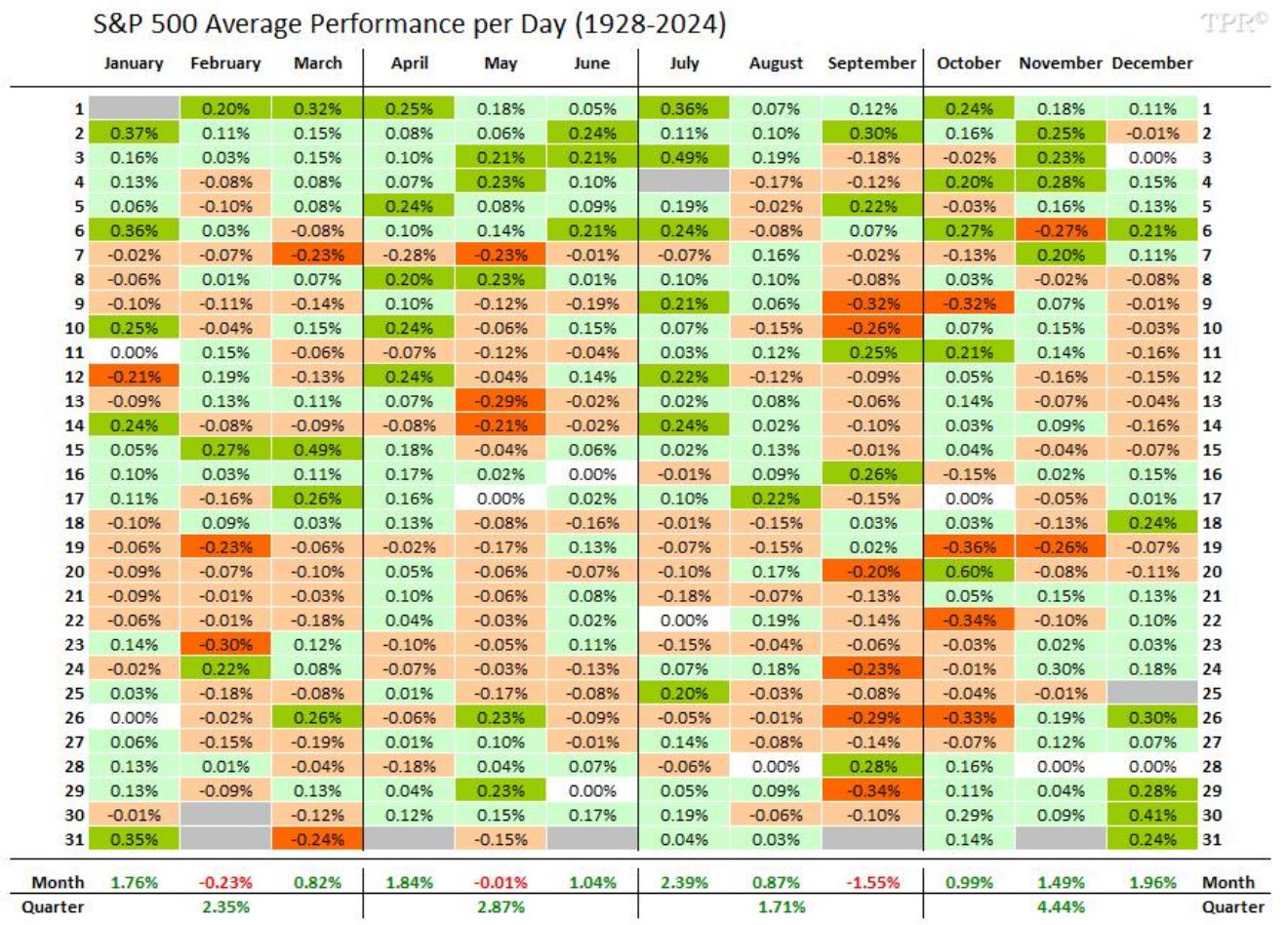

The takeaway for retail investors is straightforward: if you think we are in a tech bubble, now may be the time to start raising capital and rotating into more value oriented plays like what Chris Davis is doing. For us at CEO Watchlist, we have shared our research on seasonality data many times with our Investment Club Members. As you'll see below, historically, October tends to show some weakness:

This is why we raised some capital coming into the month of October, which was good timing, seeing as we just had a massive sell-off on Friday. But, we can't ignore the fact that in Q4, specifically November and December, that the seasonality data turns extremely positive. We don't personally believe that now is the time to rotate into value, but rather, sometime in the first half of 2026. Currently the momentum for growth stocks is to the upside, despite Friday's massive sell-off. We're not ones to fight the trend, which is why we are looking to deploy our cash, on the sidelines, heavily into the end of this month. With all the exuberance in the market as of late, we remain cautiously bullish on growth and nuetral on value.

INSIDER STOCK TRADES FROM THE WEEK:

1. BGC Group, Inc. (BGC) - Cantor Fitzgerald, director of BGC, bought ~$82,000,000 of BGC stock on Oct. 6, 2025, and it was reported later that same day. (Source)

2. Global Water Resources, Inc. (GWRS) - Jonathan Levine, director, acquired $7,500,000 of GWRS on Sep. 30, 2025, but it wasn't reported to the public until Oct. 7, 2025 (Source)

3. ASA Gold & Precious Metals (ASA) - Saba Capital Management, hedge fund and 10% owner of ASA, bought ~$2,100,000 of ASA stock on Oct. 7, 2025, but it was most recently reported to the public on Oct. 8, 2025. (Source)

Over 2,000 people have already signed up for my FREE Masterclass video on how to unlock my exact strategies for finding winning stock/options trades! I'll share everything including how to find what Politicians and CEOs are buying. Don’t miss your chance to get in for FREE before spots fill up!

INFOGRAPHICS FOR THE WEEK:

CONTACT US: [email protected]

Responses