TOP NEWS AFFECTING THE STOCK MARKET THIS WEEK:

The Top Stock Themes For 2026 and 1 Stock In Each That Can 3-5x From Here! (Source)

Stocks mentioned: $AMZN, $MSFT, $RKLB, $ASTS, $RCAT, $PL, $OUST

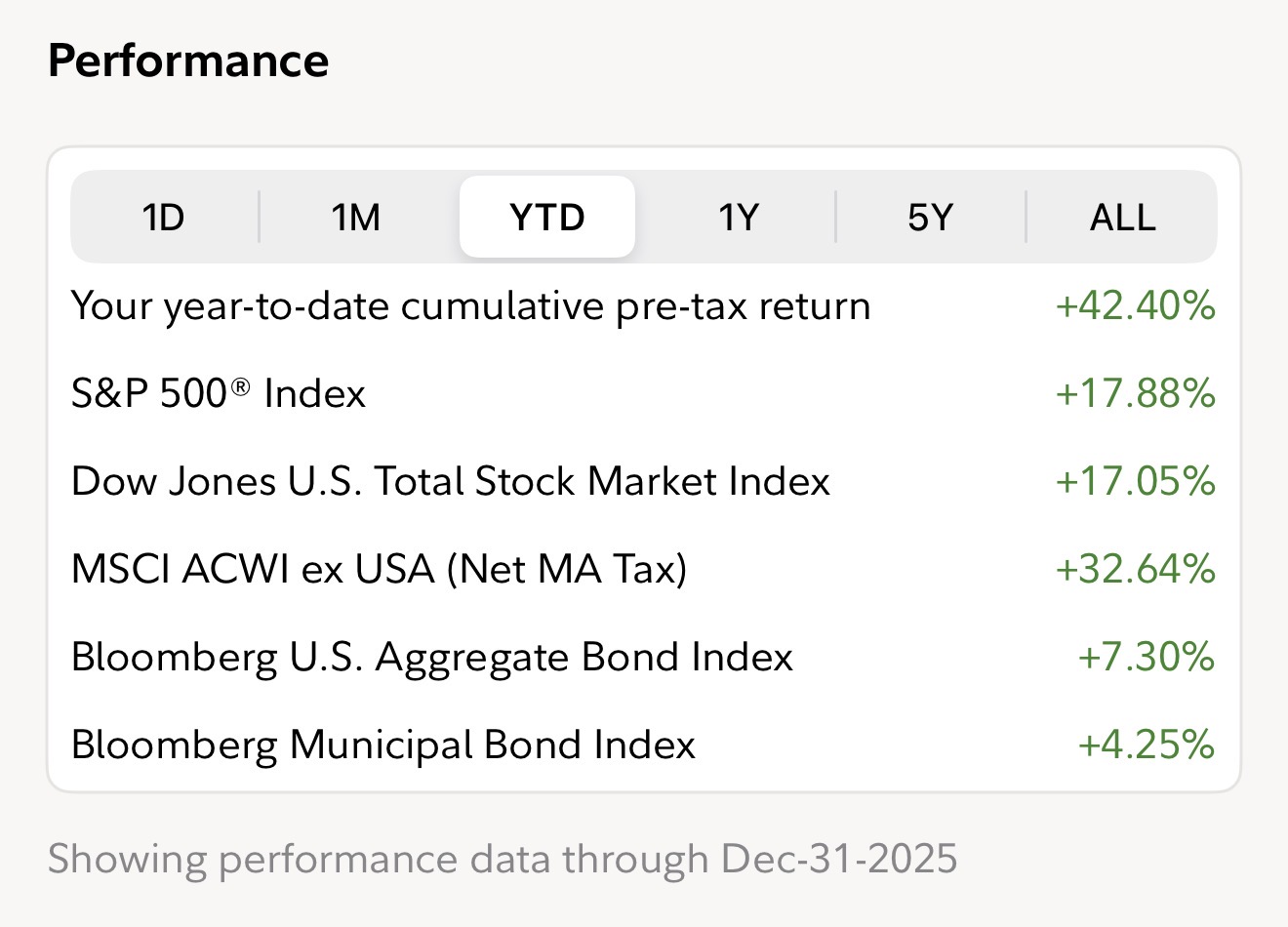

2025 reminded investors of a simple truth that often gets lost in the noise: markets reward discipline, not dogma. Last year was very strong for stocks, with the S&P 500 delivering solid gains, but our goal each year is to significantly outperform the S&P500. We were able to achieve that again this year by more than double what the S&P500 returned. The S&P500 did 17.88% in 2025, while we were able to achieve 42.4% returns during the same timeframe. That is an outperformance of 137%:

This isn't to brag but rather teach you the importance of knowing how to rotate decisively into high-quality growth at the right moments, while selectively allocating to smaller cap opportunities that can ultimately deliver outsized upside that you can't get in larger cap names like an Amazon (AMZN) or a Microsoft (MSFT). All of this is thanks to our in-house trading strategies and research processes that we have built over many years and teach to our students. This was not blind risk-taking. It was a deliberate focus on multiple areas of research including earnings durability, structural tailwinds, and mispriced growth, but moreso being able to find those opportunities before the market did.

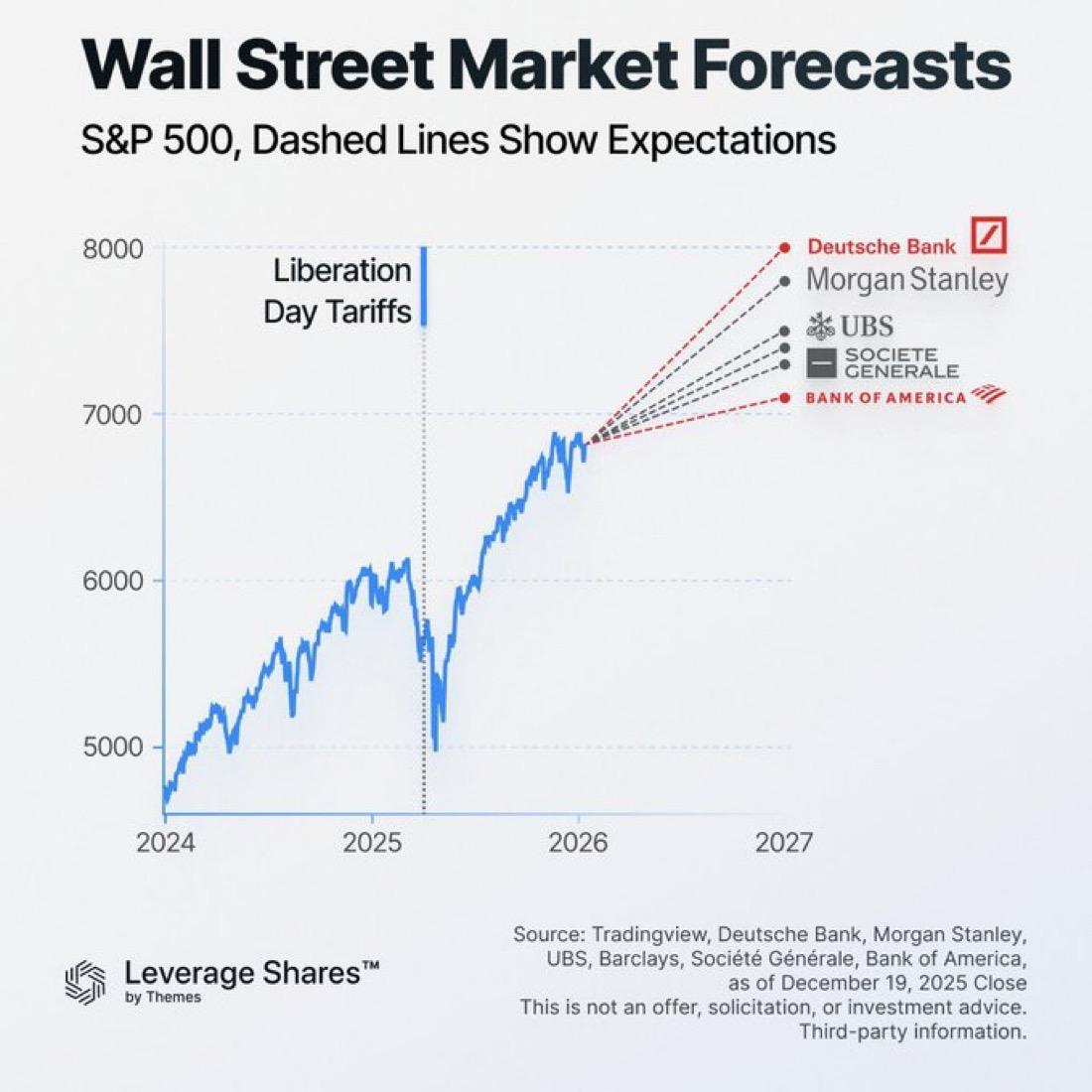

Looking ahead to 2026, our conviction remains high that another strong year is achievable and that we are already ahead on the stocks and sectors that will outperform this year. We believe we'll be able to outpace the market again significantly through our new 6 thematic investments for the year. These include themes such as drone, space, and robotic stocks. While companies like Rocketlab (RKLB) and AST SpaceMobile (ASTS) have already profited nicely, and a lot of the gains have been made in them already, we believe there are a handful of smaller-cap names that could do a 3-5x from here over the next year. And it's not just us who believes the market has more room to the upside in 2026, many major financial institutions broadly agree. The prevailing outlook calls for positive but choppier equity returns, as you can see below:

As for the thematic sectors in the market we are focusing on, and the stocks that we think are poised to benefit within them, here are 3 of the 6 themes and 1 stock for each that we are investing in for 2026:

- Drones:

- Red Cat (RCAT) - Red Cat is a U.S. technology company that develops and sells advanced all-domain unmanned systems and robotic solutions, including tactical drones and uncrewed surface vessels primarily for defense, government, and security customers. Its bull case for the next year centers on rising defense spending and accelerating adoption of its Black Widow and other autonomous systems, expansion into maritime unmanned platforms, and potential growth from large military contracts and regulatory tailwinds favoring domestic drone suppliers. Currently this stock sits at $9.16/share.

- Space:

- Planet Labs (PL) - Planet Labs designs, builds, and operates a large constellation of Earth-imaging satellites that provide daily global geospatial data and analytics to commercial and government clients worldwide. The bullish view for the next year is driven by expanding demand for satellite imagery and analytics, record backlog growth, new long-term contracts, expansion beyond pure imagery into geospatial intelligence and dedicated satellite services, and improving recurring revenue and free cash flow trends. Currently this stock sits at $20.41/share.

- Robotics:

- Ouster (OUST) - Ouster is a lidar technology company that manufactures high-resolution, digital 3D laser sensors used for autonomous vehicles, robotics, industrial automation, mapping, and smart infrastructure applications. Over the coming year the bull case suggests accelerating revenue growth as lidar adoption broadens beyond automotive into industrial, smart city, and robotics markets, improving unit economics, strong analyst ratings with elevated price targets, and momentum in sensor sales and deployment across multiple sectors. Currently this stock sits at $23.37/share.

These are just a small sample of the dozens of stocks we currently own and have on our Watchlists to buy in these thematic baskets. But hopefully, this opens the door for you to explore similar themes in the stock market throughout 2026. Now, if you're a CEO Watchlist Investment Club Member, you can [CLICK HERE] to access all 6 of our top thematic stock sectors for 2026, as well as the dozens of stocks in each sector that we currently own in our portfolio and are looking to buy in the coming weeks and months. If you're not a Club Member, and you're interested in getting access to all 6 of these themes, and the stocks we are buying in them, then [CLICK HERE] to join today. You will also get full access to our stock and options portfolios, as well as all of our research, strategies, and private live classes. And if you're brand new to Investing, that's why we also grant you access to our beginner Stock Market and Options Trading courses that will simplify everything for you from the ground up. Because it's the New Year, we still have our New Year's Sale going on, that grants you 40% OFF the subscription. So [CLICK HERE] to take advantage of this discount before the sale ends.

In summary, our 2026 outlook is very positive. The market is likely to grind higher over the year, driven by earnings growth and AI-led productivity, yet leadership will remain narrow and dispersion high. Technology and its adjacent enablers, alongside select small-cap industrial plays, appear best positioned, while laggards may continue to fall behind. This shift is structural, not cyclical, and still underpriced by many investors. The opportunity will not belong to those who simply stay invested, but to those who know where to look and know when to rotate when the opportunities present themselves.

Stock Spotlight: The Company That Controls the Semiconductor Bottleneck...ASML (Source)

Stocks mentioned: $ASML, $TSM, $INTC, $NVDA, $AMD, $AAPL

The global semiconductor industry is obsessed with chip designers and end products, from AI accelerators to smartphones, but far fewer investors focus on the quiet choke point that makes all of it possible. Advanced chips cannot be built without extraordinarily complex manufacturing tools, and this part of the value chain is both underappreciated and misunderstood. That is where ASML Holdings (ASML) enters the picture, a company that does not design chips or fabricate wafers, but instead controls the machines every leading chipmaker depends on. ASML sits at the foundation of modern computing, and its strategic importance continues to grow as chips get smaller, faster, and more powerful. The market may finally be waking up to this reality, after shares surged to record highs following a double upgrade from Aletheia Capital, with analyst Warren Lau issuing a Street high price target of $1,500/share. That move suggests recent data and demand signals imply ASML is still being underpriced relative to its true role in the semiconductor ecosystem.

ASML designs and manufactures photolithography machines, which are the tools used to etch microscopic circuit patterns onto silicon wafers. In simple terms, these machines determine how small, fast, and energy efficient a chip can be. ASML is the sole global supplier of Extreme Ultraviolet lithography systems, known as EUV, which are required to produce the most advanced chips used in AI data centers, high end smartphones, and cutting edge processors. Its customers include the most important chipmakers in the world, such as Taiwan Semiconductor (TSM) and Intel (INTC) who are the ones that produce chips for Nvidia (NVDA) and AMD (AMD). To put it simply, without ASML, the entire chip market would shut down and we would have a global stock market crash within the technology sector...that's how vital ASML is to the industry! The company’s advantage is reinforced by massive research and development spending, an exclusive supplier network, a multi-decade head start, and switching costs so high that customers are effectively locked in for years. This dominance has translated into strong financial performance, with revenue growth exceeding 20% year over year in recent periods and robust profitability driven by surging demand tied to AI and cloud infrastructure.

At the macro level, the world is entering a period of unprecedented semiconductor investment. Governments are pushing for domestic chip production, cloud providers are racing to build AI infrastructure, and every major technology platform is demanding more compute power per dollar. All of these trends require more advanced chips, and advanced chips require EUV lithography. ASML occupies a unique niche because it does not compete with chip designers or manufacturers, it enables all of them. When companies like Nvidia or Apple (AAPL) increase chip complexity, ASML benefits regardless of who wins market share. Even as geopolitical tensions and export restrictions introduce volatility, the long term direction is clear: more advanced nodes, more capital spending, and more dependence on ASML’s technology.

ASML sits at the intersection of AI, cloud computing, and national semiconductor strategy, turning what looks like a capital intensive bottleneck into a durable competitive advantage. Its machines are not optional upgrades, they are mandatory tools for progress. If Wall Street fully internalizes that ASML is not just an equipment supplier but a monopoly toll collector on advanced chip production, the valuation framework could shift meaningfully. Historically, markets have re rated companies that control critical infrastructure layers, from operating systems to payment networks, once their indispensability became obvious. ASML increasingly fits that profile, with a business model designed to compound quietly as the world demands more computing power.

"Super Investor" Spotlight: Triple Frond Partners (Source)

Stocks mentioned: $MSFT, $GOOG, $AMZN, $ASML, $TDG, $META, $LRCX, $CHTR, $ILMN, $TRU, $CCC

For newer readers, a “Super Investor” is a capital allocator who consistently compounds wealth at rates far above the broader market by making fewer, higher-conviction decisions. These investors tend to run concentrated portfolios, focus on business quality over headlines, and think in multi-year time horizons. Thanks to quarterly 13F filings, we get a rare look into how these elite managers deploy capital, even if the data is slightly delayed.

Triple Frond Partners is a textbook example of this philosophy. The firm runs an ultra-focused portfolio of just 11 stocks with roughly $918 million in disclosed assets. Rather than spreading risk across dozens of names, Triple Frond concentrates capital into companies it believes sit at the center of long-term global growth. This is a portfolio designed to compound, not trade.

Here is the full breakdown of Triple Frond Partners’ disclosed stock portfolio, ranked by position size:

• Microsoft (MSFT) – 21.7%

• Alphabet (GOOG) – 14.6%

• Amazon (AMZN) – 12.9%

• ASML (ASML) – 11.8%

• TransDigm Group (TDG) – 8.2%

• Meta Platforms (META) – 8.1%

• Lam Research (LRCX) – 6.2%

• Charter Communications (CHTR) – 4.8%

• Illumina (ILMN) – 4.0%

• TransUnion (TRU) – 3.9%

• CCC Intelligent Solutions Holdings (CCC) – 3.6%

But just having a stock portfolio from an investment firm you've never heard of doesn't do much good unless their able to beat the overall stock market. The whole point of investing our time into researching CEOs, politicans, and "Super Investors" to find an edge on the market is that they actually provide some type of performance above the average, and Triple Frond does exactly that. When looking at their performance over the past 3 years versus the S&P500, Triple Frond Partners has returned 118% versus 86% for the S&P500. That is an outperformance of roughly 37%, not too shabby when the stock market averages 10% per year.

The takeaway for retail investors is clear. Triple Frond Partners shows that long-term outperformance often comes from owning fewer businesses, understanding them deeply, and sizing positions aggressively when conviction is highest. Their latest portfolio reinforces a commitment to scale, infrastructure, and durable growth while maintaining discipline around risk. We like Triple Frond because this is what serious compounding looks like, calm, focused, and built for the long run. Plus, they are heavily investing into technology stocks, which we believe will be one of the best performing sectors of the year.

INSIDER STOCK TRADES FROM THE WEEK:

1. Under Armour (UA) - Billionaire Prem Watsa, bought roughly $138,000,000 of UA for an average price of $4.83/share between Dec. 22-30, 2025, but it was most recently reported to the public on Jan. 2, 2026. (Source)

2. Berkley WR Corp (WRB) - Mitsui Sumitomo Insurance Co., bought roughly $152,000,000 of WRB at an average price of $70.12/share between Dec. 23-29, 2025, but it was most recently reported to the public on Jan. 2, 2026. (Source)

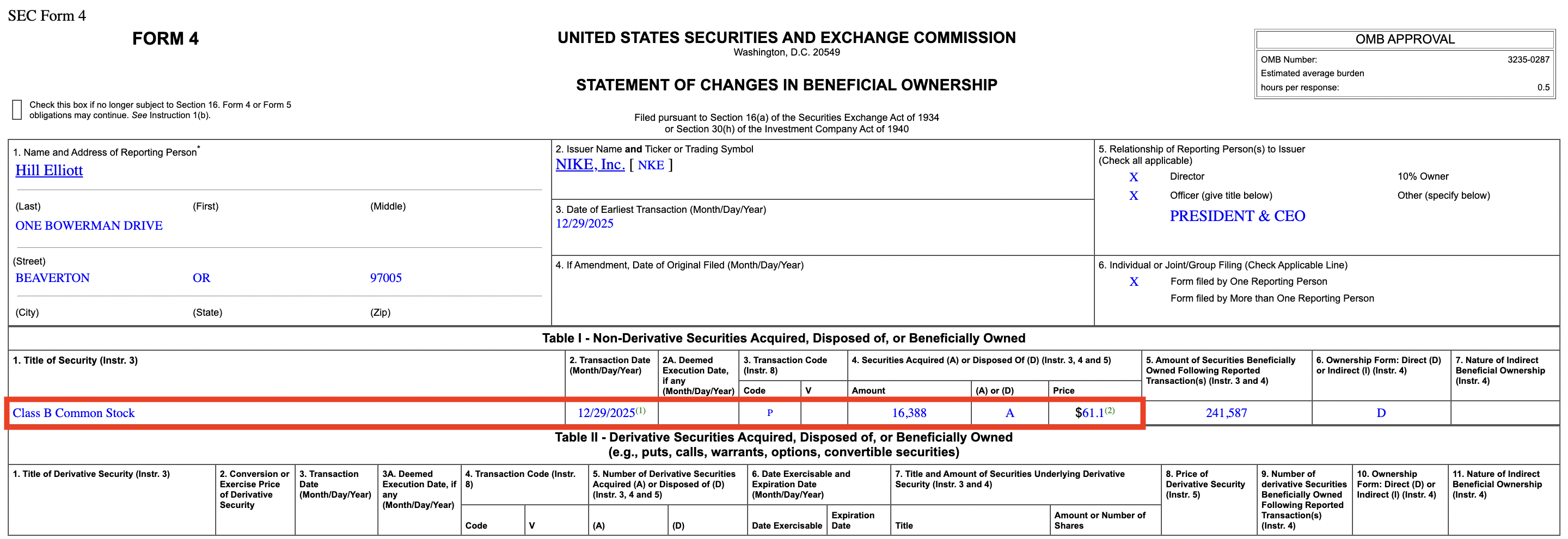

3. Nike (NKE) - Elliott Hill, CEO, bought over $1,000,000 worth of NKE at $61.10/share on Dec. 29, 2025, but it was most recently reported to the public on Dec. 30, 2025. (Source)

Over 2,000 people have already signed up for my FREE Masterclass video on how to unlock my exact strategies for finding winning stock/options trades! I'll share everything including how to find what Politicians and CEOs are buying. Don’t miss your chance to get in for FREE before spots fill up!

INFOGRAPHICS FOR THE WEEK:

CONTACT US: [email protected]

Responses